Fronting Car Insurance The Costly Risk UK Drivers Take

Ever heard of fronting car insurance ? It is a term that comes up a lot, especially when parents are trying to help their children get on the road without breaking the bank.

At first glance, it seems like a savvy little trick. You list a more experienced, lower-risk driver—often a parent—as the main person using the car, then add the actual, higher-risk driver—like a son or daughter who just passed their test—as a 'named driver'. The result? A much cheaper premium.

But here is the catch: while it might feel like a harmless white lie to save some cash, fronting is actually a form of insurance fraud. And in the UK, it is illegal .

The Hard Truth About Fronting Car Insurance

Let us be honest, the temptation is completely understandable. New and young drivers often face eye-watering insurance quotes so the idea of putting Mum or Dad down as the main driver to slash the cost is appealing.

The problem is, this is not some clever loophole. It is a deliberate act of misrepresentation. You are giving the insurer a false picture of who really holds the risk and that fundamentally breaks the agreement you have with them.

Make no mistake, this is taken very seriously. Under the Fraud Act 2006 , fronting is not just a minor slip-up on a form; it is a criminal offence. The fallout can be huge, from having your policy instantly cancelled to facing a criminal record and in serious cases even prison. The provability of the claim is central; once an insurer establishes the deception, the consequences are unavoidable.

Main Driver vs Named Driver: What's the Difference?

To really grasp why fronting is such a big deal, you need to understand the clear distinction between a 'main driver' and a 'named driver'. An insurer calculates the premium almost entirely based on the risk profile of the main driver—the person who will be behind the wheel most of the time.

Getting this wrong is not just a technicality; it is the core of the contract.

"At its heart, fronting is a form of deceit. It deliberately misleads the insurer about who poses the greatest risk, undermining the entire basis of the insurance agreement. The financial fallout for those caught is often far greater than any initial savings."

So, who is who? Let us break down the roles and responsibilities to see why mixing them up has such serious consequences.

A Clear Comparison of Driver Roles

One of the most common points of confusion is figuring out who the real main driver is. It is not necessarily the person who owns the car or pays for the insurance. It is the person who uses it the most.

Think about it: who drives the car to work or university every day? Who does the weekly shop in it or uses it most weekends? That person is the main driver, period.

This simple table clarifies the distinct responsibilities:

Main Driver vs Named Driver What's the Difference

| Responsibility | Main Driver | Named Driver |

|---|---|---|

| Primary Use | The person who uses the vehicle most often. | An occasional, secondary user of the vehicle. |

| Insurance Premium | Their details are the primary factor in calculating the premium. | Their details have a smaller impact on the overall cost. |

| No-Claims Bonus | Earns their own no-claims bonus on the policy. | Does not typically earn a no-claims bonus on this policy. |

| Legal Status | Legally responsible for declaring their status accurately. | Must be declared but is not the central risk factor. |

When it comes down to it, honesty is the only way forward. While the cost of car insurance can feel daunting, the potential financial and legal devastation caused by fronting fraud is a far heavier price to pay.

And this deception does not just hurt the people involved. It contributes to rising insurance costs for every single honest driver on the road, creating a burden on the entire industry and all of us as consumers.

The Financial Pressures Driving the Fronting Gamble

It is easy to dismiss fronting as simple dishonesty. But to really get a grip on why so many people are tempted, you have to look at the harsh financial reality staring UK drivers in the face.

The truth is, soaring car insurance premiums are piling immense pressure on households, pushing some to consider desperate measures. This is not just a feeling; the numbers tell a stark story of rising costs that are hitting everyone.

These price hikes are not happening in a vacuum. They are a direct response to a perfect storm of economic factors that have made insuring vehicles much more expensive for the companies providing the cover. From the repair garage to the courtroom, the costs of getting a driver back on the road after an incident have shot up.

The Soaring Cost of Keeping Cars on the Road

At the heart of the issue is the ballooning cost of claims. Modern cars, crammed with sophisticated sensors, cameras and complex electronics, are a world away from the vehicles of a decade ago. They are also far more expensive to repair.

A simple bumper replacement is no longer a quick fix. It can now involve recalibrating multiple advanced driver-assistance systems, turning what was once a minor job into a costly and technical exercise.

This complexity has a direct knock-on effect on what insurers have to pay out. The average cost of a motor insurance claim rocketed from £2,410 in 2019 to £3,293 in 2023 —that is a staggering 37% increase . With repair costs making up roughly two-thirds of those payouts, it is no surprise that premiums have followed suit, jumping by around 40% over the same period. You can explore a detailed breakdown of these figures in the FCA's comprehensive review of the motor insurance market.

When the cost to repair a car after an accident spirals, insurers have to balance their books. That financial pressure is inevitably passed on to every policyholder, honest or not, through higher annual premiums.

This ripple effect means even drivers with spotless records are feeling the pinch. Throw in general inflation, which pushes up the cost of labour, courtesy cars and spare parts and you have a perfect recipe for unaffordable insurance.

Why Young Drivers Face the Steepest Climb

For young or newly qualified drivers, this financial pressure is magnified tenfold. They lack a long history of safe driving and statistically they are more likely to be involved in an accident. Insurers, naturally, place them in the highest risk categories.

The result? Premiums that can often cost more than their first car.

- Lack of Experience: Insurers have no data to prove a new driver is a safe bet, so they have to price in a higher level of risk.

- Higher Accident Rates: The statistics do not lie. Year after year, they show that drivers under 25 are involved in a disproportionately high number of serious accidents.

- No No-Claims Bonus: Without years of claim-free driving under their belt, they cannot access the significant discounts that reward more experienced motorists.

This creates a formidable barrier for anyone just starting out. For many young people, driving is not a luxury—it is a necessity for getting to college, work and gaining independence. Faced with quotes running into thousands of pounds, the apparent "saving" from fronting car insurance can feel like the only way forward, even though it is fraud.

While you can understand the temptation, it is a gamble where the potential losses—a cancelled policy, a criminal record and personal liability for huge claims—dwarf any initial financial relief.

That little thrill of saving a few hundred quid on a premium? It can quickly spiral into a life-altering financial and legal nightmare. What starts as a seemingly small fib on an application form unravels dramatically the moment a claim needs to be made. Suddenly, the consequences of fronting car insurance become devastatingly real.

Picture this: the young, actual main driver has a minor prang. When the insurance company starts its standard investigation, inconsistencies begin to surface. Once they prove the policy was fronted, the fallout is swift and severe.

Your Policy Becomes Worthless

The very first thing an insurer will do is cancel the policy. And they will not just cancel it from that day forward—they will void it right back to the start date, treating it as if it never existed in the first place.

This has immediate and terrifying implications:

- The Claim Is Refused: The insurer will refuse to pay for any damages. This leaves both the parent and the young driver on the hook for every single penny. That could mean repairs to their own car, the other party's vehicle and potentially thousands in injury compensation.

- They'll Want Their Money Back: If any previous claims were paid out under the fraudulent policy, the insurer can legally demand you repay it all.

- You're Blacklisted: Both people involved will be added to industry databases like the CUE (Claims and Underwriting Exchange). This flags them as high-risk, making it incredibly difficult and eye-wateringly expensive to get any kind of insurance in the future.

These penalties alone can be financially crippling. But believe it or not, they are just the start.

From a White Lie to a Criminal Record

Fronting is not just a breach of your insurance contract; it is a form of fraud under the Fraud Act 2006 . This means the consequences go far beyond dealing with an angry insurer. Once the police are involved, both the experienced driver who fronted the policy and the young driver who benefited from it can face criminal charges.

A simple decision made to save a bit of cash can lead to a criminal record for fraud. That single mark against your name can haunt you for years, affecting job opportunities, travel visas and even getting a mortgage.

The legal penalties are designed to be a serious deterrent. They include:

- Unlimited Fines: The courts can impose unlimited fines for insurance fraud, reflecting just how seriously it is taken.

- Penalty Points & A Driving Ban: Both drivers could get up to six penalty points for driving without valid insurance. For a new driver, that is an automatic ban.

- Your Car Can Be Seized: Police have the power to seize any vehicle being driven without valid insurance, right there at the roadside.

- A Criminal Record: A conviction for fraud is a serious offence that stays with you for life.

The scary part is that many people, especially younger drivers, have no idea how severe the outcome can be. There is a massive knowledge gap where the real risks just are not understood. Research from Aviva in 2024 revealed that 35% of young drivers think lying on an insurance application is a victimless crime and a third did not know they could face an unlimited fine.

When you weigh it all up, the short-term financial gain from fronting is completely dwarfed by the risk of long-term financial ruin and legal trouble. One dishonest decision can set off a chain reaction that damages credit scores, career prospects and the freedom to drive for everyone named on that policy.

How Insurers Prove You're Lying About the Main Driver

You might think that committing fronting car insurance fraud is a quiet, harmless secret between you and your family. But in reality, insurers have a surprisingly effective, methodical process for bringing these deceptions to light. They are not just taking a wild guess; they are connecting dots using data, technology and good old-fashioned investigation.

The whole thing often unravels after a claim. An accident, no matter how small, suddenly puts your policy under a microscope. Insurers immediately start looking for red flags and inconsistencies that hint the person listed as the main driver is not actually the one behind the wheel most of the time.

The provability of the fraud is key. It usually starts with the basics. Who was driving when the incident happened? Where did it take place? If an accident occurs late at night near a university campus and the driver is a 19-year-old student but the main driver on the policy is their 50-year-old parent living 100 miles away… well, alarm bells start ringing pretty loudly.

Building a Case Against a Fraudulent Policy

Insurers do not just hang their hats on a single piece of evidence. Instead, they build a complete picture of how the vehicle is really being used. This means piecing together information from all sorts of sources to see if the story you told on the application form matches up with reality.

Their investigation is thorough and can involve several key checks:

- Address Verification: They will check where the vehicle is consistently parked overnight. Is it at the main driver's address or the named driver's? A car regularly left outside a student flat instead of the parent's home is a massive giveaway.

- Commuting Patterns: Investigators will look at where the main driver works compared to where the named driver studies or is employed. If the car's primary use is for the named driver's daily commute, the fronting arrangement quickly becomes obvious.

- Witness Interviews: After an accident, investigators often chat with neighbours, eyewitnesses or even the other driver involved. Simple questions like, "Who do you normally see driving this car?" can unravel a fraudulent policy in minutes.

The digital footprint we all leave behind provides a rich source of evidence. Social media posts showing the supposed 'occasional' driver constantly using the car for daily activities can be all the proof an insurer needs to void a policy.

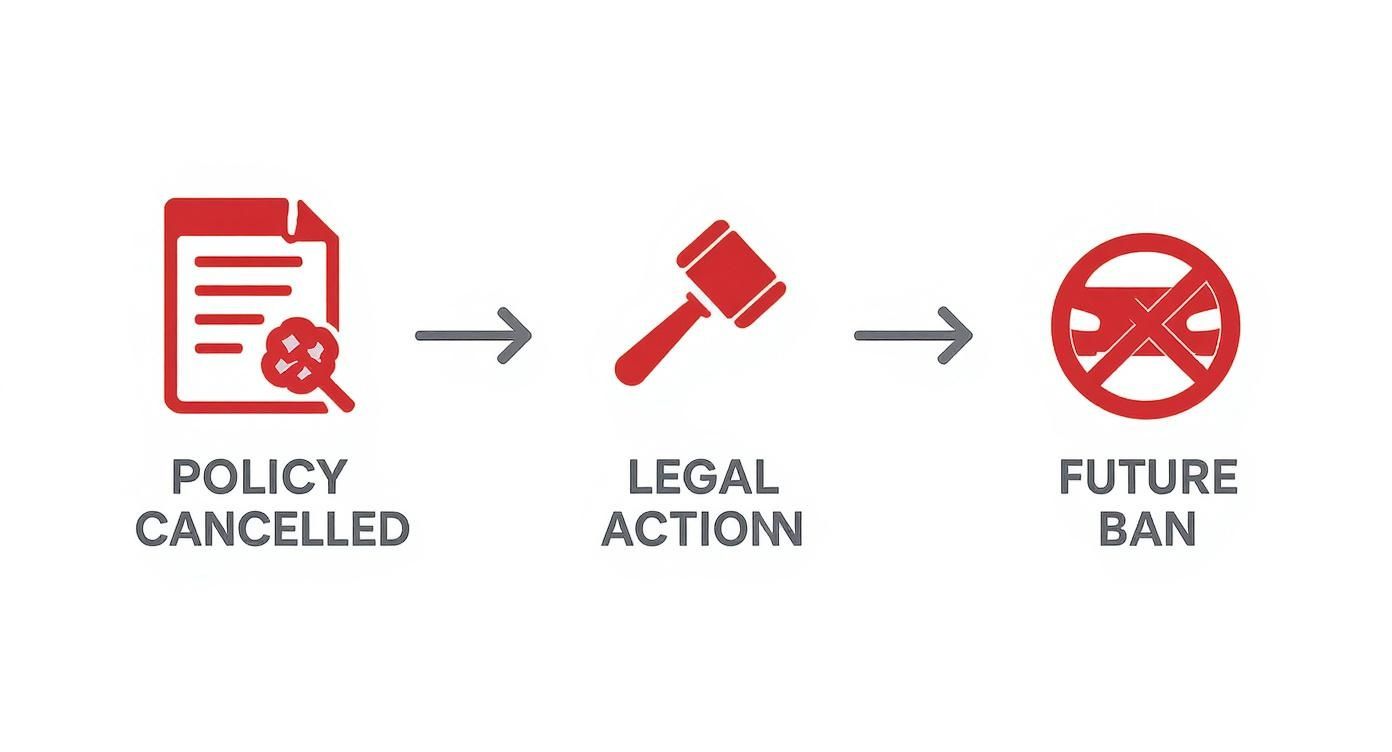

This infographic shows exactly what happens when you get caught, from the policy being cancelled right through to legal action and a potential driving ban.

As you can see, once fraud is proven, the consequences escalate fast, leading to serious and long-lasting penalties for everyone involved.

The Role of Technology in Catching Dishonesty

Modern insurance is not just about paperwork anymore. Insurers now use advanced data analytics and verification tools to spot potential fronting schemes right from the application stage—long before a claim is ever made. To tackle more sophisticated attempts at deception, insurers are turning to advanced techniques, with some even exploring machine learning fraud detection methods to identify patterns of risky behaviour.

Sophisticated algorithms can flag applications that fit a high-risk fronting profile. For example, a policy for a high-performance car with a low-risk, middle-aged main driver but a high-risk young named driver will almost certainly trigger an immediate review. This proactive approach helps stop fraud in its tracks. For a deeper look at how this fits into the wider picture, you can learn more about spotting scams and proving false claims in car insurance.

Ultimately, the belief that fronting car insurance is an easy secret to keep is a dangerous myth. With a combination of traditional investigation and powerful data analysis, insurers have become extremely skilled at proving who is truly the main driver. The risk of getting caught has never been higher and the consequences are severe.

How Fronting Fraud Hits Every Honest Driver's Pocket

It is tempting to think of fronting car insurance as a quiet, personal gamble—a little white lie that only affects the people involved. But that is a dangerously narrow view. This is not some clever loophole; it is a type of insurance fraud with a costly ripple effect and every single honest driver in the UK ends up footing the bill.

When an insurer discovers a fronted policy, they do not just shrug and absorb the loss. Every fraudulent claim that gets paid and every dodgy policy that has to be cancelled digs a deeper financial hole for the industry. To stay in business, insurance companies have to balance their books somehow.

And that means spreading those losses across their entire customer base. The direct result? Premiums go up for everyone. The dishonest shortcut taken by a few makes driving more expensive for millions of law-abiding motorists.

The Staggering Scale of Motor Insurance Fraud

The collective cost of insurance fraud is not just a rounding error; it is a multi-billion-pound problem. While fronting is just one piece of the puzzle, it contributes to a wider culture of deception that ultimately inflates costs for everyone. When insurers are forced to spend more on investigations and cover losses from dishonest claims, those expenses get baked into the price of every policy sold.

The numbers are genuinely shocking. In 2022, the Association of British Insurers (ABI) uncovered 72,600 dishonest motor insurance claims worth a massive £1.1 billion . These figures lay bare the immense financial damage caused by fraudulent activities like fronting. As insurers pay out on invalid claims or deal with the fallout, they claw back these losses by hiking premiums across the board. To see more data on this topic, you can explore detailed insights on insurance fronting.

Fronting is not a clever saving trick. It is an act that poisons the well for everyone. Each fraudulent policy contributes to a system where trust is eroded and costs are driven up, forcing honest drivers to subsidise the dishonesty of others.

This creates a vicious cycle. Higher premiums squeeze drivers financially, which might tempt more people to consider dishonest shortcuts like fronting—fuelling the very problem that caused the price hikes in the first place.

Connecting the Dots to Your Premium

So, how does a fraudulent policy taken out hundreds of miles away actually hit your wallet? The simplest way to think about it is to see car insurance as a giant collective fund that all drivers pay into. This pot of money is then used to pay for claims when accidents happen.

When people commit fraud, they are essentially stealing from that collective pot.

- Increased Operational Costs: Insurers have to plough huge amounts of money into fraud detection teams, sophisticated software and lengthy investigations to root out dishonest applications. Those operational costs are passed straight on to you, the consumer.

- Higher Risk Pools: Widespread fraud makes it incredibly difficult for insurers to calculate risk accurately. If they cannot trust the information they are given, they have to assume a higher level of risk right across their books, which translates to higher base premiums for all customers.

The sheer scale of this issue is immense and you can delve deeper into what insurance fraud really costs the industry to understand the full financial impact. At the end of the day, fronting is far more than a personal risk. It is a selfish act that damages the integrity of the insurance system and makes the road a more expensive place for us all.

Legitimate Ways to Reduce Your Car Insurance Premium

After exploring the serious risks of fronting car insurance , it is a relief to know there are plenty of honest and effective ways to lower your premium. The high cost of insurance, especially for new drivers, can feel like a massive hurdle but committing fraud is a game that is never worth playing.

The good news is you can take back control. By making smart, legitimate choices, you can demonstrate you are a lower-risk driver—and that is exactly what insurers reward. From the car you choose to the way you drive, every decision can make a real difference to your annual bill without ever crossing a legal line.

Choose Your Vehicle Wisely

One of the biggest levers you can pull to influence your premium is the car itself. Insurers sort every vehicle into one of 50 insurance groups ; group 1 is the cheapest to insure and group 50 is the most expensive. It is simple, really: a car in a lower group usually has a smaller engine, is cheaper to repair and has better security.

Before you even think about buying a car, check its insurance group. Picking a model in groups 1-10 can lead to massive savings, particularly if you are a young driver. This single choice can have a bigger impact than almost anything else.

Prove Your Skills and Build Trust

Insurers want proof that you are a safe and responsible driver. Passing your test is just the starting line. Going the extra mile shows you are committed to road safety and it can unlock some serious discounts.

-

Take an Advanced Driving Course: Completing a recognised course like Pass Plus proves to insurers you have skills that go beyond the basic test, like motorway and night-time driving. Many providers will offer a discount to drivers with this qualification.

-

Consider Telematics (Black Box) Insurance: This is one of the most direct ways for young drivers to slash their costs. A small device tracks your driving habits—things like speed, braking and mileage—and rewards safe behaviour with lower premiums at renewal. It is your chance to prove you are a low-risk individual, not just another statistic.

-

Build Your No-Claims Bonus: This one is a long-term strategy but it is incredibly powerful. For every year you drive without making a claim, you earn a discount. To get the full picture, check out our guide on how a no claims bonus works for UK drivers.

Fine-Tune Your Policy Details

Tweaking the details of your policy is another brilliant way to bring the cost down. By adjusting a few key elements, you signal to insurers that you are actively managing your risk, which often results in a better quote.

Increasing your voluntary excess—the amount you agree to pay towards a claim—shows you are less likely to make small, frivolous claims. This confidence can be rewarded by the insurer with a noticeably lower overall premium.

Other smart adjustments include:

-

Adding a Lower-Risk Named Driver: Legally adding an experienced driver, like a parent, who will use the car occasionally can sometimes lower the premium. This is the correct way to add another driver, as long as you remain the main user.

-

Paying Annually: If you can swing it, paying for your entire year's premium upfront is nearly always cheaper than monthly instalments because it cuts out the interest charges.

Instead of resorting to risky shortcuts like fronting, these strategies offer a clear, legal path to lower car insurance costs. We have put together a quick summary of the most effective options below.

Effective and Legal Methods to Lower Car Insurance Costs

| Strategy | How It Works | Potential Premium Reduction |

|---|---|---|

| Choose a Low-Group Car | Opt for a vehicle in insurance groups 1-10, which are cheaper to insure. | High |

| Install a Telematics Box | A device tracks safe driving habits (braking, speed, mileage) to earn discounts. | High |

| Increase Voluntary Excess | Agreeing to pay more towards a claim reduces the insurer's risk and your premium. | Medium |

| Pay Annually | Paying the full premium upfront avoids interest charges on monthly payments. | Low to Medium |

| Add a Named Driver | Adding an experienced, low-risk driver who uses the car occasionally can help. | Low to Medium |

| Build a No-Claims Bonus | Earn a discount for every year you go without making a claim. | Grows over time (High) |

| Take an Advanced Course | Completing a course like Pass Plus proves you have extra driving skills. | Low |

By using these honest methods, you can actively reduce your car insurance costs while building a solid and trustworthy insurance history for the future. It is about playing the long game and proving you are a safe bet on the road.

Got Questions About Fronting?

Let us clear up some of the common grey areas around car insurance fronting. These are the kinds of real-world questions that often trip people up.

Is It Still Fronting If the Main Driver Uses the Car Sometimes?

Yes, it absolutely can be. What really matters is who drives the car most of the time.

Think about it this way: if the higher-risk driver (say, your son or daughter) is the one using the car for their daily commute, running errands or heading out with friends, then they are the true main driver. Naming someone else is just misrepresentation, even if that person takes the car out for a spin now and then. Insurers base their premiums on the person who is on the road the most, as that is where the real risk lies.

What Happens If I'm a Passenger in a 'Fronted' Car?

This is a really tricky spot to be in. If you are injured as a passenger, you might be able to claim compensation through the Motor Insurers' Bureau (MIB). This is a fund designed to help victims of uninsured and untraced drivers.

Because fronting car insurance makes the policy void, the driver is effectively uninsured. While the MIB provides a crucial safety net, making a claim is often far more complicated and takes much longer than a standard insurance claim. Plus, it does not let the drivers off the hook—they will still face serious legal and financial trouble.

Can I Legally Add My Child to My Policy?

Of course. Adding your child, or anyone else, as a 'named driver' is perfectly legal and very common, as long as you remain the main driver. This is the standard way to insure a genuinely shared family car.

The key difference here is honesty. If you are the one using the car for your 9-to-5 and most other trips and your child only borrows it on weekends, then listing them as a named driver is the right thing to do. It is all about being truthful about who is really in the driver’s seat.

When you can prove ownership and usage right from the start, there is no room for doubt. It protects everyone involved. With Proova , you can document exactly who uses a vehicle and what is insured, making sure any future claims are settled on facts, not guesswork. Find out how Proova builds trust and transparency at https://www.proova.com.