How Much Contents Insurance Do I Need: A UK Guide

Figuring out how much contents insurance you need is straightforward in theory: you need enough cover to replace everything you own with a brand-new version. That means the final number should cover the cost of buying every single item again—from your sofa and TV to your clothes and cutlery—at today’s prices.

The Real Cost of Guessing Your Contents Value

Working out your contents cover can feel like a chore but getting it wrong can have serious financial consequences. It is a common pitfall. Many households unintentionally underinsure themselves, leaving a massive gap between their policy limit and the true cost of replacing everything after something like a fire or a burglary. We often forget the smaller things but they can easily add up to thousands of pounds.

On the other hand, over-insuring means you are just throwing money away on premiums for protection you will never use. You are paying for a level of cover that goes way beyond what your stuff is actually worth and an insurer will only ever pay out the proven value of what you lost. Finding that sweet spot is crucial for both your peace of mind and your bank balance.

The Wider Impact of Inaccurate Valuations

The problem goes beyond just your personal financial risk. Inaccurate valuations are directly linked to the ongoing problem of insurance fraud. When claims are submitted with guessed or inflated values, it forces insurers to spend more time and resources digging into every single detail to verify the claim's legitimacy.

This friction does not just slow down the claims process for honest policyholders; it also drives up operational costs across the entire industry. And where do those costs end up? They get passed on to all of us in the form of higher premiums. So, getting your valuation right is not just about protecting yourself—it is about contributing to a fairer, more affordable insurance system for everyone.

By providing a provable, accurate inventory of your possessions from the very beginning, you help tackle the very issues that make insurance more expensive. It shows transparency and removes the ambiguity that fraudulent claims often hide behind.

This level of accuracy is especially important in a market seeing so much activity. According to the Association of British Insurers (ABI), a staggering £1.6 billion was paid out in property and contents claims during the second quarter of 2025 alone. Despite these rising costs, the average contents-only premium was just £129 annually , which shows how competitive the market is and why every pound counts. You can read more about the latest insurance claim trends over on the ABI website.

While contents insurance provides that vital financial safety net, it is also worth understanding how proactive loss prevention services can help safeguard your assets in the first place, minimising the chance you will ever need to claim.

A Practical Method For Valuing Your Possessions

Before you can figure out how much contents insurance you need, you first have to get a realistic picture of what you actually own. The best way to do this is a straightforward, room-by-room inventory. This is not just about noting down the big-ticket items like your television or sofa; it is about creating a complete, provable record of all your belongings.

Taking this detailed approach is your strongest defence against underinsurance . It is incredibly easy to underestimate the combined value of all your smaller possessions. Just think about your kitchen for a moment—the air fryer, coffee machine, stand mixer and all those utensils can quickly add up to a surprising amount. A proper inventory makes sure you account for everything.

Starting Your Room-by-Room Inventory

I always tell people to just start in one room. Let's say, the living room. List everything you see, starting with the obvious: furniture, electronics and any art or decorative pieces. Once that is done, look closer. What about the things people usually miss? Your book collection, Blu-rays or video games and even expensive textiles like custom-made curtains or a quality rug. You will need to repeat this process for every single room and do not forget the loft, garage or shed.

A good way to keep on top of this is by keeping meticulous records, much like you would when organizing your receipts for tax purposes. These days, technology makes this far easier. An inventory app on your smartphone lets you photograph each item and attach digital copies of receipts, creating a verifiable log for your insurer right there and then.

This level of detailed proof becomes invaluable if you ever have to make a claim. It clearly establishes what you owned and what it was worth, which helps combat the fraudulent claims that unfortunately drive up insurance costs for everyone.

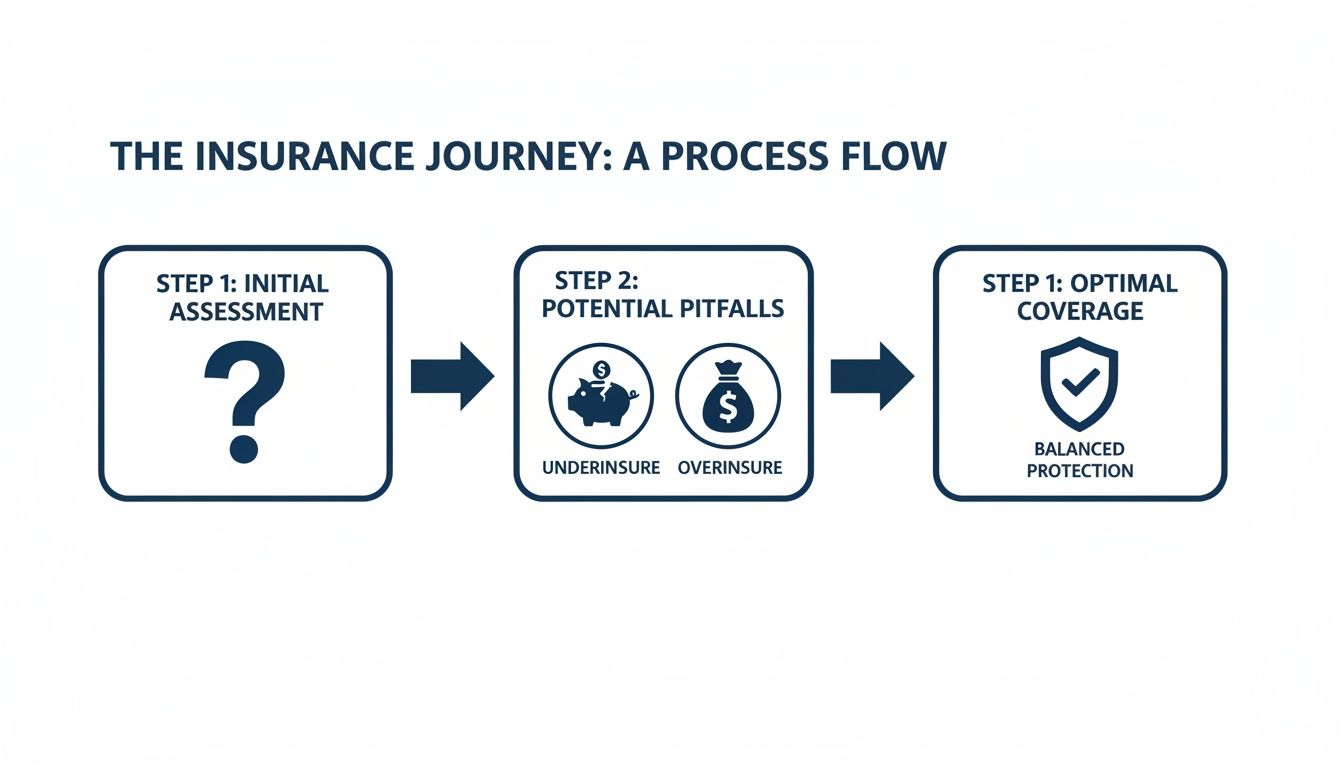

The process flow below highlights the common pitfalls of simply guessing your contents' value—a shortcut that often leads to being underinsured or even overinsured.

As you can see, a guess is rarely accurate. It can leave you financially exposed when you need support the most or you could end up paying for cover you simply do not need.

The Importance of Proof and Verification

Making a detailed list is one thing but proving the value of your items is just as crucial. Insurers need evidence to process a claim efficiently and fairly and this is where your diligent record-keeping really pays off.

A verifiable inventory, complete with photos and receipts, does not just speed up your claim—it reinforces its legitimacy. It removes any guesswork and helps your insurer distinguish your genuine claim from a potentially fraudulent one.

Without proof, you are essentially asking your insurer to take your word for it, which can easily lead to delays and disputes. Think about it in practical terms:

- Electronics: Keep receipts for your laptop, tablet and TV. Photos showing their serial numbers and condition are brilliant evidence.

- Furniture: Store the invoices for major purchases like your sofa, bed frames and dining table.

- Clothing: Designer clothes, shoes and handbags can be worth thousands. Photograph your collection and hold on to any proof of purchase you have.

Many people get a real shock when they finally tally up the true replacement cost of everything they own. If you are curious about what others typically have, our detailed guide on the UK average house contents value explained offers some useful insights.

By taking this systematic, evidence-based approach, you can be confident you have the right level of cover. It protects you from financial loss and also contributes to a more transparent and fair insurance system for all.

Room-By-Room Inventory Checklist

To help you get started, I have put together a simple checklist. It covers some of the most common items found in each room, along with a few things that people frequently forget to include in their valuation.

| Room | Common Items to Value | Often Forgotten Items |

|---|---|---|

| Living Room | Sofa, TV, coffee table, sound system, shelving units | Books, Blu-rays/DVDs, video games, lamps, curtains, rugs, photo frames |

| Kitchen | Fridge/freezer, oven, microwave, dishwasher, washing machine | Cutlery, crockery, glassware, small appliances (kettle, toaster), cookware |

| Bedroom(s) | Bed frame, mattress, wardrobes, chests of drawers, bedside tables | Bedding, clothes, shoes, jewellery, watches, mirrors, artwork |

| Bathroom | Storage units, mirrors, decorative items | Towels, electric toothbrushes, designer toiletries, bath mats |

| Home Office | Desk, office chair, computer, printer, monitors | Software licences, stationery, desk lamps, filing cabinets |

| Loft/Garage/Shed | Stored furniture, DIY tools, sports equipment, bicycles | Camping gear, luggage, Christmas decorations, garden furniture, lawnmower |

This checklist is not exhaustive, of course, but it is a solid starting point. The key is to be methodical and thorough—your future self will thank you for it if you ever need to make a claim.

Choosing Between New For Old And Indemnity Cover

Once you have put together a detailed inventory of your possessions, the next crucial step is getting to grips with how insurers actually value those items when you make a claim. This is a detail you cannot afford to overlook. The difference between the two main methods can mean getting thousands of pounds back or just a fraction of what you lost.

The two types of cover are ‘new for old’ and ‘indemnity’ . Most standard policies in the UK are thankfully new for old but it is vital to check the small print. Knowing exactly what you are signing up for is non-negotiable.

Understanding New For Old Cover

New for old cover, often called 'replacement cost' cover, is exactly what it sounds like. If your five-year-old television is stolen or destroyed, your insurer pays out enough for you to go out and buy a brand-new, equivalent model today.

It does not matter that your old one was used. The policy is designed to put you back in the exact position you were in before the loss, without you having to dip into your savings. This is almost always the best option for policyholders, giving you complete peace of mind that you can fully replace your belongings.

The Pitfall of Indemnity Cover

Indemnity cover, or 'actual cash value', works very differently. This type of policy only pays out what an item was worth at the moment it was lost or damaged. The insurer will calculate its current value by factoring in wear, tear and depreciation over time.

Let's use a real-world example to see just how stark the contrast is:

- Scenario: Your three-year-old laptop, which you bought for £1,000, is destroyed in a house fire.

- New for old cover: The insurer would pay out the cost of a brand-new, similar-spec laptop, which might still be around £1,000 .

- Indemnity cover: The insurer might decide the laptop had depreciated by 60% and was only worth £400 . That is all you would receive.

The difference is stark. Indemnity cover leaves you with a £600 gap you would have to fund yourself just to get back to where you were. For this reason, always aim for a new for old policy.

This is especially important given the rising cost of goods. UK home insurance premiums have seen complex trends, with average combined premiums reaching around £231 by mid-2025. This pressure is partly due to a 21% rise in rebuild costs in recent years, which directly impacts replacement values and pushes insurers to adjust their pricing.

Regularly reassessing your cover is crucial to keep pace with these changes. It is well worth taking the time to understand more about why home insurance premiums are going up to stay informed.

Insuring Your High-Value and Unique Items Correctly

While your standard contents insurance policy is a great safety net, it is vital to know where its coverage ends. Most policies have what is called a ‘single article limit’ — a cap on how much the insurer will pay for any one item. This figure usually sits somewhere between £1,500 and £2,000 .

This is a detail that trips a lot of people up. If you own a high-end watch, a piece of art, an expensive bicycle or precious jewellery, it almost certainly will not be fully covered by a standard policy. Finding this out after a theft or fire can be a brutal financial shock, leaving you thousands of pounds out of pocket.

Identifying and Valuing Your Prized Possessions

First things first: you need to pinpoint every item you own that could be worth more than your policy’s single article limit. This is not like the general room-by-room inventory; this is about zooming in on your most significant assets, heirlooms and investments.

Look out for items that typically fall into these categories:

- Jewellery and Watches: Engagement rings, luxury watches and inherited family pieces almost always exceed the standard limit. Our guide on insurance for an engagement ring in the UK offers a much deeper look into protecting these items.

- Art and Antiques: Paintings, sculptures or antique furniture need a professional eye to determine their real market value.

- High-Spec Electronics: Think professional camera gear, custom-built gaming PCs or specialist audio equipment that can easily sail past the £2,000 mark.

- Designer Goods: That collection of designer handbags or shoes can add up to a surprisingly high figure when valued together.

- Bicycles and Sports Equipment: Serious road bikes or other high-performance sports gear often need to be specified on your policy.

Simply plucking a value out of thin air will not cut it. To make a successful claim, you need solid, documented proof of what your items are worth. This protects you from being underpaid and reassures the insurer that the claim is legitimate, distinguishing it from fraudulent attempts to claim for non-existent or overvalued items.

The Importance of Professional Valuations and Documentation

Once you have identified your high-value items, the next move is to get them professionally valued. For things like jewellery, art or antiques, this means finding a certified appraiser who can issue a formal valuation certificate. This document is the evidence your insurer will need.

A professional valuation acts as an impartial, verifiable record of an item's worth. It removes any guesswork and is a critical piece of evidence that substantiates your claim, helping to prevent the kind of inflated or fraudulent claims that drive up premiums for everyone.

With a valuation in hand, you must declare each of these items to your insurer. They will then be listed individually on your policy, usually for a small additional premium, ensuring they are covered for their full appraised value.

Finally, gather all your documentation — valuation certificates, original receipts and clear photographs — and keep them safe. Store physical copies somewhere secure and have digital backups in the cloud. This paperwork is your best defence, making sure your most treasured possessions are properly protected, no matter what happens.

Essential Insurance Advice For Renters

It is a common—and often costly—mistake for renters to think their landlord’s insurance has them covered. Let us be clear: it does not. The landlord's policy is designed to protect the building itself—the walls, the roof, the fixtures—but it does absolutely nothing for your personal belongings.

Imagine a fire or a flood. Your landlord can claim for repairs to the property but you would be left footing the bill to replace everything you own. We are talking about your laptop, clothes, furniture and kitchenware. It is a huge financial gamble that far too many renters take without even realising it.

Why Are Renters So Often Uninsured?

So, why do so many renters skip contents insurance? One of the biggest reasons is simply underestimating the value of their stuff. When you buy things gradually over years, it is easy to lose sight of their collective worth. The other common issue is a misplaced belief that they are already covered elsewhere.

This protection gap is becoming a real concern. In the UK, the number of renters with contents insurance has been on a downward slide, dropping from 51% in 2021 to just 46% in 2023 . This trend means a shocking number of households are financially exposed if disaster strikes.

Special Considerations For Shared Homes

Living in a shared flat or a house of multiple occupation (HMO) adds another layer of complexity to the insurance puzzle. Figuring out how much cover you need in this setup requires a slightly different game plan.

- Individual Policies: The simplest route is often to get a policy that just covers your own possessions, usually limited to your private room. This is a great option if your housemates are not on board with a group policy.

- Locks are Key: Insurers will almost always insist that your individual room has a lock on the door. Without one, you will likely find you are not covered for theft, which defeats a major purpose of the policy.

- Joint Policies: Some insurers do offer policies for housemates. However, this means everyone needs to be named on the policy and agree on the total value of contents throughout the entire property, not just in their own rooms.

If you are in higher education, the rules can be a bit different again. It is well worth checking out our dedicated guide on student home contents insurance for more tailored advice.

What About Working From Home?

The explosion of remote work has blurred the lines between personal and professional belongings. It is absolutely crucial to check whether your employer’s gear, like a company laptop or monitor, is covered under your personal contents policy.

Most standard contents insurance policies will not cover items owned by your employer. If that work laptop is stolen from your home, your personal policy is unlikely to pay out. Your employer should have their own business insurance to cover these assets.

If you run your own business from home or own your work equipment, you will probably need to add business cover to your policy or take out a completely separate business insurance policy. Always have this conversation with your insurer to make sure you are not left with a gap in your protection. Getting this right means you are properly covered for both your personal and professional life.

A Few Common Questions About Valuing Your Stuff

Even when you think you have got it all figured out, a few questions always pop up when it comes to contents insurance. Let us tackle some of the most common ones that people ask, cutting through the jargon to give you some straight answers.

Getting these details right is not just about ticking a box. It is about making sure your policy actually stands up and does its job if you ever need to make a claim.

How Often Should I Review My Contents Insurance?

You should really be giving your contents insurance a once-over at least once a year. Life moves fast and the value of your possessions changes with it. It is also a good idea to update your policy as soon as you buy anything significant, like a new high-end TV, a designer sofa or that piece of jewellery you have had your eye on.

An annual check-in makes sure your total cover keeps up with your life, stopping you from slipping into being underinsured without even realising it. It is a small job that can save you a massive financial headache later on.

What Happens If I'm Accidentally Underinsured?

This is a big one. If you file a claim and your insurer finds out you are underinsured, they will likely bring up something called the 'average clause'. In simple terms, it means they will only pay out a percentage of your claim, based on how much you were underinsured by.

Let's say you insured your contents for £20,000 but the real replacement value was closer to £40,000. That means you are 50% underinsured . If you then claim for £5,000 of stolen tech, the insurer might only pay out 50% of your claim —just £2,500. This is exactly why having a precise, evidence-backed inventory is so critical. It is your best defence against a nasty surprise like that.

Are Items In My Shed Or Garage Covered?

Most contents policies do cover items you keep in outbuildings like sheds and garages but there is a catch. The cover is usually capped at a much lower limit than your main policy—often somewhere between £1,000 and £2,500 .

Always dig into your policy documents to find the specific limits for outbuildings. If you are storing valuable kit like an expensive bike, a collection of power tools or a ride-on mower out there, you will almost certainly need to list them separately to get them fully covered.

Forget to declare them and you could be facing a huge shortfall if they are ever stolen or damaged. The lesson here, as with everything else, is to keep a detailed list and be upfront with your insurer. It builds a clear, transparent picture that helps avoid the kind of grey areas that lead to disputes or suspicions of fraud, which just ends up pushing up premiums for all of us.

Building and keeping a detailed, provable inventory is the single best thing you can do to get your contents insurance right. With a tool like Proova , you can create a secure digital log of everything you own, complete with photos, receipts and serial numbers. It gives both you and your insurer an undeniable record of your possessions, which helps speed up claims and eliminates the risk of being underinsured. Get some peace of mind by visiting https://www.proova.com to see how it all works.