Contents Insurance Definition: What It Covers and How to Claim

Think of contents insurance as a financial safety net for all your personal stuff – the things that turn a property into your home. It’s there to protect you from the financial hit of events like theft, fire, or flooding, so you can replace your belongings without having to foot the entire bill yourself.

What Exactly Is Contents Insurance?

It’s easy to get confused, so here’s a simple way to think about it: if you could pick up your house and shake it, everything that falls out would be your ‘contents’. Your sofa, TV, clothes, laptop, jewellery and kitchen gadgets – all of it. That’s what this insurance is designed to cover.

This is a really important distinction from buildings insurance which covers the structure of your home itself – the roof, walls, windows and permanent fixtures. Contents insurance is purely about the movable possessions inside, making it essential for both homeowners and renters.

To give you a clearer picture, here’s a quick breakdown of what’s typically covered and what isn’t.

Contents Insurance at a Glance

| Typically Covered | Typically Excluded |

|---|---|

| Furniture (sofas, beds, tables) | The building's structure (walls, roof, floors) |

| Electronics (TVs, laptops, speakers) | Permanent fixtures (fitted kitchens, built-in wardrobes) |

| Clothing and personal accessories | Wear and tear from everyday use |

| Kitchenware (pots, pans, cutlery) | Mechanical or electrical breakdown |

| Valuables like jewellery and art (up to a limit) | Deliberate damage by the policyholder |

| Bicycles and sports equipment kept inside the home | Items used for business purposes (often needs extra cover) |

| Curtains, carpets and rugs | Pets and other animals |

Remember, every policy is different so always check the small print to see exactly what your specific cover includes.

The Role of Provability in Your Policy

When you need to make a claim, the ball is firmly in your court. You, the policyholder, have to prove to your insurer that you actually owned the items for which you are claiming. This concept of provability is the absolute bedrock of every contents insurance policy. Without solid proof, your claim could be delayed, disputed or even flat-out denied.

This creates a huge headache for many people, especially after something traumatic like a burglary or a house fire. Trying to remember every single item you’ve lost is tough enough, let alone finding old receipts for things you bought years ago.

The whole point of contents insurance is to put you back in the same financial position you were in before a loss but its effectiveness comes down to one thing: your ability to prove what you owned.

Why Fraud Inflates Costs for Everyone

This focus on proof is also the insurance industry’s main line of defence against fraud. Fraudulent claims, whether it’s slightly exaggerating the value of a stolen TV or inventing a loss altogether, cost insurers a fortune. And those costs do not just vanish – they get passed on to honest customers like you through higher premiums.

When fraud goes unchecked, the entire system gets more expensive and less efficient for everybody. That is why having undeniable proof of your belongings is so critical for genuine claims and why the industry must maintain a firm stance on the provability of any loss.

For a detailed look at getting your cover level right, our guide on how much contents insurance you need offers specific advice for UK households. By backing up your claim with solid evidence, you not only get your own payout faster but also help create a fairer, more affordable insurance market for all.

Buildings vs. Contents Insurance: What’s the Difference?

It’s one of the most common trip-ups when you’re sorting out home insurance: what’s the actual difference between ‘buildings’ and ‘contents’ cover? It sounds simple but getting it wrong can leave you with some serious gaps in your protection. Nailing this distinction is the first step to getting the right policy.

The easiest way to get your head around it is with a simple thought experiment. Picture lifting your house clean off its foundations, turning it upside down and giving it a good shake.

Everything that falls out? That’s your contents . We’re talking about your sofa, TV, clothes, books and any freestanding appliances like your washing machine or fridge freezer.

Everything that stays put – the structure itself – is covered by buildings insurance . This is the bricks and mortar stuff: the walls, roof, windows, doors and anything permanently fixed in place, like a fitted kitchen or a bathroom suite.

Defining What Stays and What Goes

That ‘upside-down house’ test works for most things but some items can still feel a bit borderline. The real question to ask is: how is it fixed to the property? If you’d need a set of tools to get it out and it was designed to be permanent, it’s almost certainly part of the building.

Let's break it down with a few real-world examples:

- Flooring: Carpets are considered contents . Why? Because you can roll them up and take them with you. In contrast, laminate or solid wood flooring that’s properly fixed down is part of the building .

- Kitchens: A freestanding cooker or microwave is contents . But the fitted kitchen units, worktops and built-in hobs are permanent fixtures, so they fall under buildings insurance .

- Appliances: Your freestanding washing machine is a classic piece of contents . An integrated dishwasher, however, which is built into your kitchen cabinets, is considered part of the building’s structure.

The guiding principle here is permanence. If you wouldn’t dream of taking an item with you when you move because it’s physically integrated into the property, it’s covered by buildings insurance, not contents.

Why This Really Matters

Understanding this difference isn't just about ticking boxes; it’s crucial for every kind of resident. If you’re a homeowner, you’ll almost certainly need both buildings and contents insurance to be fully covered. In fact, most mortgage lenders will insist you have buildings insurance as a condition of your loan.

For renters, things are much more straightforward. Your landlord is responsible for insuring the building itself. Your job is simply to protect your own personal stuff, which means all you need to worry about is getting a good contents insurance policy.

Getting this right has a direct impact on whether you can make a successful claim. If you’re burgled and your laptop is stolen, you claim on your contents policy. If a storm batters your roof, that’s a job for your buildings policy. Having the wrong cover—or worse, no cover at all—could leave you seriously out of pocket.

The Rising Tide of Insurance Fraud and Its Cost to You

When we think about contents insurance, we usually picture it as a shield against burglars or a burst pipe. But for insurers, there’s another huge threat and it comes from within: insurance fraud. Many people think of it as a victimless crime, just one person getting a bit extra from a faceless corporation. The reality is far more damaging for everyone.

Insurance fraud isn't always about elaborate criminal plots. More often, it's about opportunistic dishonesty. It might be someone exaggerating the value of a stolen laptop, adding a few non-existent items to a list of things lost in a fire or claiming for damage that was already there when they took out the policy. Each one might seem small but when you add them all up, the effect on the industry and honest policyholders is staggering.

All these fraudulent claims create massive financial holes for the insurance industry. Insurers are not sitting on endless piles of cash; they work by pooling everyone's premiums to pay for genuine claims. When they are forced to pay out for fake or inflated ones, that pool of money shrinks and the shortfall has to be covered somehow.

The Hidden Cost Passed on to You

That "somehow" is pretty simple: they increase premiums for everyone. Every dishonest claim feeds a cycle where honest policyholders like you end up paying more to cover the losses from the dishonest few. In short, you are subsidising fraud every time you renew your policy.

The Association of British Insurers (ABI) has reported that undetected general insurance fraud costs the industry more than £2 billion a year. That figure is not just an abstract number; it lands directly on our bills. It’s estimated that fraud adds an average of £50 to the annual insurance bill for every single UK policyholder. Your premium is not just based on your personal risk—it's calculated with a buffer to absorb the industry-wide cost of fraud.

This erodes trust and makes the claims process tougher for everyone, even those with completely legitimate losses. To get a real sense of the scale of this problem, it's worth understanding what insurance fraud really costs the industry and its ripple effects.

The Burden of Proof in a High-Stakes Game

Because fraud is such a pervasive threat, insurers have no choice but to put the burden of proof firmly on the policyholder's shoulders. When you make a claim, it is on you to provide clear, convincing evidence that you owned the items, they were in the condition you have stated and the loss happened the way you described it. This is not just red tape; it is a fundamental part of how contents insurance works.

Try to see it from their side. Without solid proof, the floodgates would open to countless fabricated claims. But this need for verification puts honest customers in a really tough spot, especially right after a traumatic event like a break-in or a flood.

The challenge of proving ownership for dozens, or even hundreds, of items from memory, without receipts or photos, can be completely overwhelming. It is this exact friction point—the gap between a genuine loss and the ability to prove it—that can turn a simple claim into a long, stressful dispute.

Common Types of Contents Insurance Fraud

To protect yourself and understand why insurers are so cautious, it helps to know what fraud typically looks like. These are the kinds of actions that directly lead to the higher premiums we all have to pay.

- Opportunistic Exaggeration: This is the most common kind of fraud. A classic example is claiming a five-year-old TV was a brand-new, top-of-the-range model.

- Claiming for Pre-Existing Damage: Someone might buy a policy after cracking their phone screen, wait a few weeks and then file a claim for accidental damage.

- Fabricating a Loss: This involves inventing a theft or loss that never actually happened, like reporting a valuable watch stolen when it was simply lost or sold.

- Organised Schemes: On a much more serious level, criminal groups stage fake burglaries or accidents to submit high-value claims, often involving multiple people and policies.

The industry's battle against these scams is precisely why having robust, verifiable evidence is no longer a 'nice-to-have'—it is an absolute must for a smooth claims process. Thankfully, modern solutions are now emerging to close these gaps, protecting insurers from fraud and saving honest customers from the nightmare of trying to prove a genuine claim.

How to Prove Your Claim with the Right Evidence

Let’s be honest. After a fire or a burglary, the last thing you want to do is start a monumental paperwork quest. Your world has just been turned upside down and now you’re expected to prove everything you’ve lost. Insurers need solid evidence to pay out a claim fairly but when you’re still in shock, providing it can feel like an impossible burden.

The old way of doing things involves you digging through files for ancient receipts, hunting down bank statements or trying to find a photo where your stolen TV just happens to be in the background. It's a slow, painful process that puts all the pressure on you at the worst possible time.

Think about it. Could you, right now, list every single item in your living room? The TV model, the books on the shelf, the art on the walls and what each one was worth? It’s a brutal memory test and any gaps in your memory could cost you thousands. This is where the friction starts. The insurer needs to verify your loss to prevent fraud, while you just need help getting back on your feet. When the evidence is weak, the whole process grinds to a halt.

The Problem with Traditional Proof

Relying on old-fashioned methods is a recipe for frustration. It’s not just that it’s hard to remember everything you own; finding the paperwork is often impossible, especially if it was destroyed in the very event for which you are claiming.

Here’s why the traditional approach falls short:

- Receipts Fade and Get Lost: Let's be realistic. The receipt for that sofa you bought three years ago is probably long gone. Even if you do find it, chances are the ink has faded into a useless smudge.

- Photographs Lack Detail: A happy family photo might show your laptop in the background but it won’t prove the make, model or its condition. It gives context but it is not the concrete proof of value an insurer needs.

- Memory is Unreliable Under Stress: After a traumatic event, our brains are not wired for perfect recall. You’re almost guaranteed to forget things, which means you’ll end up under-claiming and losing out.

The struggle to prove genuine claims does not just affect you; it creates wider problems across the industry and every policyholder ends up paying the price.

This data is not just a bunch of abstract numbers. It shows a direct link between the difficulty of verifying genuine claims and the fight against fraud. The result? Higher premiums for everyone, a heavier burden on honest customers and huge financial losses for the industry.

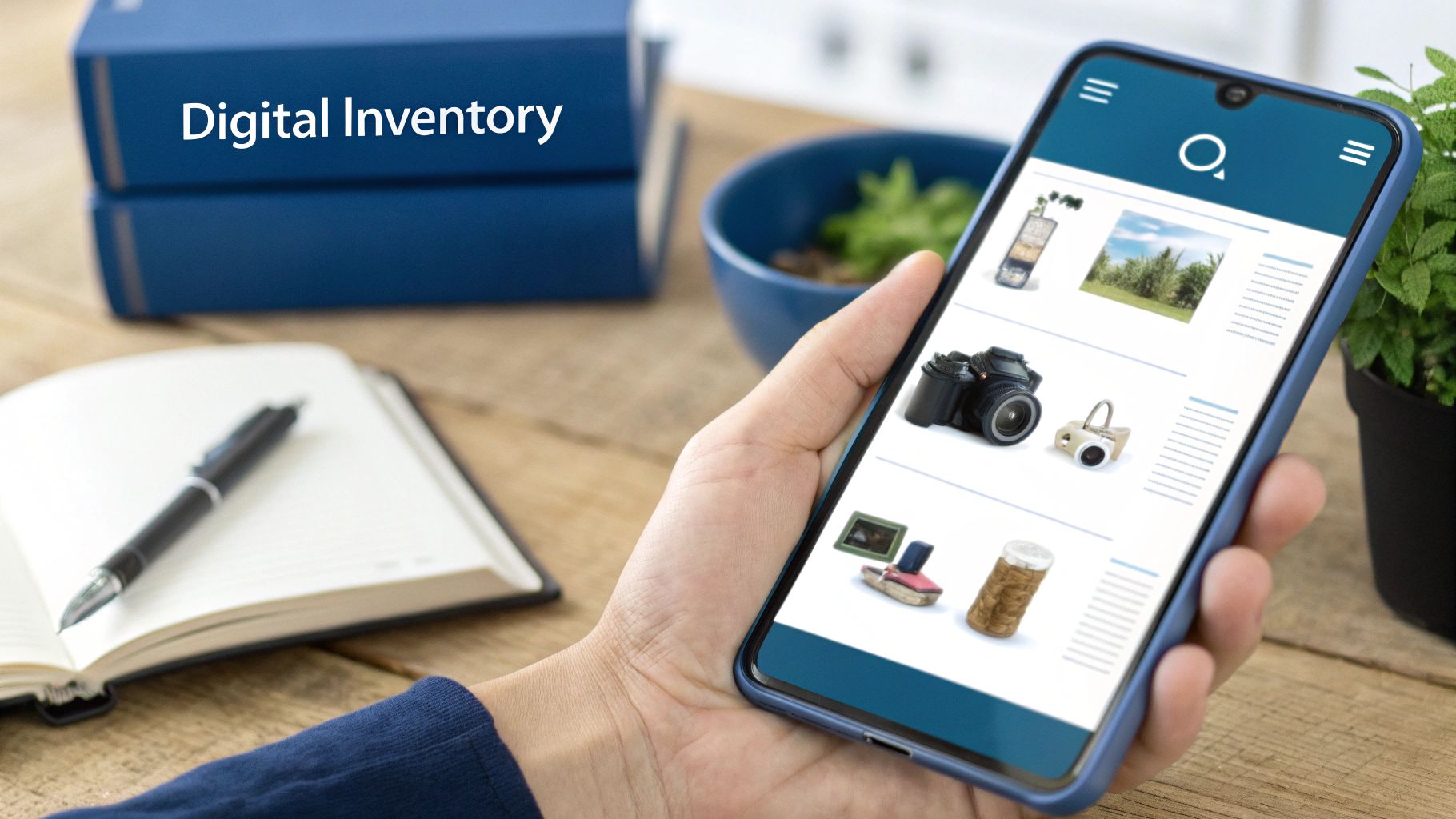

The Power of a Digital Inventory

This is where a modern solution like a digital inventory completely changes the game. Instead of scrambling to piece together evidence after a disaster, you create a solid, verifiable record of your belongings beforehand. A pre-existing, timestamped log of your possessions turns a stressful claims process into a straightforward verification exercise.

With a digital inventory platform, you can:

- Catalogue Your Items: Simply go from room to room and log everything you own.

- Add Photographic Evidence: Snap clear photos of each item to capture its exact condition.

- Record Key Details: Note down makes, models and serial numbers for your valuable electronics and appliances.

- Store Proof Securely: Everything is kept in a secure, cloud-based vault that won’t get lost in a fire or flood.

By creating this record when you take out your policy, you build an undeniable source of truth. When it’s time to claim, you simply share this verified list with your insurer. It accelerates payouts and cuts out the potential for conflict.

The UK home insurance market is under enormous pressure. Combined operating ratios have been over 100% since 2020, thanks to volatile weather and rising inflation. Platforms like Proova are designed to tackle these exact problems head-on. By letting users catalogue their belongings with timestamped photos and serial numbers through a free app, they help slash fraud and get genuine claims paid faster. In a market where insurers are battling rising claim numbers and supply chain issues, this approach is vital. You can read more about the challenges in the UK home insurance market from Oxbow Partners.

Taking a proactive approach helps everyone. It gives you the peace of mind that your claim is backed by irrefutable proof and it gives insurers the confidence to settle quickly and accurately. That’s how you build a better, more trustworthy relationship.

Using Digital Inventories to Transform Insurance

The insurance industry is in the middle of a huge shift, moving away from a model that just reacts to disasters towards one that proactively manages risk. At the heart of this change are digital inventory platforms, which are completely rethinking how a contents insurance policy works, right from day one.

The idea is simple but powerful: create a clear, verified record of your possessions before you ever need to make a claim. Instead of relying on guesswork and vague estimates, both you and your insurer have a precise, shared understanding of what’s covered and its condition from the outset.

This simple act of documentation builds a foundation of trust and transparency. It turns the contents insurance definition from an abstract promise on paper into a tangible, evidence-backed partnership that benefits everyone.

A New Standard For Underwriting And Risk Assessment

For insurers, one of the biggest headaches has always been accurately assessing risk. Traditionally, this involved a lot of guesswork. For higher-value homes, it might mean sending out a surveyor for a costly and time-consuming physical inspection. Digital inventories make this process faster, cheaper and far more accurate.

When a policyholder provides a comprehensive digital record of their belongings, the insurer gets a crystal-clear picture of the risk they are taking on. This allows them to price premiums more accurately, ensuring customers pay a fair price that truly reflects their specific level of cover.

This upfront clarity also shuts the door on a common type of fraud known as 'after-the-event' fraud. This is where someone damages an item, takes out an insurance policy and then claims for the pre-existing damage a few weeks later. A timestamped inventory proves the condition of items when the policy began, making this kind of deception nearly impossible.

A verified inventory establishes an undeniable baseline of truth. It removes ambiguity from the underwriting process and equips insurers with the data they need to offer better-priced, more sustainable policies.

This move towards evidence-based underwriting is not just about stopping fraud. It is about building a more resilient insurance model. To get a better sense of the technology that makes this possible, you can find out more by going inside Proova’s vault and the tech securing insured items.

Creating A Faster, Fairer Claims Process

Of course, the most significant benefit for you, the policyholder, comes when the worst happens. Dealing with the stress of a burglary or a house fire is hard enough without the added anxiety of a long, drawn-out claims process. With a digital inventory, the experience is completely different.

Instead of trying to remember every single lost item while you're still in shock, you already have a complete and detailed list ready to go. The claims process shifts from a painful negotiation based on hazy memories and old receipts to a straightforward verification exercise.

An adjuster can quickly and confidently assess the loss against the pre-existing, timestamped record. There’s no need for long debates over whether an item existed, its condition or its value—the proof is already there. This creates a win-win scenario for everyone.

The table below breaks down just how different the claims journey becomes.

Traditional vs Digital Claims Process

| Process Step | Traditional Method (Pain Points) | Digital Inventory Method (Benefits) |

|---|---|---|

| 1. Reporting the Loss | Policyholder must recall every item from memory, often while distressed. | Policyholder simply shares their pre-existing digital inventory with the insurer. |

| 2. Providing Proof | A frantic search for receipts, photos or bank statements to prove ownership and value. | Proof of ownership, condition and value is already documented and timestamped. |

| 3. Claim Assessment | Adjuster investigates, often leading to disputes over item existence or condition. | Adjuster verifies the loss against a trusted, pre-agreed record, reducing friction. |

| 4. Payout Decision | A slow, stressful process that can take weeks or months to resolve. | A fast, evidence-based process leading to much quicker claim settlement and payout. |

As you can see, a digital inventory doesn’t just speed things up; it removes much of the emotional and administrative burden that makes traditional claims so difficult.

The idea of using technology for meticulous record-keeping is not limited to personal contents. For example, modern digital inventory features in property management apps are used to create comprehensive property condition reports, showing just how versatile these tools have become.

Ultimately, this shared source of truth builds a stronger, more trusting relationship between the customer and the insurer. It ensures genuine claims are paid quickly and efficiently, while protecting the entire system from the fraud that drives up costs for everyone.

Securing Your Possessions and Peace of Mind

Throughout this guide, we’ve covered the ins and outs of contents insurance, showing how it acts as a vital financial shield for your personal belongings. It's the safety net that catches you after a fire, flood or theft. But here's the catch: its real value hinges entirely on your ability to prove what you actually owned.

This brings us to a huge challenge facing both homeowners and insurers. The shadow of insurance fraud—from small exaggerations to organised crime—drives up costs for everyone. It forces insurers to be cautious, placing a heavy burden of proof on honest customers right when they are at their most vulnerable. Relying on faded receipts and hazy memories just does not cut it anymore.

Embracing a Proactive Approach

The good news is that the industry is shifting towards a more evidence-based model and you can get ahead of the curve. Digital inventory solutions are not just a nice-to-have; they are fast becoming an essential tool for any modern policyholder. By creating a clear, timestamped record of your possessions from day one, you remove all the guesswork.

This simple, proactive step completely changes the game. It strengthens your position, tackles the fraud problem head-on and turns the claims process from a potential argument into a straightforward verification. You’re no longer asking an insurer to take your word for it—you’re providing undeniable proof of ownership, allowing them to settle genuine claims faster and with far more confidence.

Adopting technology to document your belongings empowers you to secure your own peace of mind. More than that, it contributes to a more transparent, efficient and fair insurance ecosystem for everybody involved.

By preparing today, you make sure your contents insurance will do exactly what you paid for when you need it most. You protect your possessions and you also help build a more trustworthy and affordable insurance market for the future.

Frequently Asked Questions About Contents Insurance

Getting your head around the small print of contents insurance can feel like a chore but it's where the real value lies. A few key questions pop up time and time again and getting clear, simple answers is the best way to make sure you’re properly protected without overpaying.

We'll walk through the essentials: how to value your stuff, what happens when you take it out of the house and what an ‘excess’ actually means for you. Nail these points and you’ll be in a much better position to choose the right cover.

How Do I Accurately Calculate the Value of My Contents?

The only real way to do this is to go room by room and create a list of everything you own. For each item, you need to figure out what it would cost to buy it brand new today. Insurers call this ‘new for old’ cover and it’s designed to give you enough cash to replace everything without being out of pocket.

It's easy to forget things tucked away in the garage, the loft or the garden shed, so make sure to include those too. If you have high-value items like art, antiques or expensive jewellery, it’s always a good move to get a professional valuation. Using an app to digitally photograph and log everything simplifies this job massively and gives you a ready-made inventory for your insurer.

Are My Belongings Covered When I Take Them Outside My Home?

Your standard contents policy is designed to protect your belongings while they're inside your home. Once you step outside, that cover usually stops. If you want your laptop, phone or bike protected while you're out and about, you'll need to add an extra layer to your policy.

This add-on is often called ‘personal possessions cover’ or ‘all-risks cover’. It’s an optional extra that will bump up your premium a bit but it’s crucial for covering theft, accidental damage or loss when you're away from home. Always double-check the single-item limit on this extra cover to be certain your most valuable portable gadgets are fully protected.

What Is an Excess and How Does It Work on a Contents Claim?

The excess is simply the amount you agree to pay towards any claim you make. For example, if you have a £250 excess and claim for a stolen TV worth £1,000 , your insurer will pay out £750 . You cover the first £250 .

Policies usually have two types of excess. The compulsory excess is set by the insurer and is non-negotiable. The voluntary excess is an amount you can choose to add on top.

Choosing a higher voluntary excess can often bring down your annual premium, which sounds great. But you have to be honest with yourself—could you comfortably afford to pay that total excess if you needed to make a claim tomorrow? If not, it could make your policy useless when you need it most.

Take the guesswork out of your contents insurance. With Proova , you can create a secure, timestamped digital inventory of your possessions, ensuring you have the undeniable proof needed for a fast and fair claims process. Protect your belongings and your peace of mind by getting started today. Visit https://www.proova.com to learn more.