Fraud Car Insurance: Spotting Scams and Proving False Claims

Car insurance fraud is not just a technical term; it is any deliberate deception aimed at securing an unfair payout from an insurer. This can range from highly organised criminal rings staging accidents to an individual simply exaggerating a genuine claim.

No matter the scale, the result is the same: it drives up costs for every honest policyholder in the UK. The key for insurers is not just spotting fraud but having the undeniable evidence to prove it, allowing for swift and fair outcomes for all.

The Hidden Tax Inflating Your Car Insurance Premiums

Many people mistakenly see car insurance fraud as a victimless crime—a small fib told to a massive, faceless corporation. But that view is dangerously wrong. In reality, every fraudulent claim acts as a hidden tax, passed directly onto honest drivers through higher annual premiums.

Think of it like shoplifting. When someone steals from a supermarket, the store does not just absorb the loss. The cost is spread across all its products, forcing every paying customer to cover the shortfall with slightly higher prices. Fraudulent insurance claims work on the exact same principle but on a much bigger scale.

The Scale of the Problem and the Cost to Us All

The financial fallout is staggering. Deception in the UK motor insurance market has climbed sharply, with industry data suggesting that for every 10 claims filed, at least one is fraudulent. This widespread issue has pushed the annual cost of fraud to well over £3 billion .

This is not just an abstract number for the industry to worry about. It translates directly into an extra £90 to £100 per year on the average driver's policy. The provability of these claims is central to tackling this cost, which is ultimately borne by all of us.

Car insurance fraud is not a clever way to beat the system. It is a calculated crime that forces honest policyholders to pay more, funding the illegal activities of both opportunistic individuals and organised criminal gangs. Every inflated claim contributes to a cycle of rising costs for everyone.

Societal and Financial Consequences

Beyond the immediate financial sting, the problem creates much wider issues. It puts a heavy strain on law enforcement and clogs up the legal system, as insurers are forced to investigate and contest suspicious claims. This in turn delays genuine payouts for honest customers who have suffered a real loss, adding unnecessary stress during an already difficult time.

The knock-on effect is a slow erosion of trust between insurers and policyholders. It fosters an environment of suspicion where legitimate claims might face tougher scrutiny, slowing down the entire system. Tackling car insurance fraud is not just about protecting an insurer's bottom line; it is about building a fairer, more affordable and more efficient system for every single driver on the road. You can learn more about how this multi-billion-pound problem affects the entire industry.

A Guide to Common Car Insurance Scams

Car insurance fraud is not a single, clear-cut crime. It is a whole spectrum of deceptive practices, ranging from sophisticated schemes run by organised criminal gangs to split-second acts of opportunism by otherwise law-abiding individuals. Getting a handle on these different scams is the first step for any insurer looking to tackle the problem head-on.

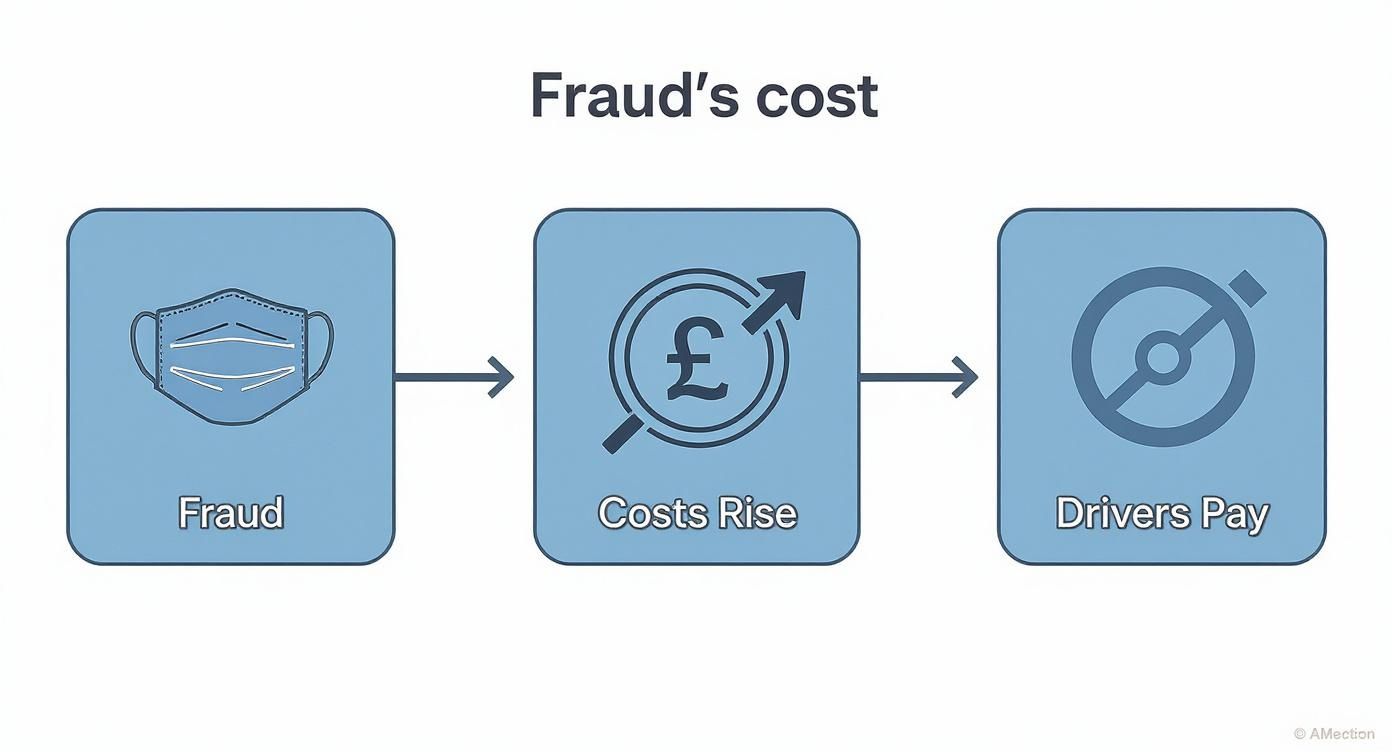

Make no mistake, these scams are a direct cause of rising premiums for everyone. The infographic below shows the damaging—and expensive—path from a fraudulent act to a higher renewal price for every single driver on the road.

As you can see, fraudulent activity systematically inflates the entire cost base for insurers. It is a financial burden that sooner or later gets passed on to honest policyholders.

To help you get a clearer picture of what you are up against, here is a quick summary of the most common schemes.

Common Car Insurance Fraud Schemes at a Glance

This table breaks down the main types of fraud, what they look like in practice and who is typically behind them.

| Fraud Scheme Type | Description | Primary Perpetrators |

|---|---|---|

| Crash for Cash | Deliberately causing an accident with an innocent driver to make fraudulent insurance claims for vehicle damage and personal injury. | Organised criminal gangs |

| Opportunistic Fraud | Exaggerating the extent of genuine damage or injury or adding pre-existing damage to a legitimate claim. | Individual policyholders |

| Application Fraud | Providing false information (e.g., address, main driver, no-claims history) to secure a lower insurance premium. | Individual applicants |

| Vehicle Cloning | Stealing a legitimate vehicle's identity (VIN, number plate) and applying it to a stolen car, often for criminal use or resale. | Organised criminal gangs |

| Ghost Broking | Fraudsters posing as brokers sell fake or invalid insurance policies to unsuspecting victims, leaving them uninsured. | Fraudulent individuals or groups |

While this table gives a high-level view, understanding the nuances of each scheme is crucial for effective detection and prevention. Let’s take a closer look at what each one entails.

Organised Crash for Cash Schemes

At the most dangerous end of the scale, you will find ‘Crash for Cash’ schemes. These are not accidents at all; they are premeditated collisions staged by criminal gangs purely to milk the insurance system for payouts. Their methods are reckless and put innocent people in very real danger.

Some of the go-to tactics include:

- The Slam-On: A fraudster’s car, often with passengers ready to claim for whiplash, will brake suddenly and violently in front of an innocent driver, giving them no chance to avoid a rear-end collision.

- The Flash for Cash: The scammer flashes their headlights to let another driver pull out of a junction then deliberately accelerates into them, later claiming the other driver was at fault.

- Ghost Accidents: Some gangs do not even need a real collision. They invent accidents that never happened, using fake identities and previously damaged vehicles to submit entirely fabricated claims.

These schemes are anything but victimless. Beyond the obvious financial cost, they inflict real physical and psychological trauma on the innocent motorists they target. The Insurance Fraud Bureau (IFB) estimates these scams cost the industry a staggering £392 million every year.

This is a persistent threat that is constantly evolving. To get a better sense of how these criminals operate, you can learn more about the methods and impact of Crash for Cash schemes in our detailed guide.

Opportunistic and Exaggerated Claims

While less dramatic than organised crime, opportunistic fraud is far more widespread. On its own, a single embellished claim might seem minor but collectively these add up to a massive cost for the industry.

This happens when a policyholder with a genuine claim decides to pad it out for a bigger payout. For example, a driver in a minor car park bump might try to claim for pre-existing scratches and dents, pretending they happened in the incident. Another classic is exaggerating injuries, like claiming for severe whiplash after a low-speed collision where such an injury is medically improbable. This kind of dishonesty turns a legitimate claim into a fraudulent one.

Application and Policy Fraud

Fraudulent activity can start long before an accident ever occurs. Application fraud, often called misrepresentation , is when someone knowingly lies to an insurer to get a cheaper premium. It is a calculated deception from day one.

This takes several common forms:

- Fronting: A classic example is a parent insuring a car in their name but listing their high-risk teenage son or daughter as a named driver, when really the teenager is the one using it every day.

- Address Deception: Someone might provide a false address in a sleepy, low-risk village to dodge the higher premiums of the city postcode where they actually live.

- NCD Fraud: Falsely claiming to have more years of No Claims Discount than they have actually earned is another popular way to slash the cost of a policy.

Sophisticated Vehicle Scams

Some of the more complex fraud car insurance scams target the identity of the vehicle itself. Vehicle cloning is a nasty one, where criminals steal the identity of a legally registered car—its number plate, VIN, the lot—and apply it to a similar, usually stolen, vehicle. This 'cloned' car is then used to commit crimes or is sold on to an innocent buyer who loses everything.

Another growing menace is ghost broking . Here, fraudsters set themselves up as legitimate insurance brokers, often targeting vulnerable people on social media with impossibly cheap policies. The victims pay up and think they are covered, only to find out their policy is completely fake when they need to make a claim. They are left uninsured, out of pocket and in serious legal trouble.

Inside the World of Organised Motor Fraud

Opportunistic fraud is one thing but organised motor fraud is another beast entirely. We are not talking about a single person exaggerating a claim; this is about criminal gangs running sophisticated, large-scale operations designed to systematically exploit the insurance industry. These are not minor offences. They are serious, calculated crimes that put innocent people in danger and carry severe legal consequences.

Modern fraud rings operate with a level of coordination once reserved for major criminal enterprises. They use complex methods, from identity theft to create fake claimants to intricate, multi-vehicle 'crash for cash' scenarios. These gangs are often involved in other serious crimes and the profits from fraud car insurance are used to fund their wider illegal activities. The scale of their operations demands a robust and coordinated response from both insurers and law enforcement.

The Anatomy of a Ghost Broking Scam

One of the most damaging forms of organised fraud is ‘ghost broking’ . This scam sees criminals pose as legitimate insurance brokers, often targeting vulnerable or younger drivers on social media with offers of unbelievably cheap cover. The victims, desperate for an affordable policy, are lured into a trap.

The process is deceptively simple but devastating for the victim:

- The Lure: The ghost broker advertises heavily discounted car insurance on platforms like Instagram or Facebook.

- The Deception: They take the victim’s money and either provide completely fake, forged policy documents or they purchase a genuine policy using stolen personal details and false information to lower the price, then cancel it shortly after to claim a refund.

- The Fallout: The victim drives away believing they are insured, only to discover the truth after being stopped by the police or trying to make a claim. They are left uninsured, out of pocket and facing potential prosecution.

Crash for Cash Hotspots and Tactics

Organised 'crash for cash' gangs are a major public safety concern. These criminals deliberately cause collisions with innocent motorists to stage elaborate claims for vehicle damage, personal injury and even hire car costs. Far from being random, these incidents are often concentrated in specific geographical areas known as fraud hotspots.

The Insurance Fraud Bureau (IFB) has identified numerous postcodes across the UK, particularly in cities like Birmingham, Bradford and London, where these gangs are most active. This geographical concentration allows them to build networks of complicit garages, claims management companies and even medical professionals to support their fraudulent claims.

The tactics they employ are reckless and designed to make the innocent party appear at fault. They might slam on their brakes for no reason, disable their brake lights to catch drivers unaware or use a second vehicle to create a distraction before the collision. The goal is always the same: to orchestrate a crash that seems like a clear-cut case of liability for the unsuspecting victim, paving the way for a fraudulent payout.

The True Cost and Consequences

The financial impact of these operations is immense. Leading UK insurer Aviva revealed it had stopped over 6,000 fraudulent claims in just the first half of a recent year, preventing losses of more than £60 million . That amounts to over £334,000 every single day . You can read more about how Aviva is tackling the rising tide of fraud.

The human cost is equally severe, with innocent drivers left traumatised by staged accidents. However, the legal system is responding with increasing severity. The notion of this being a low-risk crime is outdated. Convictions for insurance fraud are on the rise and the courts are handing down substantial prison sentences. In one year alone, prison sentences from fraudulent claims detected by a single insurer surpassed a cumulative total of 32 years . The message is clear: organised motor fraud is a serious crime with life-altering consequences for the perpetrators.

How Insurers Prove a Claim Is Fraudulent

When an insurer suspects a claim might be fraudulent, they do not just rely on a gut feeling. They kickstart a meticulous, evidence-based investigation process designed to separate genuine claims from bogus ones. This is not about creating hurdles for honest policyholders; it is about building a robust defence against those trying to exploit the system.

The whole operation is a smart blend of human experience and powerful technology. It all starts the moment a claim is filed, as automated systems scan for inconsistencies a human might initially miss. From there, seasoned claims adjusters and specialist fraud investigation units take the reins, digging deep to verify every detail and build a solid, provable case.

Ultimately, this process protects everyone. It ensures that payouts are reserved for legitimate losses and helps keep premiums as fair as possible for millions of honest drivers.

The First Line of Defence: Red Flags

Claims handlers are trained to spot the tell-tale signs that a claim needs a closer look. While a single red flag might just be an honest mistake, a cluster of them often points to something more deliberate. Investigators are always on the lookout for these patterns.

Common red flags include:

- Vague or Inconsistent Details: The claimant struggles to give a clear account of what happened or their story seems to change every time they tell it.

- Immediate Legal Representation: A solicitor gets involved almost instantly after a seemingly minor incident, sometimes before the insurer has even been notified.

- Delayed Reporting: The accident is not reported for days or weeks without a good reason, giving fraudsters time to invent details or even cause more damage.

- Unusual Claim History: The claimant has a track record of making frequent or suspiciously similar claims, suggesting a pattern of behaviour.

These early indicators are enough to move a claim from the standard processing queue into an active investigation.

At its core, proving fraud is about piecing together an undeniable narrative of deception. Investigators have to meticulously connect the dots, turning suspicion into solid evidence that can stand up in court. The goal is to dismantle the fraudster's story, one piece at a time.

Advanced Detection and Data Analytics

Beyond the initial red flags, insurers use sophisticated techniques to unearth fraud. This is where technology really comes into its own, cross-referencing information against vast industry databases to spot connections and anomalies that would otherwise be invisible.

One of the most powerful resources is the Claims and Underwriting Exchange Register (CUE) , a database holding records of all incidents reported to UK insurers. Investigators check this to see if a claimant has conveniently forgotten to mention previous accidents or claims. They also use the Insurance Fraud Register (IFR) to identify individuals with a known history of fraudulent activity.

Building an Undeniable Case

Proving fraud requires more than just suspicion—it demands cold, hard evidence. Specialist investigation units build their case by methodically gathering and verifying information from multiple, independent sources.

This rigorous process often involves a few key steps:

- Forensic Vehicle Examination: Engineers inspect the vehicles to see if the damage matches the story. They can easily spot pre-existing damage or tell-tale signs that a collision happened at a much lower speed than claimed.

- Social Media and Background Checks: Investigators may review public social media profiles. It is not uncommon to find a claimant pleading a debilitating injury posting photos of themselves playing football or hiking, which directly contradicts their claim.

- Witness Interviews and Site Visits: Investigators will talk to witnesses, police and paramedics. They might also visit the accident scene to confirm whether the events described are even physically plausible.

- Data Link Analysis: Using specialised software, investigators can map out connections between claimants, witnesses, garages and solicitors. This often uncovers the hidden networks that are the hallmark of an organised 'crash for cash' gang.

This painstaking work ensures genuine claims are handled smoothly while fraudulent ones are stopped in their tracks. It is a critical process that protects the integrity of the insurance system for everyone.

Using Technology to Stop Fraud at the Source

For years, tackling car insurance fraud has felt like a game of cat and mouse. Investigators are always one step behind, reacting to red flags only after a claim has been lodged. They are left piecing together evidence to challenge a story that might have been built on lies from the very beginning. This reactive approach is slow, expensive and leaves insurers permanently on the back foot.

But technology is flipping the script. Instead of just catching fraud after the damage is done, insurers can now stop it at the source. The focus is shifting from chasing down suspicious claims to verifying genuine evidence the moment it is created.

Preventing After the Event Fraud

One of the biggest headaches for claims handlers is ‘after the event’ fraud . This is where someone manipulates evidence after an incident has already happened. Think old photos being passed off as new damage or, worse, digitally altered images designed to exaggerate the severity of a real collision.

Without solid proof of when and where a photo was taken, disputing these claims becomes an uphill battle. This is precisely where technology that verifies evidence in real-time makes all the difference. For a deeper look into how AI is tackling these challenges, this AI fraud detection guide offers a comprehensive overview.

The Power of Real-Time Media Verification

Solutions now exist that can confirm the authenticity of photos and videos right at the point of submission. You can think of it as a digital fingerprint for evidence. When a policyholder uses a specific app to capture vehicle damage at the scene, the technology immediately locks in critical metadata.

This simple action creates a provable, time-stamped record that confirms three crucial things:

- When the photo or video was taken.

- Where it was captured, using precise location data.

- That it has not been tampered with from the moment of capture.

Suddenly, it becomes almost impossible for fraudsters to use old or doctored images to back up a dishonest claim. It establishes a clear chain of custody for digital evidence, guaranteeing its integrity from the get-go.

By validating evidence at the first point of contact, insurers can shut the door on opportunistic fraud before it even enters the claims workflow. This not only saves money but also frees up investigators to focus on more complex, organised criminal activity.

Accelerating Genuine Claims with Verifiable Proof

This technological leap is not just about stopping fraudsters. For the vast majority of honest policyholders, it means a much faster and smoother claims experience. When the evidence they submit is instantly verifiable, adjusters can approve claims with confidence and speed. You can learn more about fighting fraud before it happens with the power of verified evidence.

Instead of frustrating delays caused by suspicion and lengthy investigations, genuine customers get their payouts quicker. This is a massive boost for customer satisfaction and builds trust by showing that the insurer is on their side. By integrating these tools, the industry can create a system that is both tougher on fraudsters and fairer to everyone else.

Building a Modern Anti-Fraud Workflow

Shifting from a reactive "catch-them-if-you-can" approach to a proactive prevention strategy takes more than just clever tech. It demands a complete rethink of your claims workflow. A truly modern process embeds vigilance into every single step, from the moment a claim is first reported right through to the final settlement. This is how you build a systematic defence against fraud car insurance schemes.

A successful workflow is not just a manual with a set of rules; it is a cultural change. It is about giving claims handlers the tools and the confidence to spot things that do not add up, backed by a clear process for when they need to escalate a concern. The aim is to create a smooth system that fast-tracks genuine claims while intelligently flagging suspicious ones for a closer look, all without creating headaches for your honest customers.

From First Notice to Final Resolution

An effective workflow dissects the claims journey into clear stages, each with its own checks and balances. This step-by-step framework is your key to consistency and thoroughness.

Think of the anti-fraud claims journey in these key phases:

- Initial Claim Notification: The moment a claim is logged, automated systems should be scanning the details. Is there a link to a known fraudster? Are there glaring inconsistencies in the story from the get-go? These initial checks are your first line of defence.

- Evidence Submission and Verification: This is a make-or-break stage. When policyholders send over photos or documents, technology needs to verify their authenticity. Confirming exactly when and where that "evidence" was captured is crucial for shutting down any 'after the event' manipulation.

- Triage and Assessment: Based on the initial data and, most importantly, the verified evidence, claims are sorted. Low-risk, straightforward claims can be fast-tracked for payment. Anything with red flags gets routed to your specialist investigators.

- Investigation and Intelligence Gathering: For flagged claims, the deep dive begins. Investigators will use everything at their disposal—data analytics, industry databases and forensic analysis—to piece together the full picture.

- Resolution: Finally, the claim is either paid, negotiated or denied based on the evidence. Crucially, all findings are logged to make your fraud detection models even smarter for next time.

It is worth looking at how other industries tackle similar problems. For instance, effective retail loss prevention strategies show the power of embedding preventative measures at every single touchpoint.

Establishing Clear Performance Indicators

To know if your new workflow is actually working, you have to track the right metrics. Key Performance Indicators (KPIs) give you a clear, honest view of how well your anti-fraud strategy is performing and shine a light on areas that need improvement.

A data-driven approach is non-negotiable. Without clear KPIs, you are just guessing. You will not know if your workflow is genuinely cutting fraud or just adding friction to the claims process. Tracking the right metrics turns that guesswork into a measurable strategy.

Here is a look at some of the essential KPIs that every fraud detection team should be monitoring. These benchmarks provide a solid starting point for measuring success and identifying areas for improvement.

Key Performance Indicators for Fraud Detection Teams

A breakdown of essential metrics insurers can use to measure the effectiveness of their anti-fraud strategies.

| KPI Metric | Description | Industry Benchmark |

|---|---|---|

| Fraud Detection Rate | The percentage of all claims that are correctly identified as fraudulent. | 3-5% of all referred claims |

| False Positive Rate | The percentage of genuine claims that are incorrectly flagged as suspicious. | Below 15% of flagged claims |

| Average Investigation Time | The average time it takes from when a claim is flagged to when it is resolved. | 30-45 days |

| Referral-to-Detection Ratio | The percentage of claims referred for investigation that are ultimately confirmed as fraud. | 10-20% depending on referral quality |

| Savings per Investigator | The total value of fraudulent claims denied or reduced, divided by the number of investigators. | Varies by company size and fraud type |

By regularly reviewing these metrics, you can fine-tune your processes, allocate resources more effectively and demonstrate the real-world value your anti-fraud efforts are delivering.

The final piece of the puzzle is fostering a culture of vigilance. This means ongoing training for all claims staff, not just the specialists. When everyone in the organisation understands the common tactics fraudsters use and knows their role in stopping them, your entire workflow becomes stronger and far more resilient. This collective effort is the foundation of any truly modern defence against insurance fraud.

Got Questions About Car Insurance Fraud?

Diving into the world of car insurance fraud can feel a bit complex. To make things clearer, we have put together straightforward answers to the questions we hear most often from policyholders and industry pros alike.

What Should I Do If I Suspect Fraud?

If you see something that does not look right, like a staged accident, or think someone might be committing insurance fraud, the best thing you can do is report it. The Insurance Fraud Bureau (IFB) has a confidential Cheatline set up for exactly this purpose.

Even small details can be crucial. Jot down the location, vehicle registrations and anything you observed – it all helps investigators piece together a case. You should also let your own insurer and the police know, especially if you were caught up in a suspicious incident. Your report is more than just a single piece of information; it adds to a bigger picture that helps keep everyone's premiums down.

How Does Fraud Actually Affect My Premiums?

It is easy to think of fraud as a victimless crime that only affects big insurance companies but that is not how it works. Every single fraudulent claim paid out goes into a pot of losses that insurers have to cover. To stay in business, they have no choice but to spread those costs across all their customers.

So, even if you have never made a claim and have a spotless driving record, a slice of your annual premium is going towards paying for someone else's dishonesty. And the problem is getting bigger. In the first half of a recent year, insurance-related fraud filings shot up by a staggering 272% compared to two years earlier, often driven by fake documents. You can dig into the numbers in these UK fraud prevention findings.

It is a common myth that fraud only hurts the insurer. The reality is, it acts like a hidden tax on every honest driver, pushing up the cost of cover for everyone on the road.

Is a Tiny Exaggeration Really Considered Fraud?

Absolutely. It might seem harmless to add a bit of old, pre-existing damage to a new claim or to slightly overstate an injury but it is still fraud. This is what the industry calls 'opportunistic fraud' and it is a criminal offence.

Getting caught can have serious consequences. Your insurer will likely cancel your policy, which makes getting cover from anyone else in the future incredibly difficult and expensive. That small exaggeration just is not worth the risk.

Take the guesswork out of claims and stop fraud before it starts. Proova provides real-time media verification, ensuring the evidence you receive is authentic and trustworthy from the moment it is captured. Discover how Proova can protect your business and accelerate genuine claims.