A Complete Guide to Waivers of Subrogation in the UK

A waiver of subrogation is a contractual clause that stops an insurance company from coming after a third party to get back money it paid out on a claim. It sounds complicated but in essence, it's an agreement made upfront to prevent a blame game later on.

What Are Waivers of Subrogation and Why Do They Matter?

Let’s picture a common scenario. A contractor you've hired accidentally starts a small fire on your business premises. Your insurance policy covers the damage and your insurer pays the claim, no problem. Normally, your insurer would then "step into your shoes" to sue the contractor and recover the money they paid you. This right to chase the at-fault party is called subrogation .

A waiver of subrogation , however, flips this on its head. It’s a pre-agreed clause in a contract where one party willingly gives up this right. By signing it, you're telling your insurer they can't seek reimbursement from the other party in the contract, even if their negligence caused the loss.

This might seem odd at first glance—why would you let someone off the hook? But it serves a vital purpose in business. It prevents messy, expensive and relationship-damaging lawsuits between parties working together on the same project, like a general contractor and their subcontractors or a landlord and tenant.

Instead of getting bogged down in litigation, the financial hit stays with the designated insurer. Before we get into the nuts and bolts of the clauses themselves, it's worth understanding the legal bedrock they're built on. Getting to grips with the fundamental elements of a contract shows how these crucial agreements are pieced together.

The Hidden Costs of Waiving Rights

While these waivers are great for keeping projects moving and relationships intact, they create a serious headache for insurers and, by extension, their customers. When an insurer cannot recover losses from a negligent party, the entire financial burden is absorbed by the insurance pool.

This is where the real challenge begins. Without the threat of subrogation, a third party has little reason to argue the details of an incident. This can swing the door wide open for exaggerated or even fraudulent claims to slip through unchallenged, undermining the provability of any claim.

When an insurer's right to investigate and recover is signed away, the goalposts for proving a claim shift. This creates vulnerabilities that, if exploited, drive up claim costs, fuel insurance fraud and ultimately increase costs for all of us.

This is not just an insurer's problem; it has a ripple effect that touches every policyholder. When fraudulent or inflated claims go unchallenged, insurers pay out more than they should. Those extra costs are not just absorbed by the company—they are passed on to all customers in the form of higher premiums.

More unchallenged claims mean a less stable and more expensive insurance market for everyone. To truly understand the principles at play, our complete UK guide on subrogation in insurance offers a deeper dive. This really drives home the critical need for solid verification methods right from the start of a policy, ensuring claims are legitimate and provable. It’s about protecting the integrity of the system and keeping costs fair for everyone.

Let's be clear: a waiver of subrogation is not just another bit of legal jargon tucked away in a contract. In the real world of UK commercial projects, it's a vital tool for keeping things moving. Think of it as a pre-agreed truce.

In high-stakes industries like construction, commercial property and logistics, these waivers are the bedrock of smooth operations and stable business relationships. By deciding upfront who carries the financial can for any mishaps, they stop costly, time-consuming disputes from ever getting off the ground.

Picture a major London construction site—a dizzying network of main contractors, subcontractors and suppliers. If a subcontractor’s mistake leads to damage that the main contractor’s insurance covers, a waiver of subrogation is what stops the insurer from chasing that subcontractor for the money. This is absolutely critical. It prevents a domino effect of lawsuits, keeps vital working relationships intact and stops the entire project from grinding to a halt.

It’s a similar story in commercial property. These waivers are standard in leases because they protect landlords and tenants from legal battles started by each other's insurers. If a tenant’s dodgy wiring causes a fire, the landlord’s insurer pays for the damage but is contractually barred from suing the tenant. This creates a stable, cooperative environment—exactly what you need for a long-term tenancy.

A Standard Feature in High-Stakes Projects

Waivers of subrogation are now deeply woven into the fabric of UK commercial practice, especially in construction. What might have once been a bespoke clause is now a standard feature in major building contracts. This is particularly true for projects involving public bodies or large developers who simply cannot afford the delays that infighting would cause. The industry has made a strategic choice: project continuity is more important than recovering losses from a partner.

The data backs this up. A 2022 survey from the Royal Institution of Chartered Surveyors (RICS) revealed that 78% of construction professionals in England and Wales now include a waiver of subrogation clause as standard. For projects over £10 million, that number jumps to an overwhelming 89% . This shift has even started to influence insurance pricing. A 2023 analysis found that policies for projects with a waiver saw premium reductions of between 7% and 12% . You can read more about how these clauses have evolved and their impact on the insurance market.

A Double-Edged Sword for Insurers

While waivers provide commercial peace of mind, they create a real headache for insurers. By signing away the right to pursue a negligent third party, an insurer’s ability to get to the bottom of a claim is seriously hampered. The party at fault has no real reason to contest the details of what happened or the cost of the damage, creating a dangerous blind spot.

A waiver of subrogation effectively silences a key witness in a potential claim investigation—the very party that caused the loss. This can make it incredibly difficult to verify the true cause and cost of the damage, directly threatening the provability of the claim.

This is where the door creaks open for fraud. A party could, for instance, claim for pre-existing damage, knowing full well the insurer cannot approach the one person who could challenge the claim's origin. This inflates claim costs across the board and guess who ends up paying for it? All policyholders, through higher premiums that affect the entire industry.

This highlights a critical vulnerability in the system. There’s a pressing need for robust, independent proof of an asset's condition before a policy even starts. This is the only way to maintain the provability of claims when the right to subrogate has been signed away.

What Happens to the Claims Process with a Waiver?

When an incident happens on a project covered by a waiver of subrogation, the whole claims process looks completely different. Gone is the complicated blame game of figuring out who’s liable. Instead, the path forward is refreshingly direct.

The focus shifts entirely to the policyholder's own loss. There’s no looming threat of legal action between the parties who signed the contract, which is precisely the commercial benefit everyone wanted in the first place. The insurer’s investigation has just one goal: validate the policyholder's claim and get it paid. They do not need to spend time or money figuring out which other contractor might be at fault because the right to chase them was signed away from the start.

Certainty Beats Conflict Every Time

Without a waiver, the claims process can quickly spiral into a costly, relationship-damaging dispute.

Imagine a pipe bursts in a leased commercial property and floods the unit below. The landlord’s insurer pays for the damage but then immediately starts pursuing the tenant’s insurer for reimbursement. What follows is a long, expensive legal battle that creates massive friction and ruins the landlord-tenant relationship. It’s a classic example of how a simple incident introduces conflict and uncertainty into the mix.

Now, let’s replay that scenario with a mutual waiver of subrogation in the lease.

- Incident Occurs: The pipe bursts and causes damage.

- Claim is Filed: The landlord files a claim directly with their own insurer.

- Insurer Acts: The insurer validates the loss and pays the landlord’s claim.

- Process Ends: That’s it. The matter is closed. The insurer has no right to sue the tenant, preserving the business relationship and avoiding a pointless legal fight.

This is how waivers of subrogation inject legal certainty right from the outset, guaranteeing a faster and more efficient outcome for everyone involved.

By pre-emptively removing the right to subrogate, the claims process is transformed from a potential multi-party legal dispute into a straightforward, two-party administrative procedure. This simplification saves time, money and commercial partnerships.

The Make-or-Break Role of Precise Wording

Here’s the catch: this streamlined process lives or dies on the quality of the waiver clause itself. An ambiguous or poorly drafted waiver is actually worse than having no waiver at all. It creates loopholes that invite the very disputes it was designed to prevent.

For a waiver to stand up, its language must be crystal clear. It has to spell out exactly which rights are being waived, which parties are covered and the specific circumstances where it applies. Any hint of vagueness can be challenged in court, potentially making the whole clause worthless.

And that’s where the real risk lies. A flawed clause does not just fail to protect you; it can cause a policyholder to accidentally breach their insurance policy. Insurers must be told about and agree to the waiver. If the contract language does not align perfectly with the policy endorsement, a claim could be flat-out rejected, leaving the policyholder dangerously exposed. The entire agreement’s strength rests on its clarity.

The Hidden Link Between Waivers and Insurance Fraud

While waivers of subrogation are powerful tools for keeping commercial relationships smooth, they bring a significant and often overlooked vulnerability. By design, they tie an insurer's hands, restricting their ability to fully investigate the context of a claim. This can inadvertently swing the door wide open to insurance fraud.

This limitation creates a critical information gap. When an insurer is contractually blocked from pursuing a negligent third party, that party has very little incentive to dispute the details of what happened or the extent of the damage. They’re effectively taken out of the picture, which can make it incredibly difficult to verify if a claim is legitimate.

How Waivers Create Opportunities for Fraud

This lack of scrutiny can be easily exploited. Imagine a situation where a party submits a claim for pre-existing damage, knowing full well the insurer is prevented from contacting the one party who could confirm the damage was already there. It becomes a classic case of one person's word against a silent third party, making the provability of the claim almost impossible.

This dynamic makes it far easier to inflate the value of a genuine claim or to fabricate a loss entirely. Without the threat of subrogation holding them accountable, the responsible party has no reason to challenge exaggerated repair costs or questionable damage assessments. An environment where opportunistic fraud can thrive is created.

When a waiver of subrogation is in place, the burden of proof shifts almost entirely onto the policyholder and their insurer. This removes a crucial layer of accountability and can make it difficult to distinguish between genuine losses and fraudulent claims, impacting the entire industry.

The sheer prevalence of these clauses is a testament to their commercial usefulness. A detailed 2021 study by the Law Society’s UK Insurance and Reinsurance Law Committee found that 63% of commercial policies contained some form of subrogation waiver, a figure that rose to 74% in commercial real estate.

Interestingly, the study also noted that UK insurers only formally invoked subrogation in 12% of property claims over £100,000 in 2020. This highlights a clear strategic preference for using waivers and settlements to maintain business relationships.

The Cost to the Industry and Policyholders

The consequences of this vulnerability reach far beyond a single questionable claim. Every fraudulent or inflated payout feeds the wider problem of insurance fraud, which costs the UK economy billions each year. These losses are not just absorbed by insurers; they get passed on to every policyholder in the form of higher premiums.

Essentially, an unchallenged fraudulent claim today contributes to a more expensive insurance market for everyone tomorrow. The commercial benefits of waivers, therefore, come with a hidden cost that impacts the entire industry. This is a growing concern for businesses, as you can learn more about in our guide to insurance fraud and its impact on UK businesses.

This dynamic underscores a critical need within the industry. To keep the benefits of waivers of subrogation while protecting against fraud, there must be a greater focus on the provability of claims . Establishing robust, independent proof of an asset's condition and ownership before a policy even begins is no longer just good practice. It is essential for safeguarding the integrity of the claims process and ensuring fair outcomes for all.

Using Technology to Bridge the Verification Gap

The real vulnerability with a waiver of subrogation is not the clause itself, but the information gap it creates. By design, it stops an insurer from investigating a third party after a loss. While commercially useful, this also weakens the ability to fully verify a claim's legitimacy.

This gap is exactly where opportunistic fraud finds room to grow. It drives up costs across the entire insurance industry, which ultimately means higher premiums for every policyholder.

Fortunately, modern technology offers a direct and powerful solution. We can now close that information gap by creating an undeniable, time-stamped record of an asset's condition and ownership right at the start of a policy. This digital proof acts as a verifiable baseline, restoring the certainty and provability that a waiver often removes.

By building an immutable digital inventory, insurers and loss adjusters gain a crucial advantage. When a claim comes in, they can instantly compare the asset's current state against its verified condition at policy inception. This simple check makes it incredibly difficult for fraudulent claims involving pre-existing damage to succeed.

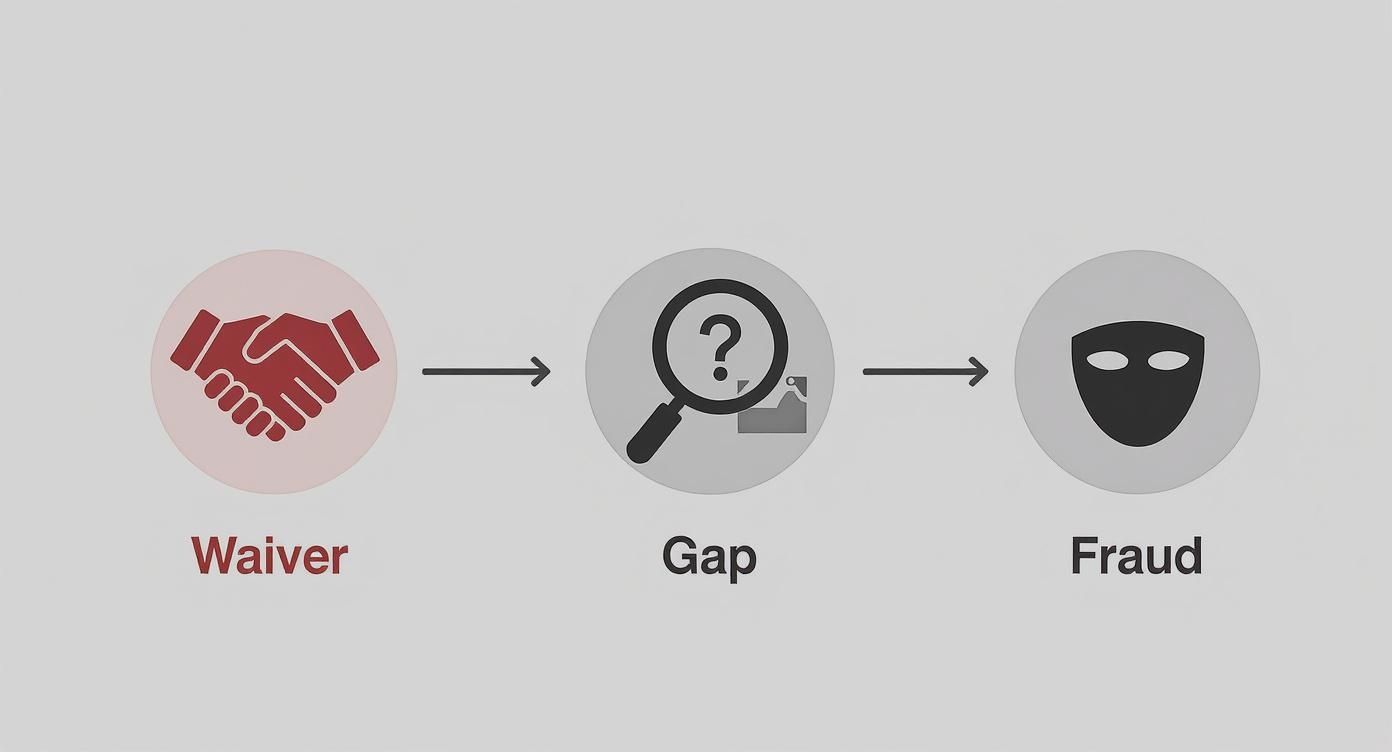

As the following flow shows, the waiver can inadvertently create a gap that fraudsters are all too willing to exploit.

By removing a key party from the accountability chain, a waiver introduces a verification challenge that needs to be managed.

Shifting from Reactive to Proactive Verification

Traditionally, claims handling has always been a reactive game. An incident happens and then the investigation begins, often held back by a frustrating lack of baseline evidence. Technology flips this entire model on its head, moving the critical verification stage to the very beginning of the insurance lifecycle.

This proactive approach fundamentally changes the dynamic of a claim. Instead of trying to piece together the past from fragmented information, claims handlers can start from a solid foundation of truth.

The benefits are immediate and significant:

- Deters Opportunistic Fraud: When potential fraudsters know a verifiable record exists from day one, the incentive to claim for old damage simply vanishes.

- Empowers Claims Handlers: Adjusters have clear, unambiguous evidence in their hands. This allows them to make faster, more accurate decisions with far greater confidence.

- Reduces Operational Costs: Investigations become simpler and less contentious, which significantly lowers the administrative burden and the associated expenses.

By establishing a 'single source of truth' before a policy even begins, technology allows the commercial benefits of waivers to be maintained while effectively neutralising the associated fraud risk.

This approach ensures the commercial convenience of waivers of subrogation does not come at the cost of claim integrity. You can find out more about this preventative strategy in our guide on fighting fraud before it happens with the power of verified evidence.

Strengthening Contracts and Claims Alike

The integrity of the waiver clause itself is also paramount. Ambiguous or poorly drafted wording can undermine the entire agreement and spiral into costly legal challenges. Here too, technology can lend a hand. An AI Legal Contract Analyzer can offer invaluable insights by dissecting complex legal documents to ensure the language is robust and fit for purpose.

The table below highlights the practical difference between a traditional claims process involving a waiver and one enhanced by proactive, technology-led verification.

Traditional Process vs Technology-Enhanced Verification

| Challenge Area | Traditional Claims Process (With Waiver) | Technology-Enhanced Process (With Waiver) |

|---|---|---|

| Evidence Quality | Relies on post-loss photos, witness accounts and documents which can be subjective or missing. | Starts with an immutable, time-stamped digital record of asset condition from policy inception. |

| Fraud Vulnerability | High. Easy to claim for pre-existing damage as there is no baseline proof to challenge it. | Low. Pre-existing damage is documented, making it nearly impossible to claim for it fraudulently. |

| Claim Settlement Time | Can be slow due to lengthy investigations and disputes over the cause or extent of damage. | Fast. Clear evidence allows for rapid validation and settlement of legitimate claims. |

| Adjuster Confidence | Moderate to low. Decisions are often based on interpretation rather than hard facts. | High. Decisions are backed by verifiable data, reducing ambiguity and disputes. |

| Operational Costs | Higher due to extensive investigation, potential litigation and fraudulent payouts. | Lower. Simplified investigations and reduced fraud lead to significant cost savings. |

As you can see, embedding verification technology at the point of underwriting creates a clear, undisputed record that protects everyone involved. It gives the policyholder proof of ownership and condition and it gives the insurer the evidence needed to handle claims fairly and efficiently.

Ultimately, the goal is to build an environment where legitimate claims get paid quickly and fraudulent ones are stopped in their tracks. This simple but powerful shift strengthens the entire insurance ecosystem. It leads to fairer outcomes for honest customers, reduces the financial impact of fraud that drives up premiums for all of us and allows the industry to operate with far greater transparency and confidence.

The result is a system where waivers can function as intended—as tools for commercial harmony—without creating unintended vulnerabilities.

Best Practices for Managing Subrogation Waivers

Successfully managing a waiver of subrogation is not just about paperwork; it requires genuine diligence from everyone involved. Treating these clauses as a simple box-ticking exercise is a massive misstep. The smart approach is to see them as a deliberate risk management strategy, one that needs to be supported by robust proof to avoid painful complications down the line.

This shift in perspective is what separates a smooth process from a future dispute. For policyholders, brokers and insurers alike, being proactive is always better than reacting after something has gone wrong.

Each party has a distinct but equally critical role to play in making sure these clauses work as intended, without opening the door to unnecessary risk or even outright insurance fraud.

Advice for Policyholders

As the policyholder, it’s on you to understand precisely what you’re signing. Before you agree to any contract containing a waiver of subrogation , you need to read the clause carefully and get your head around your obligations.

Once you’ve signed, your next immediate step should be to get your insurance policy updated to reflect the waiver. If you do not tell your insurer and get the right endorsement, you could be in breach of your policy conditions. That’s a dangerous gamble that could leave you completely uninsured for a specific loss.

Guidance for Insurance Brokers

Brokers are the critical link, bridging the gap between the policyholder and the insurer. Your job demands meticulous due diligence to advise your clients correctly and ensure their cover perfectly aligns with the contracts they're signing.

When your client agrees to waive subrogation, you have to act fast to get the necessary endorsement from the insurer. This is not just admin; it’s a crucial step that protects your client from being exposed to a breach of contract and ensures their insurance policy actually works when they need it most.

Proactive management is the cornerstone of effective risk transfer. A waiver of subrogation must be a conscious, documented decision reflected in both the commercial contract and the insurance policy, not an administrative afterthought.

Recommendations for Insurers

For insurers, the challenge is twofold: accepting that waivers are a commercial reality while guarding against the fraud and inflated claims that can come with them. This starts with having clear, consistent underwriting guidelines for when and how you’ll grant these waivers.

Bringing in modern verification technology is key to strengthening your position against fraud. By requiring immutable, time-stamped proof of an asset’s condition when the policy starts, you establish a baseline. This simple step makes it incredibly difficult for anyone to claim for pre-existing damage and preserves the integrity and provability of the claims process.

This strategy is especially important given how common waivers are in certain UK markets. In the professional indemnity and warranty & indemnity (W&I) sectors, for instance, they’re now almost universal. A 2023 analysis found that a staggering 92% of W&I policies had a waiver to protect the seller. You can get a deeper insight into how this plays out by reading about common claims themes in W&I insurance. By demanding better proof from day one, insurers can manage this widespread risk much more effectively.

Common Questions Answered

So, what exactly is a waiver of subrogation ? Think of it as a contractual agreement where you willingly sign away your insurer’s right to chase a negligent third party for money after they've paid your claim. In short, it stops your insurance company from suing the other party named in your contract.

Will a Waiver of Subrogation Affect My Insurance Premium?

Yes, it usually will, but often only slightly. When you agree to a waiver of subrogation, you're essentially telling your insurer they cannot recover their losses from the at-fault party. This means they have to absorb the full financial hit of a claim. To account for this extra risk, they'll typically add a small charge to your premium.

Is a Waiver of Subrogation Always Legally Binding?

Not always. For a waiver to hold up in court, the language in the contract has to be crystal clear and precise. Any ambiguity can be challenged and might lead to the clause being thrown out. Crucially, your insurer must be officially told about it and agree to it, usually by adding a formal endorsement to your policy. If they have not given their consent, the waiver might not be worth the paper it's written on and could even put you in breach of your policy terms.

The real test is provability. A waiver’s strength comes down to its clarity and the formal agreement of everyone involved—especially the insurer who is giving up a fundamental right.

Does a Waiver Stop All Potential Lawsuits?

No, it’s not a get-out-of-jail-free card. A waiver of subrogation only stops your insurer from suing the other party to get back the money they paid out on your claim. It does not prevent the other party from suing you directly for any damages not covered by your insurance, nor does it affect claims for losses that fall below your policy's excess.

Ultimately, while these waivers are great for keeping commercial relationships smooth by preventing insurer-led legal battles, they put a much bigger spotlight on the provability of claims . This raises the stakes on tackling insurance fraud and highlights just how vital it is to verify an asset’s condition right from the start of a policy, which can otherwise drive up costs for everyone.

Mitigate fraud risk and strengthen your claims with Proova . Our platform creates an undeniable, time-stamped record of assets when a policy begins, protecting you from fraudulent claims and paving the way for fair, fast settlements. Discover a smarter way to manage insurance verification at https://www.proova.com.