car breakdown cover uk: Find Your Best Policy Today

It’s a grim picture: your car splutters to a stop on a wet, miserable motorway. This is exactly the moment car breakdown cover UK is designed for. Think of it as your personal roadside rescue service, a safety net ready to catch you when things go wrong. While it's not a legal must-have like standard car insurance, it's the one thing that stands between you and a potentially massive bill for a single call-out.

Understanding Breakdown Cover And Its Value

At its heart, breakdown cover is a subscription service for roadside emergencies. You pay a manageable annual fee and in return, you get peace of mind. Instead of scrambling to find a local mechanic and facing an eye-watering, unpredictable bill for a tow, you have a network of professionals on standby, ready to come to your aid whenever your vehicle gives up.

This is so important because any car can fail, no matter how new or well-maintained it is. A flat battery, a sudden puncture or a mysterious engine fault can strike anyone at any time. Without cover, you’re not just stranded but also looking at a hefty bill just to get your car moved to the nearest garage.

Is It A Sensible Financial Precaution?

Absolutely. For a relatively small annual outlay, you’re protecting yourself against a much larger, unplanned expense. A single recovery truck and mechanic call-out can easily run into hundreds of pounds—often far more than the cost of a basic breakdown policy. For most UK drivers, it’s simply a smart financial move.

This whole system, however, is built on trust. When a recovery driver shows up, they’re assuming the fault just happened. That’s where the provability and integrity of claims become so critical.

The entire breakdown cover model relies on covering genuine, unexpected mishaps. When people make claims for pre-existing faults or issues they knew about, it weakens the whole system and ultimately drives up costs for every honest driver.

And this brings us to a major headache for both the insurance industry and its customers: insurance fraud.

The Hidden Cost of False Claims

When someone pretends an old, ignored fault has just happened, the insurer has to cover the loss. Those costs do not just vanish; they get passed on to every other policyholder in the form of higher premiums. Each dishonest claim makes essential car breakdown cover UK more expensive for the overwhelming majority of us who use it legitimately. The cost to all of us is significant.

It’s surprising, then, that so many drivers choose to take the risk. Research shows that around 20% of UK drivers have no breakdown cover at all, with younger drivers being the most likely to go without. You can discover more about these driver statistics and the financial gamble they're taking. This gap in cover leaves a huge number of people vulnerable to sudden, wallet-emptying repair bills.

Right, let's get into the different flavours of breakdown cover.

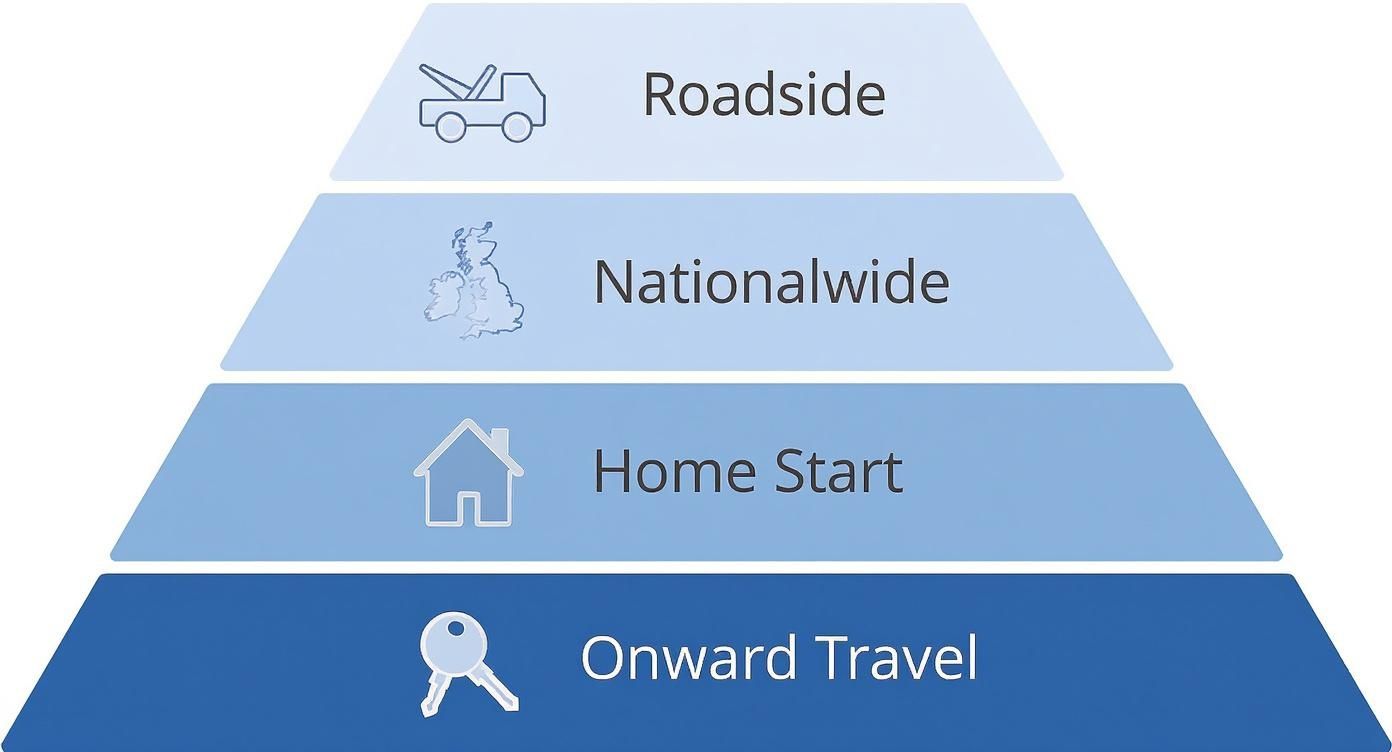

Choosing the right policy can feel a bit like staring at a restaurant menu with too many options. Providers use all sorts of different names, but when you strip it all back, the cover is usually built in layers. Think of it like a pyramid: you start with the essential base and add more protection as you go up.

Understanding these layers one by one is the simplest way to figure out what you actually need.

The Foundation: Roadside Assistance

This is your bread and butter, the most basic level of cover you can get. If your car gives up the ghost more than a quarter of a mile from your house, someone will come out to have a look. The goal is simple: get you moving again, right there and then.

If a roadside fix isn't on the cards, they'll usually give you a tow. But here’s the catch and it’s a big one: you'll likely be towed to the nearest garage. That might be miles from where you were going and it certainly might not be your trusted local mechanic. It gets you out of a jam but it's not always convenient.

Stepping Up: Nationwide Recovery

For anyone who ventures further than their local area, Nationwide Recovery is a game-changer. It includes everything from basic Roadside Assistance but it removes the fear of being stranded on the other side of the country.

If your car can't be fixed at the roadside, this cover means you, your passengers and your car will be taken to any single UK destination you choose. That could be your home, your holiday cottage or that garage you've trusted for years. It’s a proper safety net for long-distance drivers.

When Trouble Starts at Home: Home Start

It’s a classic story. You’re running late for work, you jump in the car, turn the key and… nothing. Just a sad clicking sound. Annoyingly, many standard policies won't help you if you're at home, which is where Home Start (sometimes called 'At Home' cover) comes in.

This adds protection for breakdowns that happen at your registered address or within a short distance of it (usually a quarter of a mile). It's one of the most common claims, so it's well worth considering.

The Full Works: Onward Travel

For those who simply can't afford for their plans to be ruined by a breakdown, there’s Onward Travel . This is the top-tier, all-singing, all-dancing option designed to keep your journey on track, no matter what.

If your car is headed to a garage for a longer stay, Onward Travel kicks in to soften the blow. The exact perks vary but you can generally expect things like:

- A replacement hire car , usually for a day or two.

- The cost of alternative transport covered, like train tickets.

- Overnight accommodation if you're stuck far from home and facing a lengthy repair.

It’s the priciest option, for sure. But if your car is essential for work or you have a family holiday planned, that peace of mind can be priceless.

To make it easier to see how these levels stack up, here’s a quick comparison.

Breakdown Cover Levels at a Glance

This table breaks down the main types of breakdown cover, showing what each one typically includes and who it’s best suited for.

| Cover Level | What It Covers | Best For |

|---|---|---|

| Roadside Assistance | Roadside repairs over ¼ mile from home. A tow to the nearest local garage if the car can't be fixed on the spot. | Drivers who stick to local journeys and don't mind which garage their car goes to. |

| Nationwide Recovery | Everything in Roadside Assistance, plus transport for you, your car and passengers to any single UK destination. | Anyone who drives long distances, travels for holidays or wants to get back home or to a specific garage. |

| Home Start | All the features of your chosen recovery level, but also covers breakdowns at or within ¼ mile of your home address. | Everyone. Car batteries often fail on cold mornings, making this one of the most-used features of breakdown cover. |

| Onward Travel | The most comprehensive cover. Includes everything above plus options like a hire car, overnight hotel or public transport costs. | People who absolutely cannot have their travel plans disrupted, such as business travellers or those on holiday. |

Ultimately, the best level of cover depends entirely on your driving habits and how much disruption you're willing to tolerate. By understanding what each tier offers, you can make a much more informed choice.

How Your Policy Cost Is Calculated

Figuring out the price of car breakdown cover UK isn't as simple as just picking a level of service off the shelf. Providers look at several key factors to get a sense of the risk you represent and they set your premium accordingly. It works a lot like standard motor insurance—they're building a picture of how likely you are to need their help.

One of the biggest pieces of that puzzle is your vehicle itself. The age, make and model of your car play a huge role in the calculation. An older car with a lot of miles on the clock is, statistically speaking, more likely to have a mechanical issue than a brand-new one. Because of that, it'll almost always attract a higher premium.

Personal vs Vehicle Cover

Another crucial distinction that really affects the price is whether you opt for 'personal' or 'vehicle' cover. Vehicle cover is tied to a specific car, which means anyone legally driving that car is covered if it breaks down. This is often the cheaper route but it's not as flexible.

Personal cover, on the other hand, protects you as an individual. It doesn't matter what eligible vehicle you're in—whether you're the driver or just a passenger—you're covered. This offers fantastic flexibility and peace of mind but it usually comes at a slightly higher cost because the scope of the cover is much broader.

This infographic gives you a good idea of the typical hierarchy of cover levels, which form the base cost of any policy you're looking at.

As you can see, each tier builds on the last, adding more comprehensive protection. Naturally, this directly influences the final price you'll pay.

Optional Extras And Market Factors

Finally, any optional extras you decide to add will nudge your premium up. These can include anything from European cover for your holidays abroad to key replacement or even specialist tyre protection. Think of each addition as another layer of financial protection and each one contributes to the total cost.

The UK roadside assistance industry was valued at approximately £1.8 billion , with forecasts predicting it could grow to nearly £2.2 billion . This growth is being driven by the demand for these more personalised packages that go well beyond a basic call-out.

While it’s a different world, seeing how commercial truck insurance rates are calculated can offer a useful perspective on the kinds of risk factors that influence policy costs across the board. When you understand all these different components, you can see exactly what you're paying for and why.

The True Cost Of Insurance Fraud

It’s easy to think of insurance fraud as a victimless crime against a massive, faceless company. But the truth is, when it comes to car breakdown cover UK , every single fraudulent claim sends ripples right through the system and honest drivers end up paying the price. This insurance fraud has a significant cost for the industry and all of us.

This kind of dishonesty isn’t always about outright, elaborate scams. It can be much more subtle. For instance, a driver might try to claim for a problem they knew about for weeks, acting as if it just happened. Or maybe someone exaggerates how serious their situation is just to snag a more expensive service, like onward travel, when it’s not really needed. These might feel like small fudges but they pump huge, unnecessary costs into the system.

The Investigation And The Cost To Us All

Naturally, breakdown cover providers have to take this seriously. Most have dedicated teams whose entire job is to investigate suspicious claims. They’ll look for holes in a driver’s story or hunt for evidence that a fault was a pre-existing condition long before the call for help came in. The problem is, proving fraud is incredibly difficult and drains time and resources.

Every investigation costs money. Every fraudulent claim that slips through and gets paid out adds to an insurer’s losses. At the end of the day, these companies are businesses and to stay afloat, they have to make up for those losses somewhere. They do this by spreading that financial hit across their entire customer base.

In short, the cash paid out on dodgy claims is clawed back through the premiums of honest policyholders. It’s that simple: fraud makes essential cover more expensive for every single one of us.

This collective hit is massive. While it's tricky to get exact numbers for breakdown cover alone, the wider insurance industry is fighting a huge battle. You can learn more about how insurance fraud costs the industry to see the truly staggering scale of the problem. Every false claim, big or small, adds to that eye-watering figure.

How Fraud Harms Everyone

Ultimately, insurance fraud is far from a victimless crime. It fuels a cycle of mistrust, drives up operational costs for providers and those costs are passed directly onto you, the customer.

Here’s a quick rundown of the damage:

- Higher Premiums: Insurers set their prices based on risk and claim data. When fraud inflates the number and cost of claims, the risk level for everyone goes up, leading to higher annual prices for all of us.

- Stricter Claim Processes: To fight back against fraud, providers often have to bring in more rigorous checks. This might mean demanding more evidence or asking more questions, which can slow down genuine claims and create a headache for honest customers who are in real trouble.

- Reduced Trust: Widespread fraud chips away at the trust between insurers and their customers. That relationship is the bedrock of the entire insurance model and when it’s damaged, the whole system suffers.

It means that the next time you get your renewal quote, the price you’re being asked to pay is partly shaped by the dishonest actions of a few. Understanding that connection makes it crystal clear that tackling fraud is in everyone’s best interest. It helps keep car breakdown cover fair, efficient and affordable for the honest majority who depend on it.

Choosing A Breakdown Policy That Works For You

Picking the right car breakdown cover UK policy isn't about grabbing the cheapest deal you can find. It’s about matching the level of protection to your actual, real-world driving habits. A policy that’s perfect for a local commuter could leave someone who travels the length of the country for work completely stranded.

The first step is to have an honest look at your own needs. Think about how you really use your car. Do you rely on it every single day for work or the school run or is it more for the odd weekend trip? Answering this simple question will tell you whether you can afford any downtime. If your car is absolutely vital, a basic policy might not cut it.

Evaluating Your Driving Profile

Your typical journeys are a massive factor. Do you spend most of your time on familiar local roads or are you frequently cruising down motorways for hours on end? A driver who sticks to their hometown has very different needs from a sales rep covering a national territory.

To find your ideal fit, ask yourself a few key questions:

- How far do you drive? If you often find yourself hundreds of miles from home, Nationwide Recovery is pretty much non-negotiable.

- How reliable is your car? An older vehicle with a less-than-perfect service history is a prime candidate for a more comprehensive policy. That should definitely include Home Start for those cold mornings when it just won't turn over.

- Who else drives the car? A vehicle-specific policy can be cheaper if it's just one car that needs covering. But if you often drive multiple cars or find yourself as a passenger in others, personal cover is the way to go.

- What’s the real impact of a breakdown? If a delay would completely ruin a family holiday or cause serious problems at work, paying a little extra for Onward Travel could be a very wise investment indeed.

Digging Deeper Than The Headline Price

Once you’ve got a clear picture of what you need, you can start comparing providers. It’s so tempting to just grab the cheapest quote but this is often a false economy. The true value of breakdown cover is only revealed when you actually need to use it. That’s when a provider's reputation and service level really show their worth.

Before you commit, it’s critical to look past the flashy marketing and read the small print. This is where you’ll find the important details that can make or break your experience during a stressful roadside incident.

Be sure to check for specific exclusions and limitations. Many policies will have a cap on the number of call-outs you can make in a year or strict limits on towing distances for their basic cover.

Finally, check independent customer reviews and dig into provider response times. A low price means nothing if you’re left waiting by the side of a dark road for hours on end. Choosing a reputable provider with a proven track record of fast, efficient service is what provides the genuine peace of mind you're paying for. This careful approach ensures you find a policy that offers real value and reliable support right when you need it most.

What To Do When Your Car Breaks Down

Your first move depends entirely on where you are. A busy motorway calls for a very different response than a quiet country lane.

If you have enough momentum, try to guide your car to a safe spot. On a motorway, that means getting onto the hard shoulder, as far to the left as possible. Once there, turn your wheels away from the traffic. On other roads, hunt for a lay-by or a clear area well away from blind bends or the crest of a hill.

As soon as you’ve stopped, get your hazard warning lights on. It’s the universal signal that you’re in trouble and instantly makes your vehicle more visible to other drivers.

Staying Safe While You Wait

Your safety and that of any passengers is the number one priority. If you’ve broken down on a motorway or a fast A-road, everyone needs to get out of the vehicle on the left-hand side, away from the flow of traffic. Find a safe spot on the verge, ideally well behind a safety barrier if there is one.

Whatever you do, don't wait inside your car in this situation. It’s also best to leave pets inside the vehicle unless they're in immediate danger; a scared animal could bolt into traffic.

It’s no surprise that the colder months see a spike in these incidents. In the UK, winter brings over 1.2 million breakdowns to our roads between November and January alone. That works out to more than nine every single minute. The most common culprit? Flat batteries, which hate the cold.

Contacting Your Breakdown Provider

Once everyone is safely out of harm’s way, it’s time to call for help. Have your policy number handy, though most providers can find your details using your car’s registration and your postcode.

To get a patrol out to you as quickly as possible, you’ll need to give them some clear information:

- Your exact location: Use your phone’s map app, look for the small marker posts on the side of the motorway or recall the last junction you passed.

- Your vehicle details: The make, model and registration number of your car.

- A description of the problem: Tell them what happened as best you can. Did you hear a noise? Did a specific warning light come on?

When you break down, you're immediately thinking about getting the car moved and figuring out how you'll get home. Knowing about services like towing and rental car assistance can be a huge relief.

Giving your provider clear details isn't just about getting a faster response; it's a crucial part of making a successful claim. Unclear or inaccurate information can sometimes cause issues and it's always useful to understand why an insurance company might refuse to pay a claim. The more info you can provide, the smoother the whole process will be.

Common Questions About Breakdown Cover

Even when you think you’ve settled on the right car breakdown cover UK , a few last-minute questions often pop up. Getting clear answers to these common queries can give you the confidence to sign up, knowing you’ve absolutely picked the right policy for your needs.

One of the first things people ask is about switching providers. You are completely free to move to a new breakdown company when your policy is up for renewal. In fact, it’s a great way to find a better deal. Insurers rarely reward loyalty, so shopping around is almost always worth your time.

What If I Have The Wrong Cover?

Another big worry is what happens if you break down but don’t have the right level of cover for that specific situation. For instance, what if you have a basic roadside assistance plan but need to be towed home from the other side of the country?

In that scenario, the provider will still come out to you but you’ll likely have to pay extra for any services not included in your policy. That can get very expensive, very quickly and it really highlights the importance of choosing a cover level that genuinely matches your driving habits from day one.

It’s crucial to be honest with yourself about how you use your car. Trying to save a few quid on a basic policy can lead to a much bigger bill if you end up needing a service like nationwide recovery that you opted out of.

Can I Call Out For The Same Fault?

This is a key point that every driver needs to understand. Let's say a patrol gives you a temporary fix and tells you to get the car to a garage for a proper repair. If you do not do that and then break down again with the exact same fault, your provider may refuse to attend a second time.

Breakdown cover is designed for unforeseen emergencies, not for recurring issues you already know about. You have a responsibility to keep your vehicle properly maintained.

For more detailed answers to specific queries, you can find a lot of helpful information by reading through these frequently asked questions about insurance.

At Proova , we believe in making insurance processes clear and fair. Our platform helps verify item ownership quickly and securely, making genuine claims faster and protecting the system from fraud that drives up costs for everyone. Find out more at https://www.proova.com.