A Practical Guide: home contents insurance for tenants

It's a classic renter's mistake: assuming the landlord's insurance has you covered. The truth? It absolutely does not.

That’s where home contents insurance for tenants comes in. Think of it as your personal financial safety net, a specific policy you take out to protect everything you own inside your rented home—from your laptop and TV to your sofa and clothes—against disasters like theft, fire or flooding.

Why Your Landlord's Insurance Is Not Enough

Believing the landlord's policy protects your stuff is one of the most common and costly assumptions a tenant can make. A landlord is only responsible for insuring the physical structure of the building and any items they personally own within it, like the fridge or a washing machine that came with the flat.

Your possessions are entirely your responsibility.

This means if a pipe bursts in the flat above and ruins your electronics or a kitchen fire destroys your belongings the landlord’s insurance will only pay to fix the walls, floors and ceiling. The cost of replacing your laptop, telly, clothes and furniture? That falls squarely on you.

Without your own policy, you’d be left with the staggering bill of starting from scratch.

The Real Cost of Being Uninsured

Take a moment and try to add up the value of everything you own. It's easy to just think about the big-ticket electronics but the total climbs surprisingly fast when you start listing every single item.

- Furniture: That sofa, bed, wardrobe and dining table all add up.

- Electronics: Laptops, TVs, games consoles, speakers and tablets.

- Clothing and Personal Items: Your entire wardrobe, shoes, any jewellery and sentimental keepsakes.

- Kitchenware: All the pots, pans, cutlery and small appliances you've collected.

Losing all of that in one go could easily run into thousands of pounds. For most of us, finding that kind of cash out of the blue just isn't realistic. This is precisely the nightmare scenario that contents insurance is designed to prevent.

The Importance of Honesty and Provability

While insurance is a crucial safety net the entire system is built on trust. A genuine claim, backed up by solid evidence, is exactly what the policy is for. Unfortunately, insurance fraud is a serious issue with consequences that affect everyone.

Insurance fraud isn’t a victimless crime. When people make fraudulent claims, insurers have to spread that cost out which forces them to raise premiums for everyone. It means every honest tenant ends up paying more because of the actions of a dishonest few.

Throughout this guide, we're going to come back to the importance of provability . Being able to prove you owned something is the foundation of a successful claim. This focus on honesty doesn't just protect your claim; it helps keep the insurance system fair and affordable for all renters.

How to Accurately Value Everything You Own

It’s easy to do but underestimating the value of your possessions is the fastest way to find yourself underinsured. When you get a quote, you'll be asked for a sum insured – that’s the total amount the policy would pay out in a complete disaster. Guessing this figure is a huge gamble. Aim too low and you'll be seriously out of pocket when you need to replace everything.

The only reliable method is to create a detailed inventory. It might sound like a chore but it does two critical jobs. First, it gives you a rock-solid, accurate figure for your policy. Second, it becomes your proof if you ever have to claim, showing the insurer exactly what you owned and what it was worth.

Think of it this way: an honest inventory is the foundation of a fair policy and a painless claims process. Without one, you're just hoping for the best.

A Practical Room-by-Room Method

The trick is to be methodical. Don’t try to do it all at once. Just tackle your home one room at a time with a notepad, a spreadsheet or even an inventory app on your phone. The goal is to list everything you'd need to buy again and estimate its current replacement cost.

Start with the big-ticket items, sure, but don't ignore the small stuff. It’s the combined value of all the little things that often catches people by surprise.

- Living Room: List the sofa, TV, sound system, coffee table and bookshelves. Did you buy the rugs or curtains? Add them. Then think about the smaller things: games consoles, books, DVDs and any art or decorative bits you’ve collected.

- Kitchen: It's more than just the microwave. Add up the cost of every pot, pan, plate and glass. Don’t forget the cutlery and smaller appliances like your kettle, toaster or coffee machine. It all adds up, often to hundreds of pounds.

- Bedroom: This room is almost always undervalued. Tally up your bed frame, mattress, wardrobe and drawers. Then comes the big one: realistically estimate the replacement cost of your entire wardrobe—every coat, pair of shoes and outfit.

- Home Office: Your laptop or PC is the obvious one but what about the desk, chair, printer and all the other tech accessories you rely on for work or study?

This exercise is often an eye-opener, revealing just how much stuff we actually own. If you're curious how your final tally measures up, you can get a sense of the national picture by exploring the UK average house contents value.

New-for-Old vs. Indemnity Cover

As you’re adding up the value of your things, you need to know what kind of cover you’re getting. This directly impacts how you should calculate your sum insured. The two main types are ‘new-for-old’ and ‘indemnity’.

Let’s use a simple example: a thief steals your five-year-old television.

New-for-Old Cover: Your insurer pays out enough for you to go and buy a brand-new, equivalent model today. This is the most common type of contents cover and offers the best protection, meaning you should value your items based on their new price.

Indemnity Cover: Your insurer pays you what your five-year-old TV was actually worth, factoring in all that wear and tear. The payout will be much less than a new one would cost. These policies are cheaper but leave you to find the cash to cover the difference.

For almost every tenant, new-for-old cover is the way to go. It’s designed to put you back in the position you were in before the loss, without you having to dip into your savings. Because of this, when you build your inventory, you should always use the cost of replacing each item with a brand-new equivalent.

Just be honest. Deliberately inflating values is a form of insurance fraud. It has serious consequences and ultimately just drives up the cost of insurance for everyone.

Understanding Your Policy Cover And Optional Extras

Getting your head around a tenants' contents insurance policy is way simpler than it sounds. At its core, every standard policy is there to protect your stuff against a specific list of risks, known in the industry as insured perils . These are the big-ticket events that could damage or destroy your belongings and they’re the foundation of your financial safety net.

Think of these perils as the built-in protection you get right out of the box. They almost always cover major dramas like fire, theft (or attempted theft), flooding and storm damage. So, if your flat gets burgled or a burst pipe ruins your sofa, this is the part of the policy that kicks in to help you make a claim.

But a standard policy is just the starting point. It's a solid base but let's be honest, life is full of weird and wonderful accidents that fall outside these big categories. This is where optional extras, or add-ons, really prove their worth, letting you build a policy that actually fits your life.

Tailoring Your Cover With Key Add-ons

While the standard cover handles the major disasters, optional extras are there to fill in the gaps for everyday life. They let you extend your protection beyond the four walls of your home and cover those "oops" moments that can be surprisingly expensive.

These add-ons aren't compulsory but picking the right ones can make a world of difference.

- Accidental Damage Cover: This is one of the most popular extras for good reason. It’s for those one-off, unintentional incidents. Dropped your laptop down the stairs? Spilled red wine on a brand-new rug? A standard policy won't touch that but Accidental Damage cover will.

- Personal Possessions Cover: This one extends your insurance to the outside world. It protects the things you carry around with you, like your mobile, keys, wallet or headphones, against theft or loss when you're out and about. It usually covers you anywhere in the UK and sometimes even worldwide.

- Tenants' Liability Cover: This is a huge one for renters. It protects you if you accidentally damage your landlord’s property—think their furniture, carpets or fixtures and fittings. Without it, you could lose your security deposit or even face a massive bill for repairs.

These extras are designed for specific risks, so it’s vital to be straight about what you need. Trying to claim for a stolen bike under your standard policy won't fly if you didn't specifically add it. Honesty and accuracy are everything when it comes to making sure your claim gets paid which ultimately helps keep the system fair for everyone.

The Cost and Value of Customisation

Adding extras will nudge your premium up but often not by as much as you'd think. The average cost of contents insurance for tenants in the UK can start from as little as £40-£50 a year for up to £50,000 in basic cover. The typical renter ends up paying around £138 annually once extras are added. For example, you might pay an extra £14 for accidental damage, £16.60 to cover a £1,500 laptop away from home or £45.10 for a £2,000 bike. Legal cover adds about £21.10 while £5,000 in personal possessions cover tacks on £30.90 and home emergency cover comes in at £42.70 . You can explore a more detailed breakdown of these average insurance costs to see how it all adds up.

Figuring out which extras are worthwhile comes down to your own circumstances. A keen cyclist will see huge value in specific bicycle cover while someone who never takes their laptop out of the house might give it a miss. The goal is to only pay for the protection you genuinely need.

To make things a bit clearer, here’s a simple table comparing what's usually included as standard versus what you'll need to add on.

Comparing Standard vs Optional Insurance Cover

| Feature | Included in Standard Policy? | Typical Use Case | Average Annual Cost (Add-on) |

|---|---|---|---|

| Theft, Fire & Flood Cover | Yes | Protection if your home is burgled or your possessions are damaged by fire or flooding. | N/A |

| Accidental Damage | No (Optional Extra) | You drop and smash your tablet screen while at home. | £14 |

| Personal Possessions | No (Optional Extra) | Your mobile phone is stolen while you’re on the bus. | £30.90 for £5,000 cover |

| Tenants' Liability | No (Optional Extra) | You accidentally spill paint, permanently staining the landlord's carpet. | Included in some, extra on others |

Ultimately, a well-chosen policy is all about peace of mind. By mixing solid core cover with the right optional extras, you create a shield against both major disasters and minor mishaps, making sure you’re not left facing an unexpected financial crisis on your own.

Navigating The Claims Process With Honesty

The moment you discover your flat’s been burgled or a burst pipe has wrecked your things is awful. It’s stressful, chaotic and the last thing you want to think about is paperwork. But having a clear plan for making an insurance claim makes all the difference and the entire process hinges on one simple thing: honesty.

The first few steps you take are crucial. If it’s a theft or vandalism, your very first call should be to the police. They'll issue a crime reference number , which is non-negotiable for your insurance claim. For something like a fire or flood, your absolute priority is safety. Once you're secure, your next call is to your insurer to let them know what’s happened.

This is where that detailed inventory you (hopefully) made earlier becomes your most powerful tool. It’s the difference between a vague, stressful attempt to remember everything you owned and a concrete, provable list of lost items. Trusting your memory during a crisis is a recipe for disaster.

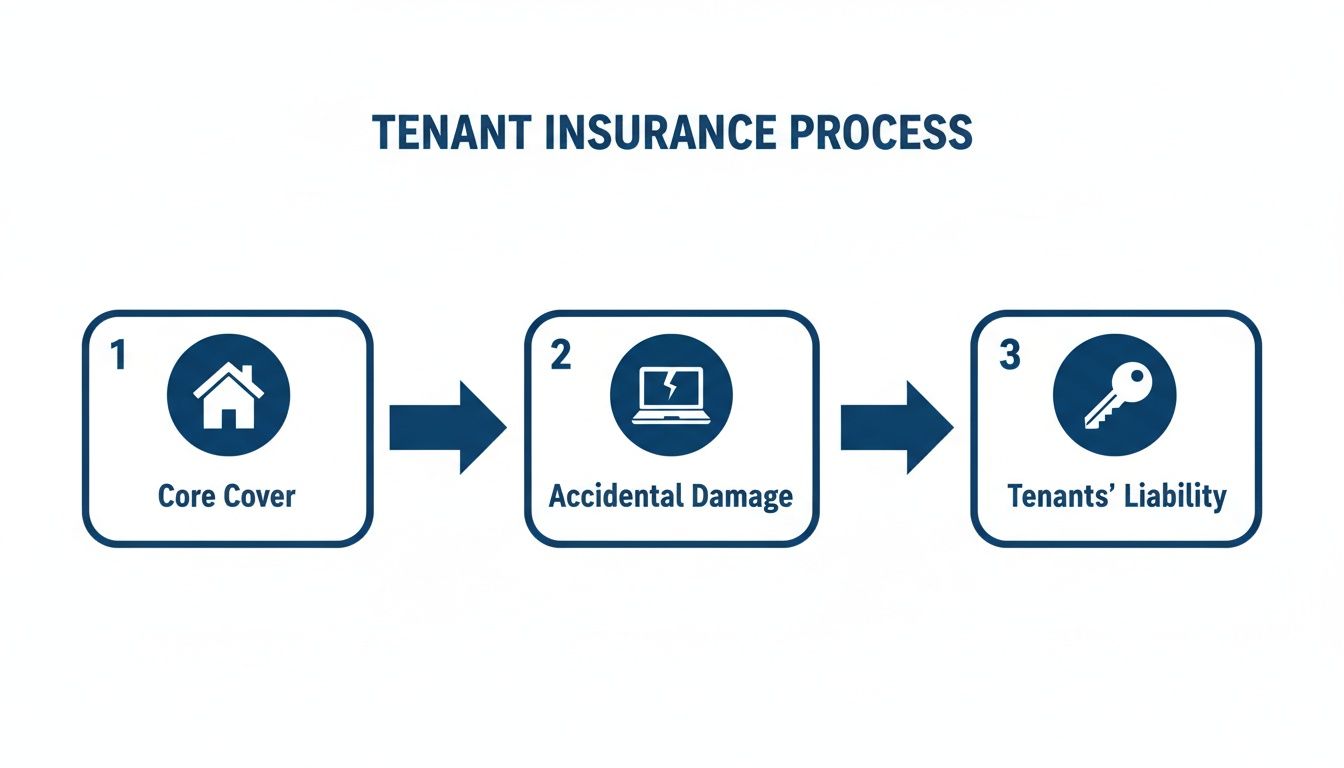

This infographic breaks down how a solid tenants' insurance policy is structured, giving you layers of protection.

As you can see, the Core Cover is the foundation but adding things like Accidental Damage and Tenants' Liability creates a safety net that truly has you covered.

The Heavy Cost Of Insurance Fraud

It can be tempting. You might think, "What's the harm in adding a few extra things to the list? Or bumping up the value of my stolen laptop?" It can feel like a harmless way to get a little extra back from a massive company but insurers and the law see it very differently. This is insurance fraud and the consequences are severe.

Insurance companies have incredibly sophisticated ways to validate claims. They scrutinise everything for inconsistencies, compare values against market rates and will dig for proof like receipts or photos. If they suspect fraudulent activity, they will investigate thoroughly.

Getting caught means your entire claim will be rejected, leaving you with nothing. Worse, your policy will be cancelled and you could be blacklisted on the Insurance Fraud Register. This makes it incredibly difficult and expensive to get any kind of insurance in the future. In serious cases, it can even lead to a criminal record.

Why Honesty Protects Everyone

The fallout from insurance fraud goes far beyond the individual. It's not a victimless crime. When insurers have to pay out on fraudulent claims, those costs don't just vanish—they get passed on to every single policyholder through higher premiums.

Put simply, every dishonest claim makes home contents insurance for tenants more expensive for honest people who just want a fair safety net. Upholding integrity is a collective responsibility that keeps the whole system affordable and working for when genuine disasters strike.

To make sure your claim goes as smoothly as possible, you can learn more and master the home insurance claims process with our guide.

Building A Strong And Provable Claim

Once you file your claim, your insurer will assign a claims handler to your case. Their job is to assess the loss and figure out a fair settlement based on your policy. To do that, they need evidence.

Your claim needs to be as detailed and accurate as you can possibly make it.

- Your Inventory: Hand over the detailed list of lost or damaged items you prepared.

- Proof of Ownership: This is vital. Dig out any receipts, bank statements or even original packaging for valuable items.

- Photographic Evidence: Before you touch or clear up anything (as long as it's safe), take clear photos or videos of the damage.

- Official Reports: Provide the police crime reference number or any reports from the fire service.

Being organised and upfront from the get-go makes the process faster and far less stressful. It proves your claim is legitimate and helps the insurer get you the support you need, as quickly as possible.

How Technology Is Making Insurance Fairer

The insurance industry has a reputation for being a bit old-fashioned but that's finally starting to change. New technology is paving the way for a fairer, more transparent experience for tenants who want to protect their belongings. We're moving beyond clunky websites and long call centre queues to a world where the proof you need is right in your hands.

This shift can't come soon enough. Despite the very real risks of theft or damage, only 46% of private tenants in the UK currently have contents insurance. That's a worrying drop from 51% just a year earlier. Many renters think their stuff isn't worth much but research shows 62% estimate their possessions are actually worth over £5,000 , revealing a massive gap in protection. You can dig into the full findings on tenant insurance uptake to see the scale of the problem.

At the heart of any insurance claim is a simple question: can you prove what you owned and what condition it was in? For years, this has been the biggest hurdle. Now, technology is solving it head-on.

The Power of Provable Ownership

Picture this: you've been burgled. Your insurer, quite reasonably, asks for a list of everything that was taken, along with proof you owned it. Trying to remember every single item while you're already stressed is hard enough, let alone digging up receipts for things you bought years ago. It’s a nightmare scenario.

This is exactly where modern tools like inventory apps completely change the game. They let you create a verifiable, time-stamped digital record of your possessions before anything goes wrong. You can log your electronics, furniture and valuables, upload photos and note down serial numbers to build an undeniable inventory.

This digital record becomes your definitive proof of ownership. It wipes out the guesswork and ambiguity, turning what could be a long, drawn-out dispute into a straightforward verification process.

This simple, proactive step fundamentally changes the dynamic between you and your insurer, building a relationship based on trust from the very beginning.

Benefits for Both Tenants and Insurers

This move towards verifiable inventories creates a genuine win-win. It makes the entire system of home contents insurance for tenants more honest and efficient for everyone involved.

For you, the tenant, the upsides are obvious:

- Faster Claims: With your proof already on file, insurers can process your claim much more quickly. You get the money you need to replace your items without frustrating delays.

- Less Stress: It completely removes the painful task of trying to remember every lost item and the friction that comes with having to prove your case.

- Fairer Payouts: A detailed inventory ensures you claim for the true value of your belongings, reducing the risk of being underinsured or underpaid.

And for the insurers? This technology gives them the confidence to act swiftly on legitimate claims. It helps them accurately assess risk from the outset and crucially, weed out fraudulent activity.

Tackling Fraud and Keeping Costs Down

Insurance fraud isn't a victimless crime. When people make exaggerated or completely false claims, the cost gets passed on to every single honest policyholder through higher premiums. Technology that establishes provable ownership makes this kind of deception far more difficult.

By giving insurers a clear, pre-incident record of what a tenant owns, it helps shut down 'after-the-event' fraud—where someone might take out a policy after losing or damaging an item and then try to claim for it. When insurers can confidently filter out dishonest claims, they reduce their losses.

Ultimately, those savings can be passed on to customers. By embracing tech that promotes honesty and provability, the insurance industry can work to keep premiums lower for the vast majority of tenants who just want fair, reliable protection for the things they own.

Finding The Right Policy For Your Rented Home

Once you have a clear idea of what you need to protect, you're ready to start looking for the right home contents insurance for tenants . It’s tempting to just grab the cheapest quote from a comparison site but the real value is always in the details, not the headline price. A policy that seems like a bargain upfront could end up costing you dearly if it fails to pay out when you need it most.

The key is to look beyond the premium and scrutinise what you’re actually getting for your money. Before diving specifically into tenant insurance, a broader understanding of how home insurance works in general can be a big help. For a general overview of home insurance options and how to protect your property, you might find this guide useful.

Looking Beyond The Price Tag

When you compare policies, there are three critical elements to check that will determine how useful the insurance actually is in a real-world scenario. Don't skim over these—they can make all the difference between a successful claim and a frustrating rejection.

- The Policy Excess: This is the amount you have to pay towards any claim. A higher excess usually means a lower premium but make sure it’s an amount you could comfortably afford if something went wrong.

- Single-Item Limits: Most policies have a limit on how much they will pay out for any one item, often around £1,500 . If you have a valuable laptop, a piece of jewellery or a high-end bicycle, you must check it doesn't exceed this limit. If it does, you'll need to list it separately.

- Insurer Reputation: Look up reviews for how insurers handle claims, not just how easy they are to buy from. A cheap policy is worthless if the provider has a reputation for being difficult when it really matters.

A Practical Checklist For Choosing Your Policy

To make sure you get the right cover, ask yourself a few practical questions. The answers will guide you towards a policy that truly fits your lifestyle, which is particularly important for those in specific living situations. Students, for example, often have unique needs and you can explore this further with a guide to student home contents insurance.

A good insurance policy is one you can forget about, confident that it has your back. It’s about securing peace of mind, not just ticking a box.

Think about these points before you commit:

- Do I need Accidental Damage cover for those inevitable spills and mishaps at home?

- Do I need Personal Possessions cover for my phone, laptop or keys when I’m out and about?

- Is my bicycle valuable enough to need specific cover against theft away from home?

- Does the policy include Tenants' Liability to protect my deposit from accidental damage to the landlord's property?

Answering these honestly ensures you only pay for the protection you genuinely need, equipping you with a policy that provides real security and value.

Frequently Asked Questions About Tenant Insurance

To wrap things up, let's tackle some of the most common questions tenants have when it comes to protecting their stuff. Getting the right contents insurance is all about knowing exactly what you're covered for, so you can have total peace of mind.

Is Home Contents Insurance a Legal Requirement for Tenants?

No, you’re not legally required to have contents insurance in the UK. However, don't be surprised if your landlord has a clause in your tenancy agreement that insists on it – specifically, they might require you to have tenants' liability insurance . This isn't for your belongings but to cover any accidental damage you might cause to their property, like spilling wine on a carpet or breaking a fixture.

Even if it’s not required, going without it is a huge gamble. If the worst happens – a fire, a flood or a break-in – you'd be footing the entire bill to replace everything you own out of your own pocket.

Does My Flatmate's Insurance Cover My Belongings?

Almost certainly not. A standard insurance policy is personal; it only covers the possessions of the person named on the policy documents. When you're in a shared house, everyone is responsible for insuring their own things.

It's a classic mistake to assume you're covered by a housemate's plan. To make sure your laptop, clothes and other valuables are safe, you need to sort out your own individual contents insurance.

A common point of confusion in shared living is whose responsibility covers what. When you share a home, you also share risks but insurance policies are personal. Relying on a housemate's cover is a gamble that will not pay off.

How Can I Get a Cheaper Insurance Premium?

There are a few straightforward ways to bring down the cost of your premium without having to cut corners on essential cover. A little bit of savvy thinking can lead to some decent savings.

- Increase Your Voluntary Excess: This is the amount you agree to pay towards any claim yourself. Opting for a higher excess signals to the insurer that you won't be claiming for minor incidents which often results in a lower premium. Just make sure it’s an amount you could comfortably afford if you needed to.

- Pay Annually: Paying for your policy in one lump sum is almost always cheaper than monthly instalments. Insurers often add interest to monthly payment plans, so you end up paying more over the year.

- Improve Your Security: Insurers love good security. If your rental has high-quality, insurer-approved locks on the doors and windows, you might be offered a discount on your premium.

For some more great advice on navigating the world of renting, check out 4 Things Every Renter Needs To Consider.

Protecting your belongings shouldn't be a matter of guesswork. With Proova , you can create a verifiable, time-stamped digital record of your possessions, making any future claims process simple and stress-free. Take control of your insurance by building a foundation of proof today at https://www.proova.com.