Electric Meter Serial Number: A Key to Insurance Fraud Prevention

The electric meter serial number, often called an MSN, is a unique alphanumeric code printed on the front of every meter. Usually found near a barcode, it serves as a critical identifier for utility companies and, increasingly, for insurance verification at policy inception. For insurers, it's a powerful tool for fraud prevention.

A Starting Point for Pre-Inception Verification

For an insurer, an electric meter's serial number is a powerful piece of evidence. This simple identifier forges a crucial link between a property and a policy at a specific moment in time—the very start of the cover period.

For claims directors and fraud teams, this connection is the first line of defence against a significant commercial problem: the lack of verifiable proof of a property's condition when the policy began.

Without this fundamental anchor point, the door is left wide open for costly disputes and opportunistic fraud. The "lounge exercise" illustrates this perfectly. Ask any policyholder to list the contents of their lounge after a burglary, and the process can quickly spiral into a six-week dispute over what was owned and when. The electric meter serial number acts as a fixed, verifiable data point to which all other evidence can be tied.

Why It Matters for Insurers

The core issue is proving what existed before a loss occurred. An MSN, captured in a time-stamped photograph, establishes an undeniable record.

- Fraud Prevention: It helps shut down 'after-the-event' fraud, where a policyholder submits a claim for an item that was already damaged or did not exist when the policy started. Learn more about how verified evidence can stop fraud before it happens in our detailed guide.

- Claims Efficiency: It cuts through the ambiguity that drags out claims investigations, reducing the need for expensive loss adjuster visits simply to verify basic property details.

- Underwriting Accuracy: It provides a solid foundation for building a verified inventory of contents, helping to ensure sum insured values are more accurate from day one and preventing underinsurance disputes.

Capturing the electric meter serial number is not just a procedural step; it is about establishing an irrefutable timeline. It transforms a policy from a simple agreement into a verifiable record, protecting both the insurer and the honest policyholder from inception.

Each of the over 40 million

smart and advanced meters installed in Great Britain has a unique Meter Serial Number (MSN). This alphanumeric code, such as S06DS123456

, often indicates the manufacturer (e.g., 'S' for Siemens), the year of calibration, and a batch sequence.

Capturing a clear, time-stamped photograph of this MSN creates irrefutable evidence that ties a policyholder's inventory to a specific property and date. You can discover more about the structure of these numbers on Wikipedia. This simple action is a foundational element for robust underwriting and proactive fraud prevention.

Why the Electric Meter Number Is a Weapon Against Insurance Fraud

It may look like a string of digits on a box, but for an insurer, the electric meter serial number (MSN) is a powerful strategic tool. It is a fixed, verifiable anchor point—a way to confirm a property's exact status at the precise moment a policy begins.

For claims directors and fraud investigators, this is invaluable. Without this simple piece of pre-inception evidence, insurers are often confined to a reactive, trust-based system that is wide open to exploitation.

The core problem it solves is after-the-event fraud . This is an all-too-common issue where claims are filed for items that were already damaged, broken, or simply did not exist before the policy was live. A time-stamped, geolocated photograph of the MSN, captured securely in a tool like the Proova app, provides irrefutable proof. It ties a policyholder’s entire inventory to a specific time and place, shifting the dynamic from a costly, drawn-out investigation to a straightforward verification exercise.

The True Cost of Inaction

Ignoring this simple verification step at policy inception can lead to serious operational inefficiencies and financial leakage. The consequences ripple across the claims department, slowing processes and frustrating genuine customers.

The commercial impacts are significant:

- Endless Dispute Resolution: When ambiguity exists about when damage occurred or what assets were at the property, claims handling times extend, and administrative costs soar. What should be a quick check becomes a lengthy dispute that damages the client relationship.

- Increased Claims Leakage: Paying out on fraudulent or inflated claims directly impacts profitability. Every claim settled without concrete inception evidence is a potential financial loss that could have been easily prevented.

- Unnecessary Loss Adjuster Costs: Despatching a loss adjuster to a property simply to confirm basic details that could have been documented from the start is a considerable and avoidable expense. Verifying contents remotely with solid evidence can reduce these visits dramatically.

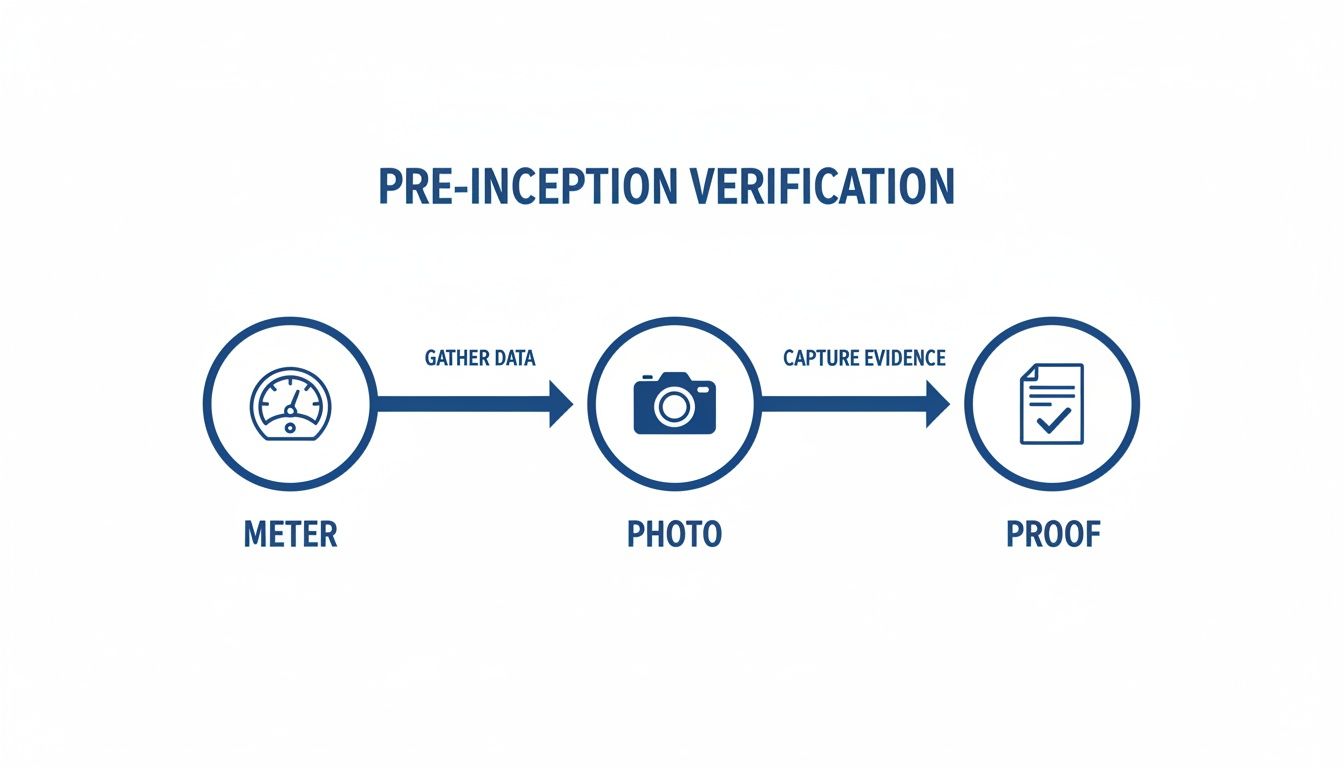

This simple flowchart shows how capturing meter data translates into concrete proof for claims teams.

As you can see, a simple photograph of a meter is transformed into powerful, verifiable proof, anchoring the entire policy to a physical reality.

A Strategic Asset for Claims Processing

Ultimately, treating the electric meter serial number as a strategic data point allows insurers to move from detection to prevention. It gives underwriting and claims teams the evidence they need to act decisively, reducing both fraudulent payouts and the operational friction that frustrates honest customers.

Adopting this approach is not just about cutting costs; it is about building a more resilient and efficient claims process from the ground up. You can explore more on this topic in our related article about using a claims database for insurance fraud prevention.

For an insurer, the MSN is not just a number; it is the start of a clear, auditable trail. It confirms 'when' and 'where', allowing claims teams to focus on the 'what' and 'how' with greater confidence and speed.

Understanding the MSN and its Link to the MPAN

To fully appreciate why the meter number is so important, it is necessary to distinguish between two key identifiers: the Meter Serial Number (MSN) and the Meter Point Administration Number (MPAN) . They work in tandem but serve different functions. For an insurer, knowing the difference is vital for securing property verification.

The electric meter serial number , or MSN, is the unique code stamped directly onto the physical meter box. It is the identifier for that specific piece of equipment. A useful analogy is the Vehicle Identification Number (VIN) on a car—it is permanently tied to that single object, and if the object is replaced, the number changes with it.

In contrast, the Meter Point Administration Number (MPAN) is a longer, 21-digit number that identifies the electricity supply point to the property. The MPAN is tied to the location , not the hardware. Therefore, if a new meter is installed, the MSN will be different, but the MPAN will remain the same.

What the MSN's Structure Reveals

A typical UK electric meter serial number is not just a random string of characters; it is coded with useful information. While exact formats can vary between manufacturers, they often follow a predictable pattern that reveals who made the meter and when.

For instance, an MSN like A##AA######

can often be broken down as follows:

- The First Letter: This usually indicates the manufacturer. A common example is ' D ', which stands for Landis+Gyr, one of the largest meter suppliers in the UK.

- The First Two Digits: These almost always represent the year the meter was manufactured or last calibrated. So, ' 12 ' would indicate the meter dates back to 2012.

This structure provides an extra layer of data that is incredibly useful for verification. An insurer is not just seeing a random number; they are seeing details about the meter’s age and origin, which can be cross-referenced with other property records for a much clearer picture.

This brings us back to the "lounge exercise"—if a policyholder cannot easily find or make sense of their own MSN, they stand almost no chance of accurately cataloguing their high-value assets without proper guidance. It perfectly highlights the need for a simple, structured solution like the Proova app to bridge that common evidence gap.

Why the MSN-MPAN Relationship Matters Commercially

For claims directors and brokers, understanding how these two numbers connect is critical. The MPAN confirms the correct property is being assessed, while the MSN confirms the specific equipment present at a certain time. When a policyholder uses a tool like Proova to capture a time-stamped photograph of their MSN, they create a verifiable, undeniable link between the physical asset (the meter) and the supply point (the MPAN).

In the UK, an MSN format like D12LC456789

(for a Landis+Gyr meter from 2012) unlocks key manufacturing data. With smart meter installations on track to exceed 40 million

by late 2025 and over 34 million

homes already operating in 'smart mode', a quick photograph of the MSN becomes definitive proof against 'after-the-event' fraud. The latest figures are available in the full government report on the smart meter rollout.

Of course, before decoding the MSN and MPAN, the basics must be understood. Learning how to read your electric meter is the first step in this process.

A Best Practice Guide for Verifying Customer Assets

Transitioning from a reactive, trust-based claims model to a proactive, evidence-led one requires a clear strategy. The electric meter serial number is an ideal starting point, but a truly robust verification process must encompass all high-value assets.

For insurers, the most effective way to reduce claims disputes and prevent after-the-event fraud is to implement a standard verification workflow at policy inception. This transforms a potentially lengthy, ambiguous claims investigation into a simple check against a pre-existing, time-stamped record.

Establishing a Clear Verification Workflow

The objective is to create an undeniable digital record of an asset's existence, its condition, and its location the moment cover begins. This simple step eliminates the subjective arguments that bog down many claims.

A best-practice workflow for any high-value item, whether a new television or a piece of jewellery, should secure a few key pieces of information:

- High-Quality Photo Evidence: Insist on clear, well-lit photographs of the entire item. Also require close-ups of any serial numbers, model numbers, or unique marks for identification.

- Core Item Data: The make, model, and serial number, recorded as text.

- Proof of Ownership: A photograph of a receipt, an invoice, or a valuation certificate that links the item directly to the policyholder.

This structured approach removes guesswork and provides claims handlers with the necessary information to process a claim efficiently.

The Role of Purpose-Built Technology

Simply asking a policyholder to email a random collection of photographs is ineffective. It is insecure, the data lacks context, and it is easily manipulated. This is where technology designed for this purpose becomes essential.

The Proova app was built specifically to solve this verification problem. Its features are designed to meet the high evidential standards insurers require:

- Geocoding and Time-Stamping: Every photograph taken within the app is automatically tagged with the precise location and time. This creates an unalterable record proving exactly where and when the asset was documented.

- Secure, Centralised Storage: All evidence is stored in a secure digital vault. This prevents data loss and ensures information is easily accessible when a claim is made.

- Guided User Experience: The app walks the policyholder through a simple, structured process, ensuring all necessary photographs and data are captured correctly for each item.

By integrating a solution like Proova at policy inception, insurers provide clients with a simple tool to build a verified inventory. This empowers the customer while giving the insurer the high-integrity data needed to clamp down on fraud and streamline claims processing.

The entire process of gathering evidence, starting with locating an electricity meter serial number, becomes a seamless part of obtaining cover. More detailed steps for policyholders are available in our guide on how to find your electricity meter serial number.

The Insurer’s Advantage: Stopping Fraud Before a Policy Starts

For claims directors and fraud teams, the battle against opportunistic claims is won or lost long before a First Notice of Loss is received. The traditional model—detecting fraud after a claim has been submitted—is a slow, expensive, and inefficient process.

This reactive approach forces teams to investigate claims with incomplete information, leading to protracted disputes and claims leakage. The smarter, more commercially sound strategy is prevention, not detection.

This is where documenting the electric meter serial number at policy inception becomes a significant strategic advantage. It acts as an unchangeable anchor point—a piece of verifiable evidence that locks in the exact location of a property’s contents the moment cover begins. This one simple step completely shifts the dynamic from a costly investigation to a straightforward verification.

From Reactive Detection to Proactive Defence

Attempting to catch fraud after a claim is like trying to extinguish a fire that should never have started. The real costs are not just in the fraudulent payouts but in the operational drag created by every questionable claim that slows down the process.

Consider the common scenarios that drain team time and resources:

- After-the-Event Fraud: A classic tactic where a policyholder insures an item that was already damaged, waits a period of time, and then files a claim. Without solid evidence from day one, proving this is a difficult, time-consuming, and often fruitless task.

- Phantom Assets: Claims submitted for high-value items that were never at the property in the first place. Verifying this after a total loss event like a fire is nearly impossible without pre-existing documentation.

By requiring a verified inventory, anchored by the property’s electric meter serial number, insurers create a robust and practical defence against these common types of fraud.

The Clear Commercial Benefits

Implementing a pre-inception verification process delivers tangible results that impact the bottom line. This is not just about minor efficiency gains; it is about eliminating unnecessary costs and protecting profitability.

A verified inventory, created using a tool like Proova , allows insurers to:

- Slash claims handling time from an industry average of 14 days down to just 7 days by removing guesswork.

- Reduce loss adjuster costs significantly by enabling remote verification of contents, which means fewer expensive site visits.

- Improve underwriting accuracy by ensuring sums insured are based on verified assets, preventing underinsurance disputes before they can arise.

Since 1998 , UK electricity meters have been tied to 21-digit MPANs, with the core 13 digits uniquely identifying each meter alongside its MSN. For insurance professionals, this provides a direct line to fraud prevention. Without MSN-proofed inventories, claims directors face a constant validation battle. Proova's app makes logging this simple, proving asset locations before a loss ever occurs and fundamentally strengthening the underwriting process. You can learn more about how these meter numbers work on UW.co.uk.

For a claims director, a verified inventory is the ultimate tool for certainty. It turns a potential six-week dispute into a simple cross-reference, saving time, money, and protecting the integrity of the claims process. This is the commercial case for making pre-inception verification standard practice.

Your Questions Answered

Here we address common questions from insurance professionals about integrating the electric meter serial number (MSN) into their underwriting and claims workflows. The answers are designed to provide practical clarity and demonstrate the commercial sense behind obtaining this proof upfront.

Will My Client's Electric Meter Serial Number Change?

Yes, it will—and that is precisely why it is so valuable. The MSN changes whenever an engineer physically replaces the meter. Obtaining a time-stamped record at the start of the policy creates a definitive, unarguable starting point for cover.

When a policyholder uses a tool like Proova to document their new meter’s serial number after a replacement, it creates a clear, auditable trail. This prevents future arguments about which assets were present under a specific meter installation, ensuring total clarity for any subsequent claim.

Is the Electric Meter Serial Number the Same as the MPAN?

No, they are two different identifiers, though they work together. The MSN is the unique code stamped onto the physical meter box itself. The MPAN (Meter Point Administration Number) identifies the electricity supply point for the entire property.

Energy suppliers use both for billing, but for an insurer, the MSN is the crucial piece of physical evidence. It proves that a specific device was installed at a specific property at a specific moment in time, anchoring the entire contents inventory to a tangible, verifiable asset.

Think of it this way: the MSN provides the physical proof of 'what and where', while the MPAN confirms the location's supply line. Using both gives underwriting teams a robust, cross-referenced data set to validate a policyholder's address and property status from day one.

Why Should My Underwriting Team Care About a Meter Number?

Underwriters should care because the MSN is a powerful, verifiable link between a policy and a physical property at the exact moment cover begins. It acts as an undeniable anchor for the policyholder’s entire contents inventory.

This single piece of evidence helps to prevent after-the-event fraud by proving the property’s status at policy inception. This documentation drastically reduces ambiguity, which in turn leads to faster, more accurate claims processing and fewer costly disputes down the line. It strengthens the integrity of the entire policy from the start.

What if the Serial Number Is Hard for a Policyholder to Read?

If the number on the meter is obscured by dirt, damage, or fading, the policyholder should still take the best possible photographs of the meter. They can then find the electric meter serial number on a recent energy bill.

When using a documentation app, they should record the number from the bill and add a clear note explaining the meter itself was illegible, including the photographs as supporting evidence. This level of diligence demonstrates good faith and strengthens the overall integrity of their verified inventory.

A verified inventory, anchored by the electric meter serial number, is the most effective way to prevent fraud and streamline claims. Proova provides the purpose-built platform to make this a standard, scalable part of your underwriting process. Learn more at https://www.proova.com.