A Guide to Your Business Risk Management Framework

A business risk management framework is not some rigid document you file away. Think of it as the architectural blueprint for your company’s resilience—a structured, continuous process for spotting, assessing and controlling threats to your capital and earnings. It is the system you rely on to protect assets, ensure you can keep the lights on and make sharp decisions in a wildly unpredictable world.

Understanding the Blueprint for Business Resilience

Imagine you are putting up a large office building in an area known for its chaotic weather. You would not just start laying bricks and cross your fingers, would you? Of course not. You would work from a detailed architectural blueprint that accounts for every potential stress, from high winds and heavy rain to ground shifts. That plan dictates the materials, foundation depth and structural supports needed to keep the building standing, no matter what the weather throws at it.

A business risk management framework does the exact same job for your organisation.

It is what moves your company from a reactive stance—scrambling to put out fires as they erupt—to a proactive one. You start anticipating threats and managing them before they can cause any real harm. This is not about trying to eliminate risk entirely, because that is impossible. It is about understanding the risks you face and making deliberate, conscious decisions about which ones are worth taking.

The True Cost of Unmanaged Risk

When risks are left to fester, the consequences ripple out far beyond a single balance sheet.

Take the insurance industry, a sector literally built on managing risk. When fraudulent claims slip through the net because of weak verification processes, the insurer is not the only one who pays. It is estimated that insurance fraud adds an extra £50 to the average UK household's annual insurance bill . This makes a crucial point crystal clear: unmanaged risk has a ripple effect that costs everyone.

Those costs are passed on to every policyholder through higher premiums. For businesses, that means higher operational expenses, making them less competitive and taking a tangible bite out of the bottom line. The ability to prove the legitimacy and value of a claim is central to a fair system for everyone. Without a structured, verifiable way to document what was lost and its condition, both genuine claimants and insurers suffer, and the industry's integrity is eroded.

A robust framework provides the necessary structure to validate claims accurately, deter fraudulent activities and ultimately control the costs that affect us all. It is the mechanism that ensures fairness and stability in the face of uncertainty.

Aligning Strategy with Risk Appetite

Ultimately, a risk management framework is a powerful strategic tool. It forces an organisation to sit down and define its risk appetite —in other words, the level of risk it is willing to accept to achieve its goals.

Getting this strategic alignment right is critical for sustainable growth. By creating a durable structure for identifying and dealing with threats, your organisation can navigate the UK's dynamic economic landscape with far greater confidence and purpose, ensuring every decision you make supports your long-term vision.

The Core Components of an Effective Framework

To turn a business risk management framework from a dusty document into a practical, everyday tool, you first need to understand its foundational pillars. Think of them not as separate steps but as interconnected gears in a machine, working together in a continuous cycle of identification, assessment and response. Each part has a distinct role but they all contribute to the same goal: building a more resilient organisation.

This structure is not just an internal box-ticking exercise. It provides the proof you need to satisfy regulators, partners and insurers that your business is managing its obligations responsibly. In sectors like insurance, where the cost of fraud gets passed on to all policyholders, a robust framework is the first line of defence against illegitimate claims that drive up costs for everyone. The provability of a claim is paramount.

At its heart, any effective framework can be broken down into five distinct but interconnected components. Getting to grips with each one is the first step towards building a system that actively protects your business.

Risk Identification And Assessment

The journey starts with Risk Identification . This is the forward-looking part of the process, where your team gets together to brainstorm everything that could go wrong. We are talking about everything from a key supplier going bust to a sudden data breach. Without this crucial first step, you are essentially flying blind.

Once you have identified a potential risk, it is time for Risk Assessment . Here, you weigh up two key factors for each threat: how likely is it to happen and what would the fallout be if it did? This stage is all about prioritisation, making sure you focus your energy and resources on the biggest threats, not the minor niggles.

Mitigation, Monitoring, And Communication

After assessing the risks, the next logical step is Risk Mitigation and Control . This is where you decide how to respond. Your options usually fall into one of four categories:

- Avoiding the risk by stopping the activity that causes it altogether.

- Accepting the risk, which often makes sense when the cost of fixing it is far greater than the potential impact.

- Reducing the risk by putting new controls and procedures in place.

- Transferring the risk, most commonly by taking out an insurance policy to cover potential losses.

A framework is not a static document you create once and forget about. The Monitoring and Review component ensures it remains a living, breathing process. It involves keeping a close eye on identified risks, checking if your control measures are actually working and adapting the whole framework as new challenges emerge.

Finally, Communication and Reporting ties everything together. This pillar ensures that information about risks, control measures and responsibilities is shared clearly with everyone who needs to know, from the board of directors right down to frontline employees. When reporting is clear, everyone understands their role in managing risk.

Many well-known models are built on these exact principles. The COSO Enterprise Risk Management (ERM) Framework, for instance, organises these ideas into five key components, including governance and strategy-setting. It is a popular choice for large UK public companies because it elevates risk management from a simple compliance task to a strategic function that helps drive the business forward. You can discover more insights about this approach and other risk management framework examples.

An effective framework is more than just a list of potential problems. It is a dynamic system for making informed decisions, protecting assets and ensuring that when a claim is made, its legitimacy can be proven swiftly and accurately.

The table below breaks down how these components work in a real-world scenario, giving you a clear view of their practical application.

Core Components of a Risk Management Framework

| Component | Objective | Practical Example (UK Manufacturing Firm) |

|---|---|---|

| Risk Identification | To proactively uncover potential internal and external threats to business objectives. | The firm holds workshops and identifies a key risk: a single-source supplier for a critical component is based in a geopolitically unstable region. |

| Risk Assessment | To analyse the likelihood and potential impact of identified risks to prioritise them effectively. | The risk is assessed as high likelihood due to recent political tensions and severe impact due to potential production halts costing millions. |

| Risk Mitigation | To develop and implement strategies to control, avoid, accept, or transfer prioritised risks. | The firm initiates a project to qualify a second supplier in a different country and increases its buffer stock of the critical component by 30% . |

| Monitoring & Review | To continuously track risks and the effectiveness of mitigation strategies, adjusting as needed. | The procurement team provides quarterly reports on the new supplier's progress and monitors geopolitical news related to the primary supplier. |

| Communication | To ensure all stakeholders are informed about risks and their respective responsibilities. | The risk and mitigation plan are logged in a central register, reviewed by the board, and communicated to the production and finance departments. |

By seeing how each pillar functions in practice, it becomes easier to visualise how a structured framework can move from theory to tangible business protection.

How to Identify and Categorise Business Risks

Effective risk management is not about gazing into a crystal ball; it is about taking a clear-eyed look at the real threats your business faces. Before you can manage risk, you have to see it first. This means systematically exploring your potential weaknesses and the pressures pushing in from the outside.

Think of it like a ship's captain studying the weather charts before a long voyage. They are not hoping for a storm but they are preparing for the possibility. The goal is to build a complete inventory of potential problems, not to create fear but to build awareness.

Starting the Identification Process

The best way to spot risks is to get different perspectives. Bring people together from all corners of the business—finance, operations, marketing, IT, you name it. A threat that is invisible to one department might be glaringly obvious to another.

A few proven methods to get the conversation started include:

- Brainstorming sessions: Get teams in a room to openly discuss "what if" scenarios without judgment. This is where you uncover the unexpected.

- SWOT analysis: A classic for a reason. Looking at your Strengths, Weaknesses, Opportunities, and Threats helps pinpoint internal vulnerabilities and external pressures.

- Digging into historical data: Your own past is a great teacher. Review old incident reports, audit findings, or insurance claims to see what issues keep cropping up.

And remember, this is not a one-and-done exercise. The world changes and new risks appear all the time. You need to revisit this process regularly to keep your risk framework relevant.

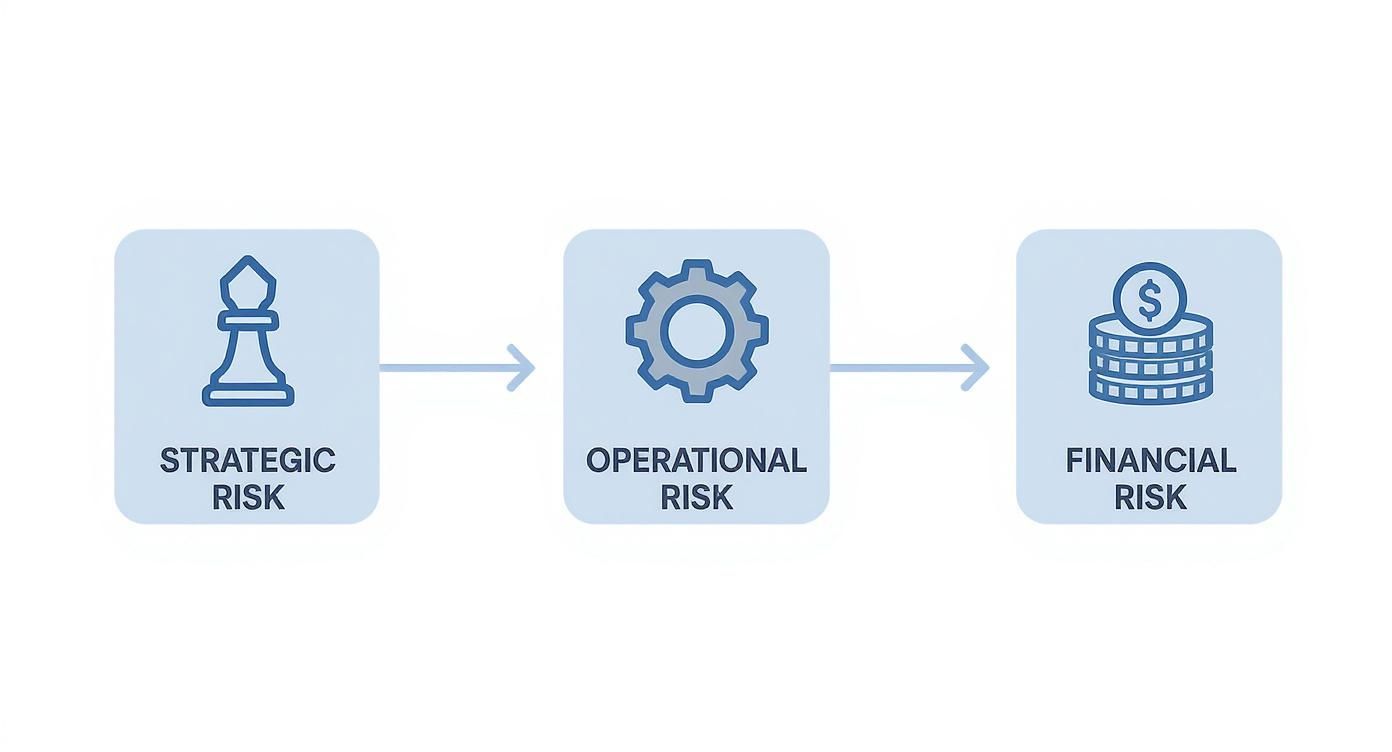

The Main Categories of Business Risk

Once you have a long list of potential risks, it is time to bring some order to the chaos. Grouping them into categories makes them far easier to analyse, prioritise and assign to someone to manage. While every business is unique, most risks fall into four main buckets.

-

Strategic Risks

These are the big-picture threats tied to your core business goals. Think about a competitor launching a game-changing new product, a sudden shift in what your customers want, or your reputation taking a nosedive after a social media disaster. -

Operational Risks

This is all about the day-to-day running of your business. Operational risks stem from failures in your processes, people, and systems. Examples include equipment breaking down on a production line, an employee making a mistake that leads to a data breach, or fraud creeping into your supply chain. These external factors, like supply chain vulnerabilities, demand their own focused strategies for successfully mastering supply chain risk assessment. -

Financial Risks

This category covers anything that threatens the financial health of your organisation. It includes things like credit risk (customers not paying their bills), liquidity risk (running out of cash to pay your own obligations), and market risk from swings in interest rates or currency values. The damage can escalate quickly, especially when fraud is involved. You can read more about this in our article on the global fraud epidemic. -

Compliance Risks

These risks pop up when you fail to follow the rules—be they laws, regulations, or industry standards. For UK businesses, this could mean falling foul of GDPR, health and safety regulations, or financial reporting standards, all of which can lead to eye-watering fines and legal trouble.

By sorting risks into these categories, you start to see patterns. You realise how a single event can cascade through the business—a supply chain failure (operational) can quickly become a financial problem and, if left unchecked, a major strategic threat.

The modern business world is a minefield of economic instability and digital threats. A 2024 survey of over 2,000 UK business leaders highlighted financial uncertainty, cybercrime and the struggle to attract and keep good people as today's most pressing risks.

This shows how quickly risk profiles can change. Persistent inflation and a tight labour market are forcing businesses to confront a much wider range of threats than before, from climate change to geopolitical instability. It is a stark reminder that identifying risk has to be a dynamic, ongoing conversation.

Implementing Your Risk Management Framework Step by Step

Alright, let us move from theory to action. Building a practical business risk management framework is not something you can knock out over a weekend. It is a structured, methodical process that requires buy-in from across the business, weaving risk awareness into the very fabric of your company culture.

Think of it less as a project for a single department and more as a collaborative effort. This guide will give you a clear roadmap to get from concept to concrete results.

First things first: you absolutely must get the leadership team on board. Without genuine sponsorship from the top, any risk management initiative is doomed to become a tick-box exercise, filed away and forgotten. Senior management cannot just approve the framework; they need to actively champion a culture where talking about and managing risk is normal.

This commitment from the top sets the tone for the entire organisation. It is a clear signal that managing risk is a shared responsibility and a core part of being successful, not just another headache for the compliance team.

Defining Your Scope and Objectives

With leadership backing you, the next job is to clearly define the scope of your framework. Are you going enterprise-wide from day one or will you start with a specific, high-risk division? It is also vital to align the framework’s objectives with your overall business strategy, making sure it supports your goals rather than getting in the way.

Imagine you are drawing the borders on a map. You need to know exactly what territory your framework will cover and what you hope to achieve within those boundaries. This clarity stops the project from spiralling out of control and keeps your efforts focused where they will have the biggest impact.

A cross-functional team is your secret weapon here. Pull together people from finance, operations, IT, legal and HR. This ensures you capture a wide range of perspectives and avoids the siloed thinking that so often lets major risks slip through the cracks between departments.

Conducting the Initial Risk Assessment

Once your team is assembled, the real work begins with an initial risk assessment. This is where you roll up your sleeves and identify potential threats right across the business—from strategic blunders and operational hiccups to financial shocks. This deep dive gives you the raw data you need to build the rest of your framework.

This infographic breaks down the key categories to think about during your risk identification process.

Visualising risks this way helps make sure you are covering all the important angles of the business.

After identifying the risks, you need to analyse each one for its potential impact and how likely it is to happen. A simple matrix scoring system is a great tool for this, helping you prioritise which threats need your attention right away. This analytical step ensures your resources are aimed at your most significant vulnerabilities first.

Everything you find is then logged in a risk register . This document is the heart of your framework. It is a central list of every risk you have identified, its potential impact, who is responsible for managing it and the plan to deal with it. Crucially, this is a living document that needs to be updated regularly.

Implementing Controls and Mitigation Plans

This is where your strategy becomes action. For each significant risk, you will need to decide on a response:

- Avoid: Stop the activity that creates the risk.

- Reduce: Put controls in place to lower the likelihood or impact.

- Transfer: Shift the financial fallout, usually by taking out insurance.

- Accept: Formally acknowledge the risk but take no further action, typically for low-impact threats.

Putting these controls into practice is a critical step. In the insurance world, for instance, proving that an item existed and was in a certain condition before a loss is a powerful control against fraudulent claims. Verifiable proof cuts through the ambiguity that fraudsters love to exploit, which ultimately helps keep premium costs down for everyone.

A business risk management framework is not a one-time project but a continuous cycle. Establishing a regular schedule for monitoring risks, reviewing the effectiveness of your controls and reporting findings to leadership is essential for its long-term success.

This final step closes the loop, making sure your framework stays relevant and can adapt to new threats and changing business conditions. It transforms risk management into an ongoing, dynamic process that builds lasting resilience and protects against the financial drain of unverified claims that plague the entire industry.

The Critical Role of Governance and the Board

A business risk management framework is only as good as the culture supporting it. You can have the most detailed plan in the world for spotting and handling threats but without genuine commitment from the very top, it is just a paper exercise.

Real resilience is built when managing risk becomes part of the company’s DNA. And that always starts with the board.

It is the board of directors that sets the 'tone at the top'. This is not just a nice-to-have; it is a fundamental requirement for any risk framework to succeed. When they get behind it, it sends a clear message to everyone that managing risk is a core strategic priority, not just a box-ticking afterthought.

This top-down approach is essential. When leadership actively champions risk management, it creates a culture of transparency where employees feel safe enough to raise concerns. Without that sponsorship, even the most carefully designed framework will struggle to gain traction and will have zero real impact on business resilience.

Board Responsibilities in Risk Governance

The board’s role goes far beyond simple oversight. They are directly responsible for several key functions that give the risk framework its authority and its teeth.

Key responsibilities include:

- Defining Risk Appetite: The board must clearly state the level and type of risk the organisation is willing to take on to meet its goals. This creates the essential guardrails for the management team.

- Integrating Risk into Strategy: Directors have to make sure risk is a central part of every major strategic decision, from entering new markets to developing new products. This stops risk from being managed in a silo, detached from the core business.

- Ensuring Adequate Resources: The board is also on the hook for allocating the necessary budget, technology and people to make the risk management function work effectively.

This level of hands-on involvement is crucial for building trust in the insurance industry . A strong governance structure is a powerful signal that a firm is serious about managing risks like fraud, which ultimately drives up costs for every policyholder.

The Governance Gap in UK Businesses

Despite how important it is, the maturity of risk governance varies wildly across UK businesses. Board-level engagement often comes down to company size and how immediate the threats feel. Cyber security, for instance, remains a top risk but the board's attention to it is patchy at best.

According to the UK's 2024 Cyber Security Breaches Survey, 63% of large businesses have board members specifically responsible for cyber security. That number drops to just 27% for micro businesses.

The gap is just as stark between sectors. Information and communications firms lead the way at 60% , while industries like construction and hospitality are lagging far behind. It just goes to show the ongoing challenge of embedding a universal, risk-aware culture from the top down.

Ultimately, the board acts as the framework's chief advocate. When directors are actively involved, risk management is transformed from a defensive measure into a strategic tool that protects value and enables sustainable growth.

Of course, here is the rewritten section, crafted to sound like it was written by an experienced human expert, following your specific style and formatting requirements.

Still Have Questions About Risk Management Frameworks?

Even when you understand the theory, putting a business risk management framework into practice can feel a bit daunting. It is only natural for questions to pop up when you start applying these ideas to the real world.

Let us tackle some of the most common ones I hear from business leaders. Getting these cleared up can help bridge that gap between the textbook and the day-to-day reality of running a business.

“Isn’t This Just for Big Corporations?”

This is probably the number one question I get asked and the simple answer is no. Risk does not care about the size of your company and neither should your approach to managing it.

The core principles—spotting risks, figuring out how serious they are and deciding what to do about them—are universal. A small local business might track everything on a straightforward spreadsheet, while a global firm will need dedicated software. The tool changes but the discipline is exactly the same.

“Is This All Just a Box-Ticking Exercise for Compliance?”

It is easy to see why people think this. But viewing a risk framework as just another compliance chore is a huge missed opportunity. Yes, it absolutely helps you meet regulatory demands but its real power is strategic.

A well-built framework is a source of vital business intelligence. It informs smarter decisions, protects your hard-earned reputation and can even shine a light on new opportunities. It should be a living, breathing part of your strategy, not a dusty document you pull out once a year for the auditors.

This is especially true when it comes to insurance. If you cannot prove what you owned and what condition it was in, making a legitimate claim can turn into a long, frustrating battle.

This is where a lack of verifiable proof really stings. It creates a perfect environment for insurance fraud to flourish. And those costs are not just absorbed by the insurers—they get passed straight on to every policyholder through higher premiums, hitting businesses and households right across the UK.

“What’s the Difference Between Risk Management and Crisis Management?”

This is another common point of confusion. The easiest way to think about it is timing.

Risk management is proactive. It is the ongoing work you do to look ahead, anticipate problems and stop them from ever happening. It is about building strong fences at the top of the cliff.

Crisis management , on the other hand, is reactive. It is the plan you kick into gear after something has already gone wrong. It is the ambulance waiting at the bottom of the cliff.

A truly effective business risk management framework means you will spend a lot less time calling that ambulance.

Take the guesswork out of your claims process. With Proova , you can create a verifiable, time-stamped record of your assets, providing the concrete proof needed to combat fraud and streamline legitimate claims. Protect your business and help lower costs for everyone by visiting https://www.proova.com to learn more.