Third Party Insurance vs Comprehensive Cover: A UK Insurer's Guide

At its heart, the difference between third-party and comprehensive insurance is simple. Third-party only (TPO) covers damage you cause to other people and their property but comprehensive insurance does all that plus it covers damage to your own vehicle.

TPO is the bare-bones legal minimum you need to drive in the UK. It is designed to make sure that if you are at fault in an accident, the other person involved is not left out of pocket. Crucially, it leaves you to foot the bill for your own car's repairs.

Third-Party vs Comprehensive: The Core Differences

Choosing the right level of motor insurance is a major decision for any driver. The choice between third-party and comprehensive cover ultimately decides who is financially responsible after an accident. Getting to grips with these fundamental differences is the first step for any insurance professional when advising clients on risk, value and what is right for them.

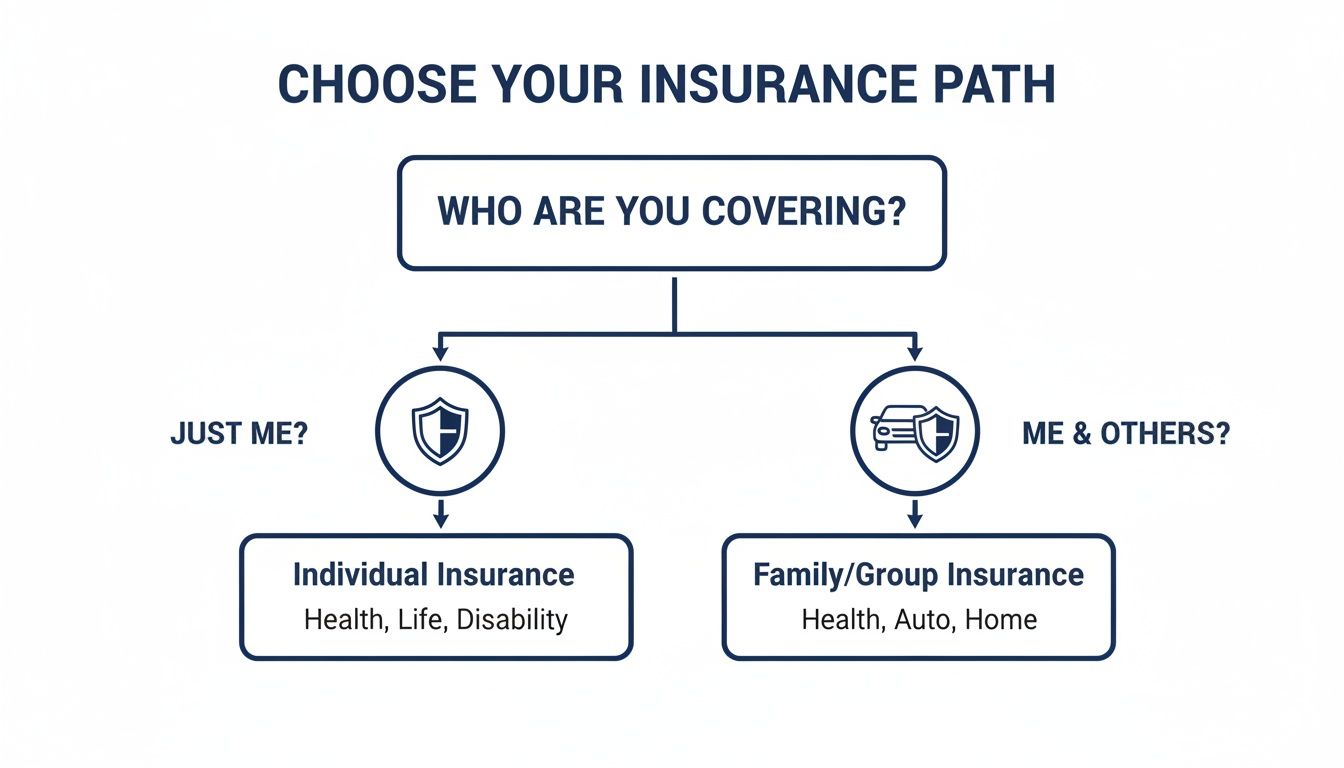

This decision tree breaks down the choice into the two main paths for insurance coverage.

The flowchart boils it down to a single question: are you protecting only others or are you protecting yourself as well? This core distinction should be the starting point for any policy discussion.

Defining the Two Levels of Cover

Third-Party Only (TPO) is the most basic car insurance you can get and it is all you need to meet the minimum legal requirements of the Road Traffic Act. Its only job is to cover the costs if you injure someone or damage their property—be it another driver, their passengers or a pedestrian. If you cause a crash, this policy pays for their repairs and any compensation claims. You can dive deeper into the specifics in our what is third party car insurance UK guide.

On the other hand, comprehensive cover gives you the highest level of protection. It includes everything a TPO policy does but extends that protection to you and your vehicle. This means it typically covers repair costs for your own car, regardless of who was at fault. It also usually includes cover for things like fire damage, theft and windscreen repair.

At-a-Glance Coverage Comparison

To make the distinction crystal clear, this table offers a simple side-by-side view. It is a great way to quickly explain the key differences to policyholders.

| Coverage Feature | Third-Party Only (TPO) | Comprehensive |

|---|---|---|

| Damage to Others' Property | ✔️ Covered | ✔️ Covered |

| Injury to Other People | ✔️ Covered | ✔️ Covered |

| Damage to Your Own Vehicle | ❌ Not Covered | ✔️ Covered |

| Theft of Your Vehicle | ❌ Not Covered | ✔️ Covered |

| Fire Damage to Your Vehicle | ❌ Not Covered | ✔️ Covered |

| Personal Injury to You | ❌ Not Covered | ✔️ Covered (Often) |

| Windscreen Damage | ❌ Not Covered | ✔️ Covered (Often) |

As you can see, the gap in protection is significant. TPO handles your liability to others, while comprehensive insurance looks after both your liabilities and your own assets.

The Problem of Proof and Fraud

A huge challenge for insurers stems from the very nature of these policies. With TPO, the risk of fraudulent personal injury claims—like exaggerated whiplash—is much higher because the entire claim focuses on the third party's losses. The provability of such claims is a constant battleground.

For comprehensive policies, the risk shifts towards things like 'after-the-event' fraud and claim embellishment. It is not unheard of for someone to damage an uninsured item, quickly buy a policy and then file a claim for it. Or they might inflate the value of items stolen from their car. These fraudulent acts add significant costs which are passed on to all policyholders.

Both scenarios point to the same central problem for the insurance industry: the difficulty of proving what existed and in what condition before a loss happened. This "provability gap" is where major costs and fraudulent activities take root, which ultimately drives up premiums for everyone. Without a reliable, verifiable record at the start of a policy, insurers are often stuck between launching costly investigations or paying out questionable claims, a cost the industry and honest consumers must bear.

Decoding UK Market Trends and Premium Paradoxes

The UK car insurance market can be a strange place, where common sense does not always seem to apply. One of the most glaring examples is a trend that defies basic logic: premiums are falling while the cost of claims is shooting through the roof. For insurers, making sense of this environment means getting to grips with the intense competitive pressures and driver behaviours that define it.

It is a tough climate to operate in. Fierce competition on price comparison websites keeps pushing premiums down yet the actual cost to settle claims keeps climbing. This puts a massive squeeze on profitability and makes smart risk management more vital than ever.

The heart of the problem is the growing expense of vehicle repairs and personal injury claims. Modern cars are loaded with sophisticated tech—sensors, cameras and advanced driver-assistance systems—that costs a small fortune to repair or replace, driving the average claim value ever higher.

The Comprehensive Premium Conundrum

Here is where it gets really counter-intuitive. It is often the most extensive comprehensive policies that face the fiercest price competition. This has created a bizarre situation where, in many instances, comprehensive cover is actually cheaper than a basic third-party only policy. The logic? Insurers often see drivers who choose comprehensive cover as more risk-averse—and therefore a safer bet—pricing their policies more attractively to win their business.

This pricing strategy has a huge impact on what customers buy. When the price difference is tiny or even inverted, the decision is no longer about cost. It is about getting far better protection for your money. Unsurprisingly, the market has shifted decisively.

Recent analysis throws this trend into sharp relief. By mid-2025, the average comprehensive car insurance premium stood at £757 annually , a drop of 16% from the year before. That is nearly a quarter down from the peak in late 2023 but this price drop hides a worrying truth: the average claim cost jumped by 37% between 2019 and 2023. It is no wonder 73% of UK drivers now go for fully comprehensive insurance. You can find more insights about these car insurance premium trends and see why people want broader protection.

Consumer Behaviour and Market Dominance

The overwhelming preference for comprehensive cover says a lot about the modern driver. They value peace of mind and protecting their own car far more than just bagging the lowest possible premium, especially when the price difference is so small.

For insurers, this is both an opportunity and a major risk. It shows a clear demand for higher-value products but it also means risk gets concentrated in comprehensive portfolios. A single comprehensive claim, involving a high-value vehicle and potential injuries, can easily wipe out the premiums collected from dozens of other policies.

The current market proves that lower premiums do not mean lower risk. In fact, it is often the opposite. As claim severity grows, the financial exposure for insurers offering cheap comprehensive policies skyrockets, making accurate underwriting and fraud detection essential for survival.

This is where the ability to verify a vehicle’s existence and condition at the start of a policy becomes a true game-changer. Without that proof, insurers are wide open to claim embellishment and after-the-event fraud, where someone buys a policy after their car is already damaged. This kind of fraud adds hidden costs that everyone else ends up paying for through higher premiums.

To manage a portfolio effectively in this landscape, insurers need to move from reactive claim investigations to proactive risk verification. By getting a clear, evidence-based record from day one, they can navigate the premium paradox, protect their bottom line and stop honest customers from subsidising fraudsters. That is the foundation of a fair and sustainable insurance model for everyone.

The Real Cost of Claims and the Shadow of Fraud

The sheer amount of money circulating in the UK car insurance market puts everything into perspective. It explains why verifying claims and stamping out fraud have become top priorities for every insurer. When payouts run into the billions each quarter, the pressure to separate genuine claims from fraudulent ones is immense. These costs do not just eat into profits; they directly inflate the premiums every honest driver has to pay.

To really grasp the scale, look at the numbers. In the third quarter of 2023 alone, UK car insurers paid out a jaw-dropping £2.54 billion in claims. Over the full year, total claims hit £11.9 billion against £14.1 billion in premiums written—a figure that has jumped by 32% since 2019. These stats, highlighted in recent UK car insurance statistics and facts, show just how thin the margins are. Even tiny efficiencies in claims handling can make a massive difference.

This financial squeeze means every claim is under the microscope. The central challenge boils down to one simple question: can the loss be proven? This is where the divide between third-party and comprehensive cover creates very different opportunities for fraud.

How Fraudsters Exploit Different Policy Types

While fraud can happen with any policy, the deception itself often changes depending on what the cover includes. Each policy type presents its own unique headache for claims adjusters and fraud investigation teams.

A third-party only policy is, by design, focused entirely on the other person in an incident. This creates a perfect breeding ground for specific scams:

- Exaggerated Personal Injury Claims: This is the territory of 'crash for cash' schemes. Fraudsters stage or deliberately cause accidents to make claims for fake or wildly inflated injuries like whiplash. The difficulty in proving the true extent of such injuries costs the industry millions.

- Inflated Third-Party Vehicle Damage: A claimant might pad their repair estimate, adding pre-existing dents and scratches into the mix, knowing the policyholder's insurer is on the hook for the bill.

- Phantom Passenger Claims: It sounds unbelievable but people who were not even in the car at the time of the crash will try to file personal injury claims.

Comprehensive policies, which cover the policyholder’s own car and property, open up a different, but just as costly, playbook for fraud.

- Falsified Item Losses: A policyholder might claim expensive electronics or tools were stolen from their vehicle even though those items never existed. Without proof of ownership from the start of the policy, these claims are incredibly hard to challenge.

- Claim Embellishment: After a genuine accident, a policyholder might try to sneak pre-existing damage into their claim, hoping the insurer will cover repairs for unrelated scuffs and scrapes.

- 'After-the-Event' Fraud: This one is particularly brazen. Someone damages their own uninsured property, rushes to buy a comprehensive policy, waits a short while and then files a claim for the pre-existing damage.

The common thread tying all of these scams together is the lack of a verifiable record. Without solid proof of what assets a policyholder owned—and the condition they were in when the policy started—insurers are stuck in a reactive and expensive game of cat and mouse.

The Ripple Effect of Insurance Fraud

Insurance fraud is far from a victimless crime. It places a huge financial burden on the industry, forcing insurers to pour resources into investigations and legal battles. We break down the full economic impact in our guide on what insurance fraud really costs the industry.

Ultimately, these costs are passed straight on to honest customers. Every bogus payout adds to the rising tide of premiums for everyone, punishing the majority for the actions of a deceitful few. It is a reality that underscores the urgent need for a system that establishes proof from day one, effectively stopping fraud before a claim can even be made.

Navigating a Fragmented Underwriting and Claims Landscape

At first glance, the UK motor insurance market looks consolidated but pull back the curtain and you will find it is deeply fragmented. This creates some serious operational headaches for underwriting and claims departments, where a lack of standardisation opens the door to major inefficiencies and vulnerabilities.

While a few big names dominate the headlines, the reality is a sprawling ecosystem of competing companies. This means there is no single, unified approach to assessing risk or handling claims. This inconsistency is not just an internal process issue; it creates loopholes that fraudsters are becoming experts at exploiting.

This complex environment brings the vast differences in claims processing into sharp focus. Without a universal standard for verifying a loss, adjusters often face an uphill battle. This is especially true when trying to tell a legitimate third-party claim from an exaggerated one or simply validating that the items listed in a comprehensive claim even existed.

The Challenge of Inconsistent Processes

The fragmentation of the UK insurance market has a direct, tangible impact on operational consistency. Each insurer—and there are many—operates with its own set of underwriting rules, claims procedures and fraud detection protocols. This variation creates a system where the outcome of a claim can depend as much on the insurer's internal playbook as it does on the facts of the case.

Without a standardised, evidence-based system, proving a loss can become a subjective and often difficult task for everyone involved.

In an industry where trust is paramount, inconsistent processes erode confidence and increase costs for everyone. When claims adjusters cannot quickly and reliably verify information, claim lifecycles extend, operational expenses mount and the potential for fraudulent payouts grows.

This operational mess hits the bottom line hard. It slows down settlement times for honest customers while allowing fraudulent claims to slip through the cracks, ultimately pushing up premiums for all policyholders. There is an urgent need for scalable, reliable solutions that can bring a measure of consistency to a diverse and fiercely competitive industry.

Market Concentration vs. Operational Fragmentation

The scale of this challenge becomes clearer when you look at the market structure. As of 2024, the top 10 car insurance providers controlled 75% of the UK market, with Admiral Group alone holding a 13% share. Yet, the industry remains incredibly fractured, with 141 separate companies all competing for business.

This creates huge variations in how claims are handled. With average claim costs now at £3,293 , the financial stakes are incredibly high. For a deeper dive into these figures, you can read more about the UK car insurance market statistics .

This environment creates a paradox: a market that is concentrated at the top but operationally fragmented on the ground. A claim submitted to one insurer might be scrutinised using advanced analytics, while another might rely on more traditional, manual reviews. This inconsistency gives fraudsters a crucial advantage, as they can probe for and exploit the weakest link in the chain.

For insurers, this underscores the necessity of adopting robust, scalable solutions for rapid claim verification and fraud detection to remain both competitive and profitable.

Modernising Claims and Underwriting: The Power of Proof

At the heart of the debate between third-party only and comprehensive cover lies a fundamental challenge: provability . Insurers are in a constant tug-of-war, needing to rigorously validate claims while also being under pressure to settle them quickly and fairly. This tension reveals the urgent need to move beyond reactive investigation towards a more modern, proactive approach to verification.

The real issue is the lack of a reliable, indisputable record of what a policyholder owns—and its condition—the moment a policy begins. Without this baseline evidence, claims adjusters are left trying to reconstruct a picture after the fact. They have to rely on receipts, witness statements and often, just the policyholder’s word, which creates friction and leaves the door wide open for costly fraud.

What is needed is a new way of thinking, one that establishes a single source of truth right from the start. By creating an immutable, time-stamped inventory of assets at policy inception, insurers can completely change the dynamic of the claims process.

Giving Adjusters the Edge with Pre-emptive Evidence

Imagine a claims process where the adjuster is not starting from scratch. Instead, they already have a verified digital catalogue of the items being reported as stolen or damaged. This kind of pre-emptive evidence gives them the power to validate legitimate claims with incredible speed and accuracy. The weeks spent investigating whether an item even existed and in what condition are gone. They simply cross-reference the claim against the initial inventory.

This directly tackles the most common types of fraud plaguing comprehensive policies:

- Claim Embellishment: It is impossible to add pre-existing damage to a claim when there is a clear, time-stamped record of the item's original condition.

- Fabricated Losses: Claims for high-value items that were never owned are instantly invalidated, as they will not appear in the verified inception inventory.

The impact on operational efficiency is profound. With definitive proof in hand, claim lifecycles shrink dramatically and adjustment costs plummet. More importantly, it means honest customers get their payouts faster, which massively improves the claims experience and builds loyalty. This is the core of creating a more trusted system, as we explore in our article on why authentication is the missing piece in the future of insurance claims.

By embedding provability into the very start of the policy lifecycle, insurers can transform the claims process from a contentious negotiation into a simple act of verification. This not only cuts costs but also builds a foundation of trust with the policyholder.

A New Frontier for Underwriting

The benefits of a verifiable asset inventory do not stop at the claims department. This technology is a powerful new tool for underwriters, allowing them to assess risk with far greater precision without having to rely on expensive and time-consuming physical surveys.

To modernise these processes, it is vital to know how to turn raw, unstructured information into usable data. A good look into understanding data parsing shows just how critical this step is for converting policyholder photos and details into structured insights for risk assessment.

Using a tool like Proova, insurers can ask a policyholder to create a digital record of their assets during the application process. This gives underwriters a crystal-clear, verified view of the exact items and risks they are being asked to cover.

How Proova Works in Practice

Proova's mechanism is simple but incredibly effective. It lets policyholders use a mobile app to create an indisputable, time-stamped inventory of their assets when their policy starts. This digital record acts as a definitive baseline for the entire duration of the cover.

- For the Policyholder: The process is straightforward. They take pictures and add details of their valuable items, which are then cryptographically sealed and time-stamped to create a permanent, unalterable record.

- For the Claims Adjuster: When a claim is filed, the adjuster has immediate access to this verified inventory, letting them confirm ownership and condition in minutes, not weeks.

- For the Underwriter: The inventory offers a granular view of the risk being insured. This allows for more accurate premium calculations and removes the need for costly manual inspections on high-value policies.

This system tackles the provability problem head-on, effectively bridging the trust gap between third-party and comprehensive cover. It provides the digital certainty needed to process claims fairly and efficiently, reducing the financial fallout from fraud that ultimately drives up costs for every policyholder.

How Digital Proof Stops After-The-Event Fraud Cold

One of the most stubborn and expensive schemes insurers face is 'after-the-event' fraud. It is a particularly common headache with comprehensive cover, where the policyholder's own assets are protected. This type of deception hits the core weakness of traditional insurance models: the lack of verifiable proof of an item's condition at the moment a policy begins.

The scheme itself is infuriatingly simple. Someone damages an uninsured item—a laptop, a TV or even their car—and then buys a comprehensive policy. After letting a little time pass to look less suspicious, they file a claim for the damage that was already there. They are betting on the insurer’s inability to prove the damage happened before the cover was active.

This puts claims adjusters in a truly impossible spot. Lacking concrete evidence of the item's condition when the policy started, they are left with a terrible choice. Either they launch a costly, time-consuming investigation or they pay out a claim that just does not feel right. This vulnerability is a massive drain on resources and is a direct reason why honest customers end up paying higher premiums.

Creating an Unbreakable Chain of Evidence

The only real way to stop this kind of fraud is to establish an irrefutable, time-stamped record of an asset's existence and condition from day one. This is exactly where Proova's technology comes in, creating a new standard of digital certainty that makes after-the-event fraud practically impossible to get away with.

By prompting the policyholder to create a digital inventory right at the start of their cover, Proova builds a verifiable baseline. It is a simple, proactive step that completely flips the script on the claims dynamic.

When a policyholder creates a time-stamped, unalterable digital record of their assets at inception, they are not just buying insurance; they are establishing a verifiable truth. This truth becomes the insurer's most powerful tool in differentiating between legitimate losses and outright fraud.

This pre-emptive evidence gives adjusters the power to reject fraudulent claims with complete confidence, backed by solid, indisputable proof. It closes a loophole that fraudsters have exploited for years, protecting insurers from preventable losses and preserving the integrity of the whole claims system.

The Role of Technology in Proactive Prevention

Achieving this level of digital certainty relies on modern technology. While advanced systems like machine learning fraud detection are becoming vital for spotting suspicious patterns, they work best when they are fed foundational, verifiable data at the policy level.

Proova provides this crucial data layer, offering concrete evidence that stops fraud before a claim can even be fully processed. It delivers the digital certainty needed to solve the fundamental challenges of provability that sit at the very centre of the third party insurance vs comprehensive debate, ensuring fairness and stability for the entire industry.

Frequently Asked Questions

When you get down to the brass tacks of insurance, the differences between policies often spark some important questions. Here are a few common queries that come up, especially when we are talking about proving claims and preventing fraud in the UK market.

Getting these details right is fundamental to giving clients solid advice and managing risk across a portfolio. It is also why a simple price check often misses the bigger picture of what a client could be exposed to financially.

Why Is Comprehensive Cover Sometimes Cheaper Than Third-Party?

It seems backwards, does it not? More cover for less money. This strange pricing is all down to how insurers profile risk. Actuarial data has shown, time and again, that drivers who choose comprehensive cover tend to be more careful and, statistically, are less likely to file a claim.

Insurers build their pricing models around this perceived lower risk. The result is the counter-intuitive scenario where broader protection can actually come with a lower premium. It is a perfect example of why underwriting should be guided by behavioural data, not just the level of cover someone picks.

How Does Fraud Differ Between These Policy Types?

Fraud looks very different depending on the policy. With third-party only policies, the risk is all about claims coming from the other person involved. This makes it a prime target for organised scams like staged 'crash for cash' incidents or wildly exaggerated personal injury claims.

Comprehensive policies, on the other hand, are more susceptible to 'after-the-event' fraud. This is where someone buys a policy after their phone screen has already cracked or they embellish a claim by adding non-existent items to a list of stolen goods. This fundamental difference in fraud tactics really shapes the entire third party insurance vs comprehensive debate for anyone managing risk.

The core problem in fighting insurance fraud, no matter the policy, is the lack of verifiable proof. Without a concrete record of an item's existence and condition when the policy starts, insurers are stuck in a reactive, expensive cycle of investigation.

What Is The Biggest Hurdle In Verifying Claims?

The single biggest challenge is establishing a baseline of truth. When a claim comes in, an adjuster has to figure out what was actually lost or damaged and what condition it was in before the incident.

Right now, that process relies on things like receipts, old photos and human memory, which is inefficient and easy to manipulate. This absence of a time-stamped, unalterable inventory at the start of a policy creates a 'provability gap' that fraudsters love to exploit. It inflates operational costs and, ultimately, drives up premiums for honest customers. This lack of initial proof is the weakest link in the entire claims chain.

By creating a verifiable record of assets from day one, Proova gives insurers the digital certainty needed to close these gaps. Our platform helps neutralise after-the-event fraud, validate claims far more quickly and underwrite with greater precision. Find out how you can modernise your claims and underwriting at https://www.proova.com.