A Guide to the Insurance Fraud Bureau

Insurance fraud is not a victimless crime. It is a calculated act that hits every honest policyholder right where it hurts—their wallets. In the UK, the Insurance Fraud Bureau (IFB) stands as the central command post for the industry's coordinated fight against this problem, especially the organised criminal networks profiting from it.

The Hidden War on Insurance Fraud

Insurance fraud is a quiet but costly problem that affects millions of people across the UK. It is far from a harmless way to pocket a small payout; it is a deliberate deception that places a massive financial burden on the entire industry and, by extension, every single honest customer.

Each falsified claim and dishonest application adds to a rising tide of costs that insurers have to absorb. But those costs do not just disappear. They are passed directly onto policyholders through higher annual premiums for car, home and business insurance. In short, honest customers are left subsidising the illegal activities of a dishonest minority. This hidden "fraud tax" makes essential cover more expensive for families and businesses alike.

Why a Unified Approach Is So Critical

For years, individual insurers fought fraud from within their own silos. While they might catch a bit of low-level opportunistic fraud, they were missing the bigger picture. The real challenge comes from organised criminal gangs who are experts at spreading their scams across multiple companies, making their coordinated efforts almost impossible for a single insurer to spot.

This is exactly where an insurance fraud bureau becomes essential. By creating a central hub for sharing data, the industry can finally connect the dots between what look like unrelated claims and policies.

The Insurance Fraud Bureau (IFB) acts as the nerve centre for the UK's insurance industry. It pools data from hundreds of members to uncover patterns of fraudulent behaviour that would otherwise stay hidden. This collaborative intelligence is the key to disrupting complex criminal operations.

Understanding Public Attitudes to Fraud

Tackling the problem also means getting to grips with the social factors that drive it. Surveys offer a crucial window into public perceptions and the findings can be pretty unsettling. For instance, a recent YouGov survey commissioned by the IFB found that a staggering 17% of UK adults believe it is acceptable to lie on an insurance application to save money.

The study also shed light on some interesting demographic trends. It turns out that adults aged 25-34 were the most likely group to admit to deliberately lying on an application form, with 8% confessing they had done it. Geographically, Londoners were the most likely to admit to bending the truth on applications or claims, at 7% . You can explore more of these findings on insurance fraud statistics on the IFB's website.

This kind of data proves that fighting fraud is not just about having advanced detection systems. It is also about shifting public perception and making people understand its true cost.

How the Insurance Fraud Bureau Uncovers Criminal Networks

Think of the Insurance Fraud Bureau (IFB) as the central intelligence hub for the entire UK insurance industry. It is not a government agency or a police force, but a not-for-profit organisation funded by insurers. Its mission is laser-focused: to detect and dismantle organised insurance fraud. The real power of the IFB comes from its unique vantage point—it sees the bigger picture in a way no single insurer ever could.

At its heart, the IFB's strategy is all about secure, collaborative data sharing. Hundreds of insurers feed anonymised policy and claims data into a central system. This creates a massive, interconnected map of the insurance market, allowing analysts to spot suspicious patterns and connections that would otherwise fly completely under the radar.

This collaborative model is absolutely essential. Why? Because organised criminals are smart enough to spread their fraudulent activities across multiple companies to avoid getting caught. A single staged accident, for example, might involve claimants holding policies with five different insurers. To each individual company, it just looks like an isolated incident. But the IFB can see all the common threads linking them together.

Connecting the Dots with Data

The IFB uses powerful analytical tools to comb through millions of data points, hunting for anomalies and hidden relationships. It is like a digital detective agency, using clever algorithms to flag individuals, vehicles and addresses that pop up again and again in suspicious claims across the industry. This is how raw, disconnected data gets turned into actionable intelligence.

One of the most vital tools in this fight is the Insurance Fraud Register (IFR) . This is a national database that holds the records of individuals who have already been caught committing insurance fraud. When processing new applications or claims, insurers can check the IFR to stop known fraudsters from repeatedly targeting the industry. It acts as a collective memory, ensuring a criminal caught by one company cannot just move on to the next one without a trace.

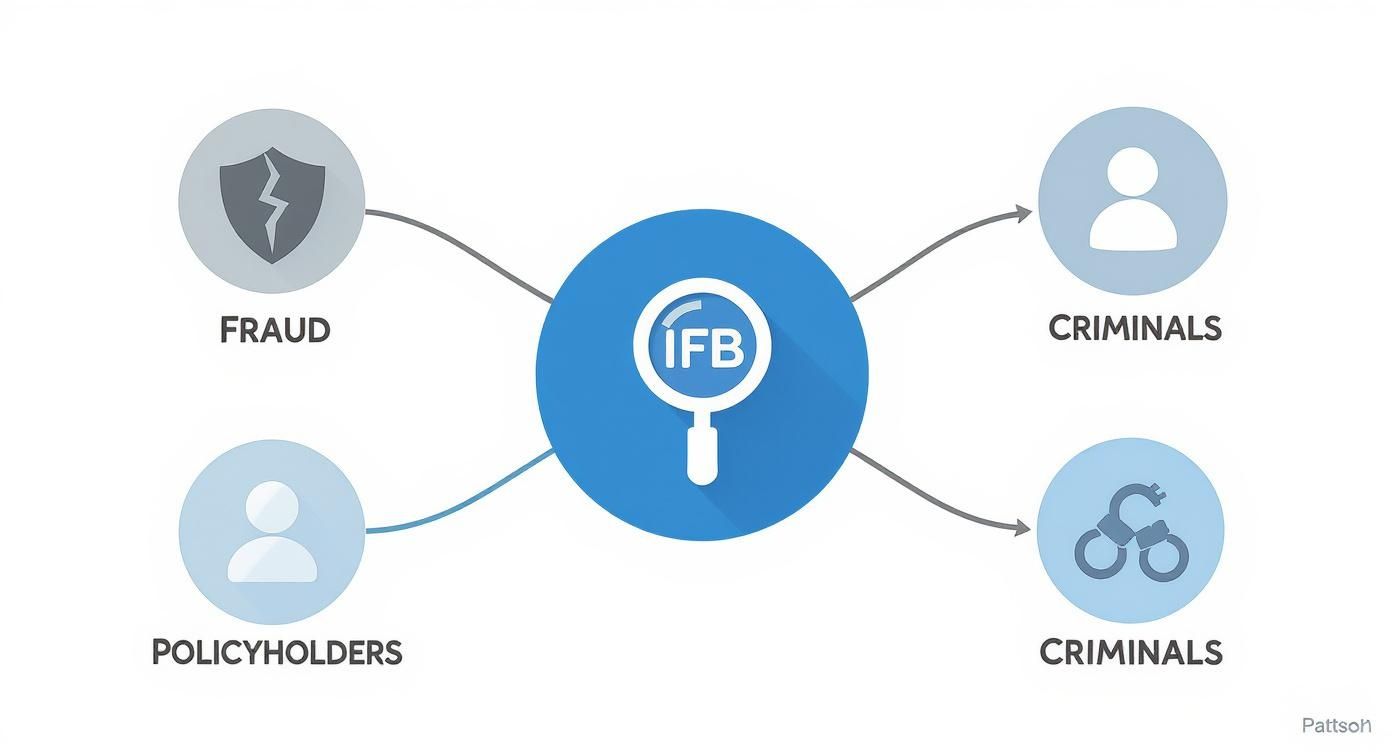

This infographic shows how the IFB sits right at the centre of the fight against fraud, connecting the dots between criminal activity and the protection of honest policyholders.

The visualisation really brings home the IFB's role as a crucial intermediary, using data to shield the public while enabling law enforcement to go after criminal enterprises.

From Digital Clues to Real-World Arrests

Spotting a suspicious network is just the beginning. The IFB’s intelligence teams then get to work enriching this data, building out a comprehensive picture of the suspected criminal operation. They carefully analyse the evidence to figure out the scale of the fraud, identify the key players and map out exactly how the network operates.

Once complete, this detailed intelligence package is handed over to police forces across the UK. It gives law enforcement a ready-made case, complete with hard evidence and clear links between the suspects. This collaboration is what turns digital patterns into tangible police investigations that lead to arrests, prosecutions and the complete dismantling of organised crime rings.

The IFB’s work is a perfect example of a public-private partnership. By combining industry data with police enforcement powers, they create a formidable opposition to insurance fraud that neither could achieve alone.

These criminal networks can be incredibly sophisticated, making investigations complex. To effectively take them down, the Insurance Fraud Bureau often has to delve into areas like the workings of the dark web , a common marketplace for stolen identities and fraudulent documents.

The results of this coordinated effort are massive. Every year, the IFB’s intelligence leads to hundreds of arrests and criminal convictions, stopping millions of pounds in fraudulent payouts. This does not just bring criminals to justice; it sends a powerful message that insurance fraud is a high-risk crime with serious consequences. Ultimately, it protects everyone’s premiums from being inflated by these illegal schemes.

The True Cost of a Seemingly Victimless Crime

It is a dangerous myth that insurance fraud is a ‘victimless’ crime. The reality is, it is a massive drain on the UK economy and it hits every single person with an insurance policy right where it hurts: their wallet. Every bogus claim, whether it is a small exaggeration or part of a large-scale organised scam, piles onto a mountain of costs that insurers have to manage.

And where do those costs go? They do not just vanish into a corporate black hole. They are passed directly onto honest policyholders through higher annual premiums. This means every family and business is paying a hidden ‘fraud tax’, making essential cover for cars, homes and businesses more expensive than it needs to be. It is a direct penalty for playing by the rules.

The Ripple Effect on Your Finances

The financial damage goes far beyond the initial fraudulent payout. To fight back, insurers have to pour money into specialist fraud teams, sophisticated detection software and continuous training. These are huge operational expenses that are baked directly into the price of insurance for everyone.

Think of it as an ongoing arms race. As criminals dream up new schemes, insurers must respond with even smarter defences. This investment is vital to protect the industry but its price tag is ultimately paid for by the premiums of law-abiding customers.

Insurance fraud isn't a clever game against a faceless corporation. It's a direct transfer of wealth from honest people to criminals, with every policyholder footing the bill for the industry's defence.

This cycle of fraud and prevention quietly inflates the cost of living and running a business in the UK. The money spent fighting criminals could be used to lower premiums or improve customer service. Instead, it is diverted to tackle illegal activity. To get a real sense of the scale, you can learn more about what insurance fraud really costs the industry .

Quantifying the Financial Damage

The numbers paint a stark picture. An insurance fraud bureau is essential for tracking these trends and the data reveals a deeply worrying rise in criminal activity. In 2025, the Insurance Fraud Bureau (IFB) reported a significant jump in detected fraud. To put that into perspective, Allianz UK alone uncovered £92.6 million in fraudulent activity in just the first half of the year—a staggering 34% increase from the same period in 2024.

This is not an isolated incident. The IFB also flagged a seven-fold increase in identity theft cases linked to insurance scams over the past year. As you can discover more about this surge in fraud , it is clear the financial threat is not just real; it is growing.

Hard data like this completely dismantles the idea of a victimless crime. It shows a clear, undeniable line connecting fraudulent acts to the rising cost of insurance for everyone. The work of an insurance fraud bureau, therefore, is not just about catching criminals. It is about protecting the financial wellbeing of every household and business that depends on fair and affordable insurance.

Mapping the UK's Fraud Hotspots

The real power of an insurance fraud bureau is not just in collecting data; it is in turning that mountain of information into targeted, real-world action. Instead of playing whack-a-mole with individual fraudulent claims, the Insurance Fraud Bureau (IFB) proactively analyses industry-wide data to spot geographical patterns and uncover organised criminal behaviour. This intelligence-led approach allows insurers and police to focus their resources where they will have the biggest impact: the specific towns and postcodes where fraud is rife.

This is not some academic exercise. It is about transforming millions of data points into a clear operational map. A map that guides enforcement, disrupts criminal gangs at a local level and protects communities from the ground up.

Pinpointing Problem Areas with Precision

The IFB’s data-driven strategy has been critical in shining a light on the UK's worst-affected areas for policy fraud, offering vital insights for insurers and the public alike. A key report, for example, revealed that West Yorkshire , Greater Manchester and the West Midlands were the top three hotspots in England. Within those regions, cities like Bradford, Oldham and Birmingham consistently topped the list.

The analysis did not stop there. Glasgow was identified as the primary hotspot in Scotland, while the Isle of Anglesey in Wales and County Fermanagh in Northern Ireland were flagged as the most affected regions in their respective nations. This level of detail is exactly what is needed for local police forces to launch targeted operations and for insurers to apply more rigorous checks on applications coming from these high-risk postcodes.

Understanding the Socio-Economic Drivers

Identifying a hotspot is one thing. Understanding why an area has become a breeding ground for organised fraud is another challenge entirely. The IFB's analysis often points towards deeper socio-economic factors that can create the perfect conditions for these scams to take hold.

These drivers often include:

- Economic Deprivation: Areas with higher unemployment or financial hardship can make people more susceptible to the lure of 'easy money' offered by criminal gangs.

- Densely Populated Urban Areas: Big cities offer a degree of anonymity, making it far easier for fraudsters to operate under the radar.

- Established Criminal Networks: Pre-existing organised crime groups often diversify their operations to include lucrative insurance scams, using the infrastructure they already have in place.

By looking beyond the statistics, the IFB paints a much fuller picture of the problem. This context is crucial for authorities and community leaders, helping them develop long-term strategies that tackle not just the symptoms but the root causes of the fraud itself.

"The IFB's geographical intelligence doesn't just show us where fraud is happening; it helps us understand the conditions that allow it to thrive. That insight is essential for building resilient communities and preventing future criminal activity."

From Data Maps to Enforcement Action

Ultimately, the goal of mapping these hotspots is to drive decisive action on the ground. When the IFB detects a surge in a specific scam, like staged ‘crash for cash’ incidents, it can immediately alert local police and share detailed intelligence packages. This is not just a vague tip-off; it can include names of suspected ringleaders, vehicle registrations and the exact tactics being used.

This collaborative approach ensures that enforcement is not random but laser-focused and effective. Armed with this evidence, police can launch investigations with a much higher chance of success, leading to arrests and prosecutions that can dismantle an entire criminal network. For a deeper look into these organised schemes, check out our guide on the crash for cash the persistent threat .

It is this proactive, localised strategy that lies at the heart of the IFB’s success, proving how shared data can protect everyone from the costly impact of insurance fraud.

Strengthening Your First Line of Defence Against Fraud

While an insurance fraud bureau is vital for tackling organised crime, the industry's real resilience starts on the front line with claims handlers and underwriters. For years, the standard approach was reactive: pay out a claim and only investigate later if something felt off. That is a bit like trying to dust for fingerprints after the burglars have already sold your telly.

A much smarter strategy is to flip this model on its head, moving from reactive investigation to proactive prevention. This means embedding solid verification checks right into the initial application and claims process. It is all about the provability of the claim and spotting red flags at the earliest possible moment, long before any money changes hands.

This proactive mindset turns the claims process from a potential weakness into your most powerful line of defence. It gives claims teams the tools they need to stop fraud in its tracks, rather than just cleaning up the expensive mess afterwards.

Shifting From Reactive to Proactive Measures

Making the switch to a proactive stance demands a fundamental change in how evidence is handled. Instead of taking things on trust, claims handlers need the ability to verify submitted documents and images instantly. For any business, this also means having robust internal security. A critical first step against all sorts of fraud is setting up strong internal controls, like establishing user-level IP restrictions for controlling access.

This approach does not mean treating every customer with suspicion. It simply acknowledges the reality that a determined minority will always try to exploit the system. By building verification tech into the point of submission, insurers can instantly flag inconsistencies that might point to fraud—anything from a digitally altered invoice to a photo with manipulated metadata.

The core idea behind proactive prevention is simple: verify first, pay later . This single change in workflow can save insurers millions by stopping fraudulent payouts and slashing the huge costs tied to post-payment investigations.

Adopting a proactive model has clear advantages over the traditional reactive one, as this table illustrates.

Proactive Prevention vs Reactive Investigation

| Approach | Proactive Prevention | Reactive Investigation |

|---|---|---|

| Timing | Checks are performed at the application or initial claims stage, before payment is made. | Investigations begin after a claim has been paid, based on suspicion or post-payment audits. |

| Cost | Significantly lower costs by preventing fraudulent payouts and avoiding expensive legal proceedings. | Extremely high costs associated with recovering paid funds, legal fees, and investigator salaries. |

| Success Rate | Very high success rate as fraud is stopped before any financial loss occurs. | Low success rate in recovering funds once they have been paid out to criminals. |

| Deterrence | Acts as a powerful deterrent, making the insurer a much harder target for fraudsters. | Offers little deterrence, as criminals often assume they won’t get caught after the fact. |

As you can see, preventing fraud is always going to be more effective—and cheaper—than chasing it.

Leveraging Technology for Real-Time Verification

The key to an effective proactive defence is technology. Modern verification platforms can analyse submitted evidence in real time, flagging suspicious elements for immediate review. This empowers claims handlers to make faster, more accurate decisions without needing to be digital forensics experts themselves.

Tools like Proova , for example, allow claims teams to instantly validate the authenticity of documents and images. A handler can check if a photo of a damaged item was taken when and where the claimant says it was, or if an invoice has been tampered with. This capability is crucial for combating ‘after the event’ fraud, where someone damages an item, takes out a policy and then claims a few weeks later.

By integrating such platforms into their workflow, insurers can create a claims process that is not only faster and more efficient for honest customers but also far more secure against fraud. This technological shield makes it significantly harder for criminals to succeed, turning the first line of defence into a formidable barrier. To see how this works in practice, you can learn more about fighting fraud before it happens with the power of verified evidence .

How to Report Suspected Insurance Fraud

In the fight against insurance fraud, one of our most powerful weapons is collective vigilance. While fraud bureaus provide the analytical firepower, they rely on tip-offs from the public and honest industry professionals to point them in the right direction. Recognising and reporting suspicious activity is a responsibility we all share.

Every scrap of information helps build a stronger case against criminals, protecting everyone from the rising cost of fraud. Stepping forward might feel daunting but the process is surprisingly straightforward and completely confidential. The Insurance Fraud Bureau (IFB) has made it simple and secure for anyone to share what they know.

Using the Confidential Cheatline

The main way to report your concerns is through the IFB's Cheatline . This dedicated service is designed to handle sensitive information with the utmost discretion and is available to both the public and insurance industry insiders.

You can report fraud in two ways:

- Online Form: A secure form on the IFB website lets you provide details at your own pace.

- Phone Line: You can speak directly to a trained professional by calling 0800 422 0421 .

The entire process is 100% anonymous . You will not be asked for your name or contact details and your information will never be shared. This guarantee is vital, as it encourages people to come forward without any fear of reprisal.

Every report, no matter how small the detail may seem, contributes to a larger intelligence picture. What you know could be the missing piece of the puzzle that helps investigators connect the dots and dismantle a criminal network.

What Happens After You Make a Report

Once you have submitted your information, it goes directly to the IFB's expert intelligence team. They will analyse the details you have provided, cross-reference them with millions of records in their central database and look for links to other suspicious activities.

If the information points towards an organised criminal operation, the IFB will build a comprehensive evidence package. This package is then securely passed to a dedicated police force to kick off an investigation and take enforcement action. Your contribution directly fuels the process that brings fraudsters to justice.

Got Questions? We’ve Got Answers

Stepping into the world of insurance fraud can feel a bit complex. Let us break down some of the most common questions people have about how an insurance fraud bureau works and what it means for the industry.

Is the Insurance Fraud Bureau a Government Body?

You might think so, but no. The Insurance Fraud Bureau (IFB) is actually a not-for-profit company, set up and funded by the UK insurance industry itself.

While it works very closely with police forces and government agencies to bring fraudsters to justice, it is an industry-led organisation. Its main job is to be the central hub, coordinating the collective fight against organised insurance crime.

What’s the Difference Between Opportunistic and Organised Fraud?

This is a great question, as the distinction is really important. Opportunistic fraud is usually an individual act—think someone exaggerating the value of a stolen item on a genuine claim, or fudging a few details to get a cheaper premium. It is dishonest, but it is typically a one-off.

Organised fraud , on the other hand, is a different beast entirely. This involves criminal gangs running sophisticated, large-scale scams. We are talking about things like crash-for-cash schemes, where accidents are deliberately staged, or networks creating entirely fake claims for profit. The IFB's primary mission is to zero in on these organised criminal networks.

The real difference comes down to intent and scale. Opportunistic fraud is often a moment of poor judgement, while organised fraud is a calculated criminal enterprise designed to systematically exploit the insurance system.

Understanding this split is key. While individual insurers often handle opportunistic cases internally, it takes the coordinated power of an insurance fraud bureau to really dismantle the larger criminal operations that affect everyone's premiums.

Can I Report Fraud to the IFB Anonymously?

Yes, absolutely. The IFB runs a service called Cheatline , which is specifically designed to let you report suspected insurance fraud in complete confidence.

Your details are never shared and the entire process is anonymous. This protection is crucial because it gives people the confidence to come forward with information they might otherwise be reluctant to share.

How Does Data Sharing with the IFB Comply with GDPR?

Data privacy is non-negotiable and both the IFB and its members operate under strict data protection laws, including GDPR. The legal basis for processing data is the legitimate interest of preventing and detecting crime, which is a responsibility the industry takes seriously.

To safeguard privacy, information is anonymised or pseudonymised wherever possible and access is tightly controlled. The focus is always on spotting patterns of criminal activity, not on snooping on honest customers.

This secure framework ensures the collaborative effort to stop fraud is perfectly balanced with a firm commitment to individual privacy rights. The goal is to catch the criminals without ever compromising the data security of the millions of honest policyholders.

Strengthen your defence against fraudulent claims from the very first interaction. Proova provides the tools to verify evidence in real time, stopping fraud before it happens and protecting your bottom line. Discover how our platform can secure your claims process by visiting https://www.proova.com.