Do Dashcams Lower Insurance Premiums in the UK?

So, you’re wondering if fitting a dashcam to your car will actually lower your insurance premium. The short answer is yes but perhaps not in the way you might expect.

While some insurers do offer a direct discount just for having one, the real financial win comes from something far more valuable: having indisputable proof when an accident happens. This is what truly protects your wallet, your no-claims bonus and your good name.

Why Proof Is Your Best Financial Defence

Most UK drivers asking "do dashcams lower insurance?" are hoping for an upfront price cut. That’s understandable but it misses the bigger picture. A dashcam’s true power lies in its ability to act as your silent, impartial witness, proving exactly what happened on the road.

Think about it. How many insurance claims spiral into a messy 'he said, she said' argument? Without clear evidence, insurers are often forced to settle on a 50/50 basis where both drivers are deemed equally at fault. That kind of outcome can sting, pushing up your renewal premiums for years to come.

The Real Cost of Doubt

Insurance fraud is a massive problem in the UK and it inflates costs for every single honest driver. Organised 'crash for cash' schemes are specifically designed to create confusion and make it impossible to prove who was really at fault.

These scams add a huge financial burden to the insurance industry and that cost is ultimately passed on to all of us through higher premiums.

A dashcam is your single best defence against these fraudsters. By capturing the entire event as it unfolds, the footage strips away all doubt and exposes the scam. Not only does this save you from an unfair claim but it also helps the entire industry fight a problem that costs everyone money.

Direct vs. Indirect Savings

It’s crucial to separate the two ways a dashcam saves you cash. The first is a direct discount but this isn't a given with every provider. While installing a dashcam doesn't guarantee an instant drop in your premium, some UK insurers are offering discounts from 10% to 30% with average savings hovering around £113 per policy. You can find more dashcam insurance facts on topcarcheck.co.uk.

The second, and far more significant, saving is indirect. This is all about protecting your hard-earned no-claims bonus and sidestepping the massive premium hikes that follow an at-fault or shared-fault claim. Over the long term, this financial protection is often worth far more than any initial discount.

Let's break down how these savings stack up.

How a Dashcam Can Reduce Your Motoring Costs

This table shows the direct and indirect ways a dashcam can reduce your motoring costs, from upfront premium discounts to long-term no-claims bonus protection.

| Type of Saving | Potential Reduction | How It Works |

|---|---|---|

| Direct Insurance Discount | 10% - 30% (with participating insurers) | Some insurers offer an immediate premium reduction for installing an approved dashcam. |

| No-Claims Bonus (NCB) Protection | Up to 70% (or more, depending on your NCB level) | Footage proves you weren't at fault, protecting the discount you've built up over years. |

| Avoiding Excess Payments | £250 - £1,000+ | Proving non-fault means you don't have to pay your policy excess for the claim. |

| Fighting Fraudulent Claims | Prevents a faulty claim against your policy | Video evidence exposes 'crash for cash' scams, stopping fraudsters in their tracks. |

| Avoiding Future Premium Hikes | Hundreds of pounds over several years | A non-fault claim doesn't lead to the steep premium increases that follow an at-fault incident. |

As you can see, while the initial discount is a nice bonus, the real value lies in preventing the much larger financial hits that come from an unresolved or fraudulent claim. That's where a dashcam truly pays for itself.

How a Dashcam Becomes Your Financial Shield

While a small upfront discount on your premium is a nice perk, it’s not the real reason a dashcam is one of the smartest investments you can make for your car. The single greatest financial benefit is its power to protect your hard-earned no-claims bonus (NCB).

For most drivers, a healthy NCB is the biggest factor keeping their insurance affordable. It's a reward for years of careful driving. But all that can vanish in an instant.

Without clear evidence, a straightforward, non-fault accident can descend into a messy "he said, she said" stalemate. When insurers face two conflicting stories and no independent witnesses, they often have little choice but to settle the claim on a 50/50 basis. For you, that outcome is financially brutal, often wiping out years of your NCB and sending your premiums soaring.

The Power of Provability

This is where your dashcam steps in and truly acts as your financial shield. The footage it captures provides cold, hard proof of exactly what happened, turning a tangled dispute into a simple matter of fact.

By showing you weren't at fault, the video evidence safeguards your NCB from being unfairly slashed or wiped out entirely. This single act of provability can save you hundreds, if not thousands, of pounds over the next few years.

Recent data shows just how vital this is. Dashcams are proving invaluable in closing the UK's 'accident evidence gap' where a staggering 70% of drivers without solid proof end up shouldering unfair blame and facing punishing premium hikes. A disputed 50/50 claim could easily turn a £500 premium into £800 in the first year alone. You can dig deeper into how drivers face unfair blame on wecovr.com.

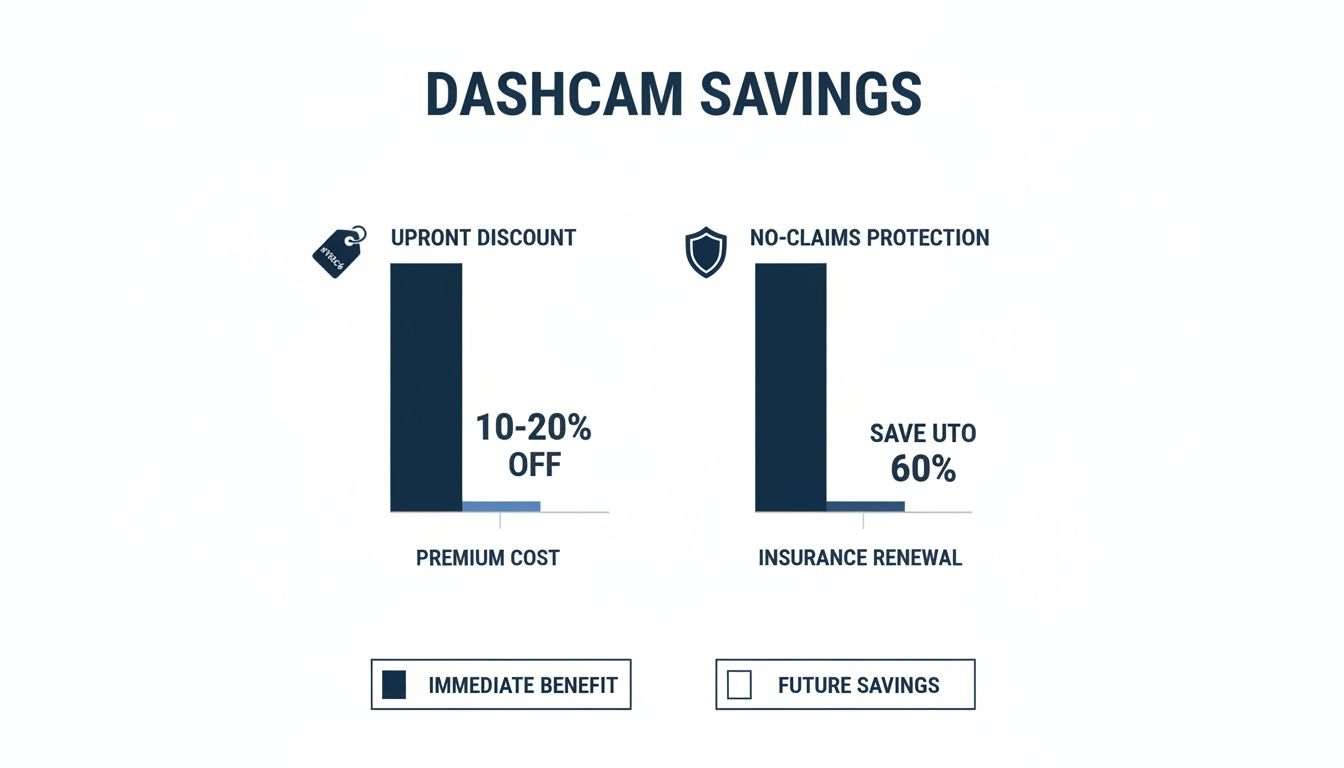

This infographic breaks down the two main ways a dashcam saves you money, comparing the immediate discount with the far more significant long-term protection it offers.

As you can see, while the initial discount is welcome, it pales in comparison to the savings from protecting your no-claims bonus down the line.

Let's look at how this plays out over time. A 50/50 claim doesn't just hurt for one year; its impact compounds as you lose your NCB discount.

The Financial Impact of a 50/50 Claim Without Evidence

| Year | Premium with Protected NCB | Premium After 50/50 Claim | Annual Difference |

|---|---|---|---|

| Year 1 | £500 | £800 | +£300 |

| Year 2 | £500 | £750 | +£250 |

| Year 3 | £500 | £700 | +£200 |

| Year 4 | £500 | £600 | +£100 |

| Year 5 | £500 | £550 | +£50 |

| Total | £2,500 | £3,400 | +£900 |

The table makes it clear: a single disputed incident without proof could cost you an extra £900 over five years. That's a heavy price to pay for someone else's mistake.

A Real-World Scenario

Picture this: you're driving along, minding your own business, when another car suddenly pulls out from a side road, leaving you no time to react. It's a classic, clear-cut case of the other driver being at fault.

But without a dashcam, they might lie. They could claim you were speeding or that they had the right of way. Now it's your word against theirs.

With dashcam footage, the entire dynamic changes. You simply send the video file to your insurer which shows:

- You were travelling at a safe and legal speed.

- The other vehicle clearly failed to yield.

- The point and nature of the impact are exactly as you described.

This crystal-clear evidence makes it almost impossible for the other party (or their insurer) to argue. Your insurer can confidently pursue the claim against their policy, leaving your NCB untouched and your premiums safe. Suddenly, the one-time cost of that dashcam looks like a brilliant investment.

Fighting the 'Crash for Cash' Scams That Cost Us All

Insurance fraud is far from a victimless crime. When an insurer pays out on a bogus claim, that loss doesn't just disappear. It gets absorbed into the system and is eventually passed on to honest motorists through higher annual premiums. It’s a vicious cycle where everyone with a policy ends up footing the bill for a dishonest few.

One of the most brazen forms of this is the ‘crash for cash’ epidemic. This isn't just an accident; it's a premeditated crime. Fraudsters will deliberately cause a collision with an innocent driver, all to make it look like the victim was at fault. Their goal? To file bogus claims for vehicle damage, fake injuries and other trumped-up costs.

The financial fallout is staggering. According to the Insurance Fraud Bureau, ‘crash for cash’ scams cost UK motorists an eye-watering £340 million every single year . These schemes often trap innocent drivers in complicated and expensive disputes. A dashcam’s crystal-clear footage can prove your innocence in an instant, protecting your no-claims bonus and saving you a world of stress.

Common Tactics Used by Fraudsters

Criminals have a playbook of calculated moves to stage these incidents. If you know what to look for, you can spot the warning signs on the road and avoid becoming their next target.

- The Slam-On: The classic manoeuvre. A fraudster drives erratically in front of you, maybe tapping their brakes for no reason, before suddenly slamming them on. It’s designed to cause a rear-end collision where the driver behind is almost always presumed to be at fault.

- The Flash for Cash: You’re at a junction and another driver flashes their headlights, seemingly letting you pull out. But as you do, they deliberately drive into you and later deny ever giving you the signal to go.

- The Deceptive Wave: Similar to the flash, a driver might wave you out of a side road or into traffic before purposefully causing a crash.

Without solid evidence, it's your word against theirs. In the heat of the moment, details get blurry which can make a fraudster’s well-rehearsed story sound surprisingly plausible. It’s an incredibly tough spot to be in.

A dashcam is your ultimate defence against these scams. It provides an impartial, time-stamped record that exposes the fraudster's actions and proves their intent. This footage is the irrefutable evidence insurers need to reject the fraudulent claim outright.

By providing this proof, you’re not just protecting your own wallet. You are actively helping to dismantle a criminal enterprise that inflates insurance costs for every driver in the country. Your personal device becomes a tool for the greater good, contributing to a fairer system for all UK motorists. Understanding this threat is the first step and our detailed guide explores the persistent risk of ‘crash for cash’ scams in greater detail.

Which UK Insurers Offer Dashcam Discounts?

So, with all the clear benefits of having solid proof, we get to the big question: do dashcams actually lower your insurance premiums? The answer is a bit of a mixed bag – a definite maybe. It really isn't a standard practice across the UK market just yet.

Think of the insurance landscape as a patchwork. On one side, you have forward-thinking providers who have fully embraced the value of video evidence. On the other, you have insurers who are just taking a bit longer to catch up.

Finding an insurer that gives you an upfront discount for having a dashcam often means you need to do a bit of digging yourself. While most providers will agree that dashcam footage is incredibly useful when you make a claim, only a handful will actually reward you with an immediate price cut. This isn't because they don't see the value; it’s more to do with their complex internal risk calculations and how long it takes for huge organisations to update their policies.

The Pioneers of Premium Reductions

A few insurers have jumped ahead of the curve, actively rewarding drivers who install a dashcam. They don’t just see these devices as a tool for claims; they see them as a sign of a more careful and responsible driver behind the wheel.

A small number of providers, like AXA and Swiftcover , have been known to offer a tempting 15% reduction if you fit one of their approved models. Insurers who do this tend to believe that dashcams encourage safer driving habits, a view that’s been backed up by various market reports. If you want to dive deeper into these trends, you can read the full analysis from industry observers.

Other names that have historically been open to discounts or better terms include:

- Adrian Flux: As a specialist broker, they're known for being open-minded about vehicle modifications and often look favourably on dashcams.

- Nextbase: The dashcam manufacturer has even teamed up with insurers directly to offer special discounts to customers who use their cameras.

The key thing to remember is that these offers can and do change. Your best bet is always to declare your dashcam when getting a quote and ask the insurer point-blank if it makes a difference. Many drivers discover that even if there's no set percentage off, an insurer might still offer a more competitive quote simply because you have one.

Why Are Some Insurers Still Hesitant?

For every insurer that's offering a discount, there are several more that aren't. Their reluctance usually comes down to a few practical concerns. First, there's the problem of verification. How can an insurer be sure the dashcam is always on, working correctly or that you'll even hand over the footage if it shows you were the one at fault?

Secondly, building dashcam data into their existing claims processes means investing in new systems and staff training. Because of this, many insurers find it easier to treat footage as helpful extra evidence on a case-by-case basis rather than creating a whole new discount structure around it. For a closer look at the ins and outs of getting covered, have a look at our practical guide to insuring your car in the UK.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert, following the provided style guide and examples.

How Dashcams Encourage Safer Driving Habits

It’s easy to think of a dashcam as just a silent witness, something that only becomes useful after an accident. But its real power lies in prevention. Having one installed can fundamentally change the way you drive for the better, often without you even realising it.

This all comes down to a simple psychological trigger known as the 'observer effect'. When you know you’re being recorded, your behaviour naturally adjusts. It’s the same reason you instinctively check your speedometer when you spot a speed camera. With an impartial, ever-present observer in your car, you become more mindful of your own driving habits – things like leaving a proper following distance, sticking to the speed limit or signalling correctly.

This subtle shift is exactly what insurers love to see. Even if they don't offer a direct discount for the hardware itself, a driver who actively works to be safer is a much better risk. And safer drivers, quite simply, make fewer claims.

The Proof Is in the Driving

This isn't just a theory; we see it in the real-world data from UK drivers. Many who fit a dashcam report a noticeable improvement in their own driving style. It's a proactive step that shows a genuine commitment to road safety.

In fact, data from Cornmarket Insurance Services revealed that 68% of UK drivers reported improved driving behaviour after installing a dashcam. This isn't a minor change; it's a significant shift that leads to fewer incidents across the board. You can read more about how dashcams impact driver habits on topcarcheck.co.uk.

The presence of a dashcam often transforms a driver's awareness. Small, subconscious habits like rolling through a stop sign or accelerating too quickly from a traffic light tend to fade away when you know every action is being documented.

This self-correction is what really starts to lower your risk profile. Over time, these small adjustments compound, turning you into a consistently safer, more defensive driver.

A Lower Risk Profile

At the end of the day, insurance premiums are all about calculating risk. A driver who takes concrete steps to be safer on the road is fundamentally less likely to be involved in an accident. By installing a dashcam, you're sending a clear signal to insurers that you are a responsible motorist.

This proactive improvement has a powerful ripple effect:

- Reduced Minor Incidents: More careful driving means fewer small scrapes, bumps and parking mishaps.

- Better Accident Avoidance: Increased awareness helps you anticipate and steer clear of hazards caused by others.

- Lower Likelihood of Fault: When an incident is unavoidable, cautious driving makes it far less likely you'll be the one to blame.

So, do dashcams lower insurance? While the direct discounts are what grab the headlines, it's this quiet improvement in driving behaviour that offers the most compelling argument. It's a long-term benefit that pays dividends in safety and can positively influence your premiums for years to come.

Making Your Dashcam Footage Count

Simply having a dashcam clipped to your windscreen isn’t the magic bullet for settling a claim. The real power lies in the quality and clarity of the footage it captures. What turns your camera from a simple gadget into an indispensable witness is its ability to provide undeniable proof.

High-resolution video is the absolute baseline. Think about it – grainy, blurry footage that can't pick out a number plate or a distant road sign is useless. To make sure your evidence is sharp, clear and credible, you should be looking for a device that records in at least 1080p Full HD .

But a clear picture is only half the story. Context is everything. A dashcam with built-in GPS logging is a game-changer because it embeds crucial data directly into the video file. It proves your vehicle's exact location, speed and direction of travel at the moment of impact, leaving no room for doubt about what you were doing.

Key Features for Robust Evidence

To ensure your footage can stand up to scrutiny, make sure your dashcam has these vital capabilities:

- GPS Data Logging: This is your objective proof. It records your speed and location, confirming you were driving lawfully and placing your vehicle precisely at the scene.

- High-Resolution Recording: Crystal-clear video is essential for capturing details like number plates and road signs, which can be critical for identifying who was involved.

- Reliable Parking Mode: Your car is vulnerable even when you're not in it. This feature acts as a silent guardian, recording bumps, scrapes and vandalism in car parks.

Securing and Submitting Your Footage

When an incident happens, you need to act fast to protect your evidence. The first step is securing the recording itself. While most cameras automatically lock the relevant video file when they detect an impact, it’s always smart to manually save it too, just to be safe. You don’t want it accidentally getting overwritten.

When it's time to submit the evidence, always provide the raw, unedited file to your insurer or the police. This maintains the integrity of the footage and confirms it's an impartial, untampered account of what happened. It’s also worth noting how modern technology is making it easier to show how real-time evidence changes everything in claims, from road accidents to vehicle theft.

Got Questions About Dashcams and Insurance? We’ve Got Answers.

Right, so you're thinking about getting a dashcam or you already have one. It’s a smart move. But as with anything involving insurance, a few common questions always pop up. Let's clear the air and tackle them head-on.

Do I Have to Tell My Insurer I've Installed a Dashcam?

Yes, absolutely. Think of it this way: a dashcam is technically a modification to your car, just like fitting new alloy wheels or upgrading the stereo. Insurers need to know about any changes, big or small.

Not telling them could, in a worst-case scenario, give them a reason to invalidate your policy right when you need it most. Besides, you won’t get a sniff of a potential discount if you don't declare it. When it comes to insurance, honesty isn't just the best policy—it is the policy.

Can My Own Dashcam Footage Be Used Against Me?

It certainly can. The footage is seen as an impartial, electronic witness to what happened on the road. If it clearly shows you were at fault in an accident, that evidence will be used to establish liability.

This is exactly why insurers are starting to embrace them. A dashcam doesn’t take sides; it just records what happened. It encourages a greater sense of accountability which studies have shown often leads to safer driving habits. And safer drivers make the roads better for everyone.

The whole point of a dashcam is to get to the objective truth of a situation. It protects you from false claims but it also holds you accountable for your own driving. That’s fundamental to how insurance works.

Are There Any Legal or Privacy Rules I Should Know About?

In the UK, using a dashcam for your personal car is completely legal. The main rule is a simple one born from common sense: it must not block your view of the road. Make sure it's installed discreetly, usually behind the rearview mirror.

Things get a bit different if you drive for a living, like a taxi or private hire driver. In that case, you have a duty to let your passengers know they are being recorded, usually with a clear sign inside the vehicle. And if you ever decide to upload footage to the internet—say, to a "bad drivers" compilation—you must blur out faces and number plates to comply with GDPR and general privacy laws.

At Proova , we're firm believers in the power of clear, verifiable evidence. It’s the key to making insurance fairer, faster and more transparent for everyone. Our platform is designed to help you document what you own, speeding up claims and stamping out fraud. Find out how we're building a more trustworthy insurance process at https://www.proova.com.