The True Cost of Insurance Fraud in the UK

Insurance fraud is far more than just an item on a company's balance sheet. It is a calculated deception that siphons billions from the UK economy every single year and who foots the bill? Honest policyholders through higher premiums. It is not a victimless crime; it is a serious offence with a financial impact that touches us all.

The Real Cost of Insurance Fraud

Many people write off insurance fraud as a harmless fudge. A small exaggeration here, a little white lie there – surely a massive corporation can handle it? This is a dangerous misunderstanding. In reality every single fraudulent claim sends ripples across the entire economy, affecting honest individuals and businesses alike. The provability of claims is central to a fair system and fraud undermines this core principle.

The scale of this problem is staggering. The Association of British Insurers (ABI) consistently reports that detected fraud costs billions annually but that is just the scams they catch; the true figure is certainly much higher. Understanding this impact is crucial not just for the public but for the financial resilience of insurance companies themselves. The cost to all of us and the industry is immense.

The Two Faces of Insurance Fraud

When you get down to it, insurance fraud really boils down to two main types. Each one comes from a different place and uses different methods but both end up costing everyone money. Understanding the distinction is the first step to seeing just how widespread the issue really is.

Let's break down the key differences.

The Two Faces of Insurance Fraud

| Type of Fraud | Core Motive | Common Example |

|---|---|---|

| Hard Fraud | Premeditated Deception | Staging a car crash or faking a burglary to get a payout. |

| Soft Fraud | Opportunistic Exaggeration | Adding a non-existent laptop to a genuine burglary claim. |

While hard fraud often involves organised criminal activity, soft fraud is much more common and is usually committed by ordinary people who spot a chance to bend the truth after a legitimate incident.

Both types, however, poison the well.

Think of the insurance system as a shared financial pool. Every false or inflated claim is a dishonest withdrawal. When fraudsters take more than their fair share everyone else has to chip in more to keep the pool full. That's why your premiums go up.

This isn't just theory. It's a real, tangible cost added to your policy. The money paid out for fraudulent claims has to come from somewhere and it is recovered by increasing the price of cover for everyone. In effect honest customers are subsidising crime, paying a hidden 'fraud tax' on their motor, home and business insurance every single year.

Exposing Common Fraud Schemes and Tactics

To get a handle on insurance fraud, you first have to understand the playbook. Fraudsters are not one-trick ponies; their schemes range from simple, opportunistic lies all the way to highly coordinated criminal operations. Getting to know their most common methods is the first step in tackling the huge challenge facing the UK insurance market.

The tactics used are surprisingly varied, with different sectors targeted by specific types of deception. Motor insurance for instance has always been a prime target for elaborate scams cooked up purely to exploit the claims process. These are not just slightly exaggerated claims – they are often premeditated crimes.

Notorious Motor Insurance Scams

One of the most infamous schemes is the 'crash for cash' incident. In these setups criminals deliberately cause collisions with innocent drivers. They might slam on their brakes for no reason or flash their lights to let someone out of a junction only to hit them intentionally. The whole point is to make it look like the victim was at fault, allowing the fraudsters to file bogus claims for vehicle damage, personal injury and a whole host of other costs. You can learn more about how to spot and avoid these dangers in our guide to the persistent threat of 'crash for cash' scams.

Another growing problem is 'ghost broking' . This is where fraudsters pose as legitimate insurance brokers, usually on social media, selling forged or completely invalid policies to unsuspecting drivers. The victims think they've found a great deal on cover but only discover they are uninsured when they actually need to make a claim or get stopped by the police.

Deception in Property Insurance

The property sector is also a hotbed for fraud. At the more extreme end you have staged events like fake burglaries or, in the most severe cases, arson committed just to cash in on an insurance policy. These acts of hard fraud involve fabricating a loss event from thin air.

But a far more common issue is the opportunistic exaggeration of a genuine claim. Imagine a real storm or a burst pipe damages a home. The policyholder might be tempted to add a few items to their claim that were not actually damaged or maybe they will inflate the value of the goods they lost. This type of soft fraud is often seen as a victimless crime but it adds up, contributing massively to the overall cost of fraud for everyone.

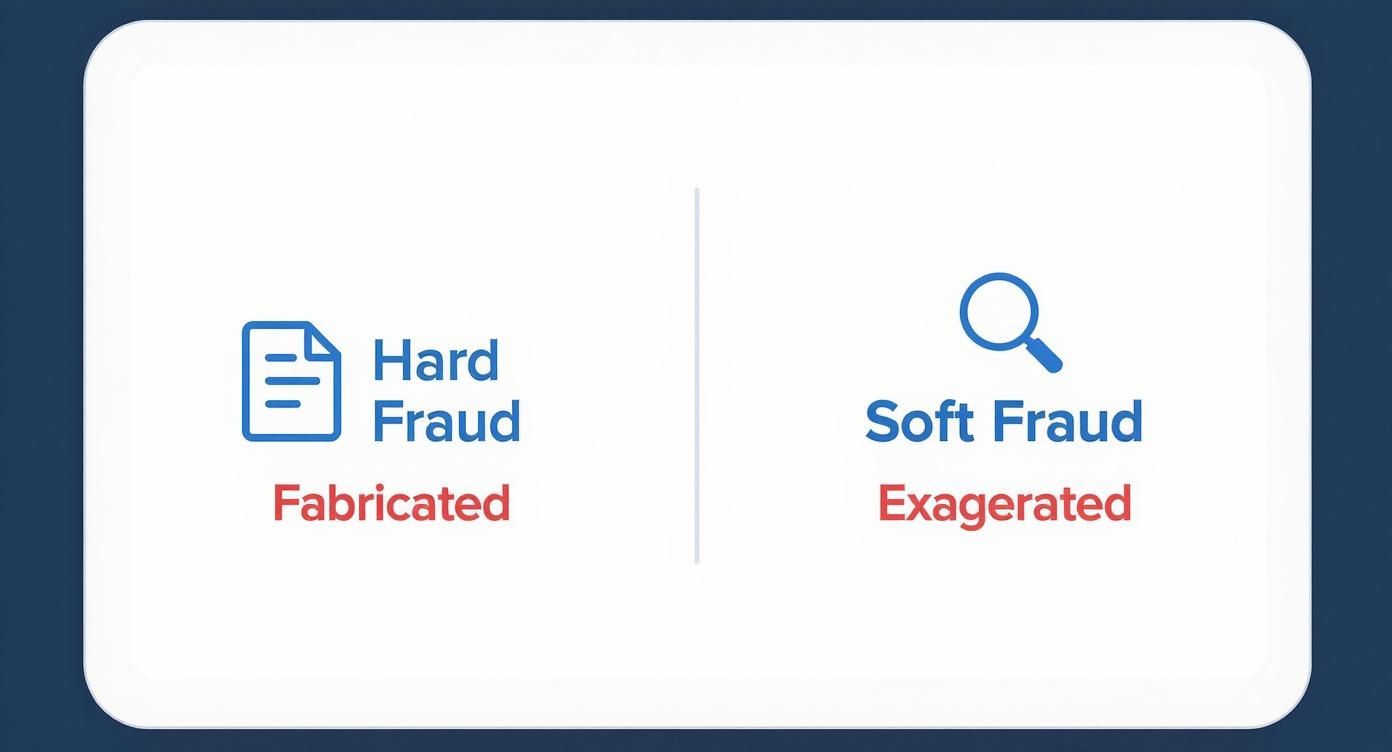

The infographic below really nails the difference between these two categories.

As you can see, hard fraud is pure invention while soft fraud starts with a real situation and stretches the truth.

The Problem of Application Fraud

Fraud isn't just limited to the claims process; it often starts the second someone applies for a policy. Application fraud is when an individual deliberately gives false information to an insurer to get a cheaper premium. This could be as simple as providing an incorrect address in a lower-risk postcode or "forgetting" to declare previous driving convictions.

While it might seem like a small fib withholding crucial facts is a form of deception. It completely undermines the principle of insurance, which is built on an honest assessment of risk. When that risk is miscalculated the entire financial model starts to wobble.

The scale of all this combined is immense. The UK insurance industry was hit with a staggering £1.16 billion in fraudulent general insurance claims during 2024, a 2% jump from the previous year. This problem affected over 98,400 individual fraud-related claims with motor insurance being the biggest target, making up 53% of all detected fraudulent claims.

This relentless rise in scams is precisely why recognising the tactics used by fraudsters has never been more critical – for both insurers and honest customers.

How Fraudulent Claims Inflate Your Premiums

It’s easy to think of insurance fraud as a victimless crime—a small fib told to a huge, faceless corporation. But that couldn't be further from the truth. The reality is that the multi-billion-pound cost of fraud isn’t just absorbed by insurers; it is passed directly to honest customers like you through higher premiums.

This creates a hidden "fraud tax" that everyone ends up paying. The connection between a dishonest claim and the price of your policy is direct and unavoidable. When insurers pay out on bogus claims they have to recover that money somehow. The main way they do this is by raising prices for everyone.

The Shared Community Fund Analogy

Think of the entire insurance system as a large, shared community fund. Everyone with a policy pays into this central pot of money. When someone in the community suffers a genuine loss—a house fire, a car accident—they can make a withdrawal from the fund to get back on their feet.

The system works beautifully when everyone is honest but insurance fraud is like someone sneaking an unauthorised withdrawal. The fraudster might invent a loss that never happened or simply inflate the value of a real one. Either way they are taking money they are not entitled to and the shared fund shrinks.

To keep the fund healthy enough to cover future, legitimate claims every other member has to chip in a bit more. That’s the core principle right there. Dishonest withdrawals force honest contributors to pay more, which translates directly into higher insurance premiums for you.

And this isn't a small problem. The scale of the financial damage is staggering. We've explored this in detail, breaking down how insurance fraud has become a £308 billion problem for the global industry, with the UK feeling a major part of that impact.

The Hidden Costs of Fighting Fraud

On top of the direct cost of paying fraudulent claims there are massive secondary expenses that also drive up your premiums. Insurers cannot just sit back and let fraud happen; they have to actively fight it and that fight is expensive.

These operational costs add yet another layer to the financial burden passed on to honest policyholders.

- Advanced Technology Investment: Insurers spend a fortune on data analytics and AI systems designed to spot suspicious patterns and red flags that might point to fraud.

- Specialist Investigation Teams: They have to fund dedicated counter-fraud teams, staffed with investigators and analysts whose entire job is to scrutinise questionable claims.

- Legal and Prosecution Costs: Taking fraudsters to court is a costly but essential process to deter others from trying the same thing.

- Industry Collaboration: Insurers also fund industry-wide bodies like the Insurance Fraud Bureau (IFB), which pools data to uncover organised crime rings.

All of these anti-fraud measures are baked into an insurer's operating costs. So a slice of every premium you pay goes towards funding this constant battle against deception.

System-Wide Delays and Inefficiency

The fallout from insurance fraud isn't just financial—it gums up the works for the entire claims process. When fraud becomes common insurers have no choice but to be more cautious with every single claim. This caution leads to longer verification processes and tougher checks for everyone, even those with perfectly legitimate claims.

What does that mean for you? It means your genuine claim could take much longer to be approved and paid out simply because resources are tied up investigating potentially dishonest ones. The time and effort spent weeding out fraud slows the whole system down, creating delays and frustration for honest customers who just need support.

Ultimately insurance fraud doesn't just cost you money. It costs you time and peace of mind too.

Inside the Fight Against Insurance Fraud

Insurers are in a constant, high-stakes battle against fraudsters. This isn't a passive waiting game; it is an active, multi-layered defence that blends powerful technology with seasoned human expertise to keep the entire insurance system honest. The mission is clear: spot suspicious claims, investigate them meticulously and stop fraudulent payouts before they happen.

The first line of defence has gone digital. Insurers now deploy sophisticated data analytics and AI to sift through thousands of claims daily, trained to spot the subtle red flags that even a sharp human eye might miss. Think of it as a digital tripwire.

A sudden cluster of claims from one neighbourhood, clashing details across different documents or a claimant with a history of small, frequent claims can all trigger an instant alert. This tech doesn't replace investigators—it points them exactly where to look.

The Investigative Process Uncovered

Once an algorithm flags a claim it's handed over to a human investigator. This is where gut instinct and deep experience come into play, as a team of specialists begins the painstaking work of piecing together the truth.

The process typically unfolds in a few key stages:

- Initial Review by Claims Handlers: The first person to see the flagged claim is usually the claims handler. They’ll take a closer look at the policy and the evidence provided, searching for any obvious inconsistencies.

- Referral to Specialist Investigators: If things still don’t feel right the case is escalated to a dedicated counter-fraud team. These are the experts trained to dig deep, run background checks and compare the claim against known fraud patterns.

- Deployment of Loss Adjusters: For larger property or complex commercial claims an independent loss adjuster might be sent to the scene. Their job is to assess the damage firsthand, confirm the details and interview the policyholder to make sure everything adds up.

This human touch is absolutely vital. Investigators conduct interviews, connect dots and use their hard-won experience to separate genuine hardship from calculated deception. To strengthen their defences many organisations use tools like KYC document collection software to reduce fraud to verify identities and documents right from the start.

Red Flags That Trigger a Fraud Investigation

Investigators are trained to look for specific signs that suggest a claim might not be legitimate. While one red flag might be a coincidence a combination of them often points to a problem that needs a closer look.

| Indicator Category | Specific Red Flags |

|---|---|

| Claimant Behaviour | Unusually calm after a major loss. Overly knowledgeable about insurance processes. Eager for a quick, low-value settlement. |

| Timing & Circumstances | Claim filed very soon after the policy was taken out. Incident occurs just before the policy is due to expire. The loss happens at an odd time, like late at night with no witnesses. |

| Documentation Issues | Submitted documents appear altered or forged. Receipts are handwritten or look unprofessional. Vague descriptions of what was lost or damaged. |

| Claim History | Multiple similar claims filed in the past. History of frequent claims across different insurers. |

| Witness & Third-Party Info | Witnesses provide conflicting stories or change their accounts. Third parties (like repair shops) have a reputation for fraud. |

These indicators help investigators prioritise their efforts, focusing on the claims that truly warrant a deeper dive.

The Power of Industry-Wide Collaboration

No single insurer can win this fight on its own. Organised crime rings in particular often hit multiple companies at once, banking on their fragmented view to stay hidden. That’s why sharing intelligence across the industry has become a game-changer.

Organisations like the Insurance Fraud Bureau (IFB) act as a central hub for this kind of collaboration. When insurers feed suspicious claims into the IFB its systems connect the dots between what might otherwise look like isolated incidents.

A single "crash for cash" claim might look like a simple accident. But when the IFB's database links the same people, vehicles and addresses to a dozen similar incidents across multiple insurers a clear pattern of organised crime snaps into focus.

This unified approach is essential for uncovering large-scale scams that would otherwise fly under the radar. And the data shows the problem is only getting bigger. The first half of 2025 saw a shocking spike in detected fraud. Allianz UK alone identified £92.6 million in fraudulent activity from over 15,800 cases—that's a 34% jump from the same period in 2024. Aviva’s team also stopped over 6,000 fraudulent claims worth more than £60 million , preventing over £334,000 in fraud every single day.

You can discover more insights about these escalating fraud trends in 2025. This technology-driven, collaborative approach is no longer just an option; it is the only way to combat such a rapidly growing financial crime.

The Life-Altering Consequences of Getting Caught

Being caught for insurance fraud is far more than just a denied claim. It is a criminal offence with severe, long-term consequences that can derail every part of your life. While some people see exaggerating a claim as a harmless fib the reality is it is a high-risk gamble with life-altering stakes.

The fallout begins the moment you are found out. The first and most obvious outcome is that the fraudulent claim gets rejected and your insurance policy is cancelled. This alone can leave you financially exposed, particularly if the original loss was genuine but you decided to embellish it.

Beyond a Denied Claim

But the consequences quickly escalate well beyond a simple policy cancellation. Once you are identified as a fraudster your details are often added to industry-wide databases. The most prominent of these is the Insurance Fraud Register (IFR) , a shared resource that insurers across the UK rely on.

Being listed on the IFR is like a permanent black mark against your name. It makes it incredibly difficult and much more expensive to get any kind of insurance in the future. And this doesn't just apply to the type of policy you defrauded; it can poison your ability to get cover for your car, home or business.

The impact of a fraud conviction extends far beyond the insurance world. It can severely damage your credit rating, making it harder to secure a mortgage, obtain a loan or even get a mobile phone contract. A record of financial dishonesty creates a ripple effect that touches almost every part of modern life.

This digital footprint of dishonesty can follow you for years, slamming doors on financial opportunities that most people take for granted.

The Escalation to Criminal Prosecution

For more serious cases of insurance fraud the penalties become far more severe. This isn't just a civil matter; it is a crime that can easily lead to prosecution. If you're convicted you face a range of penalties that reflect just how seriously the offence is taken.

These can include:

- Substantial Fines: Courts can impose fines that dwarf the value of the original fraudulent claim, creating a devastating financial burden.

- A Permanent Criminal Record: This can lock you out of certain careers, especially in fields like finance, law or any role that needs a background check.

- Prison Sentences: For the most serious and organised fraud schemes a custodial sentence is a very real possibility.

The justice system is taking an increasingly firm stance on financial crime. The consequences for offenders are mounting; prison sentences resulting from fraudulent insurance claims detected by Aviva in 2025 have already surpassed a cumulative total of 32 years of custodial and suspended sentences. That's a nine-year increase compared to the entire total handed down in 2024. You can learn more about these rising penalties for insurance fraud.

Ultimately what might start as a seemingly small deception can easily spiral into a life-changing conviction, with consequences that last a lifetime.

Strengthening Claims with Proactive Proof

When something goes wrong—a fire, a break-in—the last thing anyone wants is a long, drawn-out battle to prove what they owned. Yet in a world where insurance fraud is always a threat, the burden of proof often falls squarely on the policyholder's shoulders. Trying to remember every single lost item, let alone find a receipt for it, is a huge ask after a traumatic event.

This lack of provability doesn't just create stress and delays. It also opens the door for fraudulent claims to slip through the cracks.

But what if the evidence was already locked in, long before anything bad ever happened? That's the simple idea behind proactive proof. By creating a secure, digital record of your possessions beforehand, the entire claims process transforms from a point of friction into a straightforward verification. The dynamic shifts from suspicion to trust.

From Ambiguity to Certainty

The old way of handling claims relies on fading memories and dusty receipts stuffed in a drawer somewhere. An authenticated-item database changes the game completely. It lets you build an unchangeable, time-stamped inventory of your valuables, backed up with photos, serial numbers and proof of their condition.

This simple step establishes a clear, verifiable baseline of what you own. It is like having an impartial digital witness that can’t be argued with, giving both you and your insurer a single source of truth. The knock-on effects are huge for everyone involved.

- For Honest Policyholders: It means a faster, smoother and far less stressful claims journey. When the proof is already on file the process is about validation, not investigation, which means getting paid out quicker.

- For Insurers: It massively shrinks the opportunity for both soft and hard insurance fraud . Claims for items that never existed become impossible and exaggerated values are easy to spot, protecting the entire claims pool.

By taking the guesswork out of the process, proactive verification builds a more transparent and trustworthy relationship between customers and their insurers. It empowers honest people while shutting the door on fraudsters.

The Power of Pre-emptive Proof

Ultimately this proactive approach makes the entire insurance model stronger. For insurers it means they can settle legitimate claims with speed and confidence, knowing the loss is genuine and accurately documented. It's also a powerful tool for underwriting, helping them assess risk with greater accuracy right from the start. You can learn more about fighting fraud before it happens with the power of verified evidence.

For genuine customers it provides priceless peace of mind. Knowing your most valued possessions are properly documented and their ownership is indisputable removes a massive layer of anxiety. In the ongoing fight against rising insurance fraud, having clear, proactive proof is the most effective tool an honest policyholder can possibly have.

Your Questions on Insurance Fraud Answered

When you're dealing with insurance it's natural for questions to pop up, especially around a serious topic like fraud. We've pulled together some of the most common queries to give you clear, straightforward answers about how this crime works, who it really affects and what the consequences are.

This isn't about legal jargon or complicated definitions. It's about understanding the real-world impact of fraud on everyone.

What Is the Real Cost of Insurance Fraud?

The biggest cost of insurance fraud lands squarely on the shoulders of honest policyholders. When an insurer pays a fraudulent claim that money has to be recovered somehow for the business to remain stable. The way they do this is by increasing premiums for everyone else.

In short every honest person with a policy is paying a hidden 'fraud tax'. This isn't just to cover the bogus payouts themselves; it also funds the expensive business of fighting fraud, from hiring specialist investigators to investing in new detection technology.

Where Does Most Insurance Fraud Happen?

While fraud can happen anywhere it isn't spread evenly. In fact deep dives into the data show it often clusters in specific areas. A detailed geographic analysis by the Insurance Fraud Bureau, which looked at over 2.4 million policies, identified clear fraud hotspots right across the UK.

In England postcodes within West Yorkshire, Greater Manchester and the West Midlands lit up as areas with the highest rates of fraudulent activity. This kind of pattern often points to organised criminal networks running coordinated scams. The analysis also flagged Glasgow as the main area of concern in Scotland, while the Isle of Anglesey in Wales and County Fermanagh in Northern Ireland topped their respective lists. You can read the full research about these UK fraud hotspots for a closer look.

Can I Go to Prison for a Minor Exaggeration?

Yes, absolutely. Any deliberate lie to get a financial advantage from an insurance policy is a criminal offence, no matter how small the amount. A minor exaggeration might not land you in prison on its own but it can easily lead to a criminal record, hefty fines and being blacklisted by insurers, making it incredibly difficult to get cover in the future.

For more serious deception or if it's a repeated offence a prison sentence is a very real possibility. The justice system is getting tougher on financial crime, which means that what might seem like a tiny fib can have life-changing legal consequences.

At the end of the day there’s no such thing as a "harmless" bit of insurance fraud. Every single instance adds to the problem and comes with a massive personal risk.

At Proova , we believe proving what you own shouldn't be a battle. Our platform creates an unchangeable, time-stamped record of your possessions, which makes genuine claims faster and fraudulent ones much harder to pull off. Secure your assets and get a smoother claims process by visiting https://www.proova.com to see how it works.