An Insurer's Guide to Mitigating Laptop Insurance Fraud & Costs

Laptop insurance, whether standalone or part of a contents policy, has become a high-volume, low-margin product that presents a significant commercial risk. The rapid growth in gadget cover has created a fertile ground for opportunistic fraud and costly claims disputes. For insurers, every policy written without upfront verification of the asset is a latent liability, primed to inflate claims costs and erode profitability.

The Quantified Problem with Laptop Insurance Claims

The UK gadget insurance market is expanding rapidly, but this growth masks a serious threat to insurers' bottom lines. As policy volumes rise, so does exposure to after-the-event fraud and inefficient claims processing, driving up operational costs and claims leakage.

According to industry data, gadget insurance policies in the UK increased from 7.87 million in 2023 to 8.46 million in 2024 —a 7.5% rise in a single year. Consequently, gross written premium grew by 22% , from £496 million to £604 million, driven by the increasing value of essential devices like laptops. However, this growth brings with it two core challenges that directly impact profitability.

The Twin Challenges Draining Profitability

From a claims director's perspective, this market expansion introduces two significant problems that inflate operational costs and fuel claims leakage.

-

Fraudulent Claims for Pre-Existing Damage: A policyholder damages their uninsured laptop, takes out a new policy, and files a claim after the exclusion period. Without verifiable proof of the laptop's condition at inception, refuting the claim is often commercially unviable. The cost to investigate often exceeds the claim value. Detected insurance fraud costs the industry £1.1 billion annually, but much of this low-value fraud goes undetected. You can learn more about the https://www.proova.com/the-true-cost-of-insurance-fraud-in-the-uk in our detailed guide.

-

Administrative Burdens of Post-Loss Verification: For legitimate claims, the process of verifying ownership and condition after a loss is a major operational drain. Handlers spend weeks chasing receipts, confirming serial numbers, and disputing valuations. This reactive model turns every undocumented laptop into a source of friction, delay, and spiralling overheads.

Understanding these failure points is key. For instance, a simple guide on how to replace laptop battery on HP models shows just one of many repair costs that often trigger a claim. Without evidence from before the policy went live, verifying what actually caused the damage becomes a costly and adversarial slog. Every unverified device on the books is a ticking clock, just waiting to become a dispute.

To put it into perspective, here's how these challenges directly hit an insurer's bottom line.

Financial Impact of Inefficient Laptop Claims Processing

This table breaks down the key financial drains insurers face when processing laptop claims without upfront verification, illustrating the cost of inaction.

| Challenge Area | Traditional Process Failure | Direct Cost to Insurer |

|---|---|---|

| Fraudulent Claims | Inability to disprove pre-existing damage due to lack of inception evidence. | Direct payout for fraudulent claims, impacting loss ratios and driving up premiums. |

| Claims Leakage | Overpayment on devices due to inflated valuations and lack of serial number proof. | Unnecessary payouts for higher-spec models, eroding underwriting profit. |

| Operational Drag | Claims handlers spend weeks chasing receipts and verifying ownership after a loss. | Increased staff costs, longer claim lifecycles, and a higher cost-per-claim. |

| Customer Friction | Adversarial process creates disputes, complaints, and reputational damage. | Loss of customer loyalty, negative reviews, and potential regulatory scrutiny. |

Ultimately, these interconnected issues create a cycle of financial loss and operational inefficiency. The only way to break it is by tackling the root cause: the evidence gap at the start of the policy.

Why Current Approaches Fail: The Flaw in Post-Claim Verification

The traditional ‘detect at claim’ model for handling laptop insurance is fundamentally broken. It is a reactive process that creates friction, invites fraud, and inflates operational costs. This approach places the burden of proof on the policyholder at the most stressful moment—immediately following a loss.

Consider our classic "lounge exercise." Ask a policyholder to list their lounge contents, and they will tell you it is easy. Ask them to do it from memory after a burglary, complete with serial numbers and proof of purchase, and the process can descend into a six-week dispute. That same principle applies with brutal efficiency to laptops.

The Problem with Proof After the Fact

Expecting a customer to produce a receipt or serial number for a laptop purchased two years ago is unrealistic. This adversarial scramble for documentation is a direct cause of protracted claims cycles, which in turn damages customer satisfaction and increases churn.

This reactive verification process fails insurers in several critical ways:

- It fuels opportunistic fraud: Without baseline evidence of the laptop's existence and condition at inception, it is nearly impossible to disprove a claim for a high-spec model that never existed or one that was damaged before the policy was active.

- It necessitates costly interventions: When basic evidence is missing, the next step is often deploying a loss adjuster. This adds a significant, often disproportionate, expense to a relatively low-value electronics claim, directly hitting the claims expense ratio.

- It creates administrative drag: Claims handlers waste valuable time chasing paperwork and debating valuations—time that could be spent on more complex cases.

An Unreliable Foundation for Claims

A huge factor in why post-claim verification fails is the lack of robust IT Asset Management from the policyholder's side, which is essential for accurate tracking. When the insurer has no verified record to work from, every claim starts from a position of ambiguity and potential dispute.

The core issue is that post-claim verification tries to solve a problem at the end of the process that should have been prevented at the beginning. It's like trying to confirm a building's foundations after it has already collapsed.

This approach not only fails to stop fraud but actively creates an environment where it can flourish. By shifting verification to the policy's inception, insurers can move from a costly, detective model to an efficient, preventative one. You can learn more about how real-time evidence changes everything in our detailed analysis. The entire claims lifecycle is simplified, reducing costs and improving the customer experience all at once.

The Cost of Inaction: Quantifying the Financial Drain

Sticking with the status quo on laptop claims is not merely inefficient; it is a significant financial leak. Tolerating after-the-fact proof of ownership directly impacts profitability through claims leakage, inflated operational costs, and damaged customer relationships. The cost of inaction becomes impossible to ignore when these impacts are quantified.

The UK's electronic gadgets insurance market is set to grow at over 10% CAGR through 2033 , a surge powered largely by laptops. With accidental damage making up a colossal 78.57% of the market , the financial exposure from unverified policies is climbing fast. You can explore more data on the UK electronic gadgets insurance market on datainsightsmarket.com to get a sense of the scale. Every new policy written without upfront proof is just another potential hole in the bucket.

Claims Leakage from Unverified Laptops

The most immediate cost is paying out on claims that are either fraudulent or inflated. Without a time-stamped record of a laptop's existence, model, and condition at policy inception, an insurer is at a disadvantage from the outset.

Was the laptop already damaged before the policy went live? Was it a basic model now being claimed as a top-of-the-range machine? Attempting to disprove these claims after a loss is a costly and often futile exercise. The path of least resistance is frequently to pay the claim, leading to a steady, preventable leakage that erodes underwriting profit.

The real cost isn't just one fraudulent claim. It’s the systemic acceptance of ambiguity across the entire book of business. This normalises overpayment and turns the claims process into a game of chance, not a function of evidence.

Swollen Operational Costs

Beyond direct payouts, the operational waste is staggering. Consider the hours your experienced claims handlers spend on low-value, high-friction laptop claims.

- Chasing Paperwork: Countless hours are burned trying to track down receipts, photos, and serial numbers that the policyholder may no longer possess.

- Arguing Over Value: Time spent debating valuations and pre-loss condition could be applied to complex, higher-value claims where expertise is crucial.

- Deploying Loss Adjusters: Appointing a loss adjuster to verify a £1,500 laptop claim is a disproportionate expense that eliminates any potential profit on that policy.

These administrative burdens create a slow, expensive claims cycle and divert skilled personnel to tasks that could be eliminated through upfront verification.

The Long-Term Price of a Bad Claims Experience

Finally, there is the long-term cost of a difficult claims process: customer churn. An adversarial, protracted experience over a lost or damaged laptop leaves a lasting negative impression.

This does not just mean losing one policyholder. It fuels negative reviews and damages brand reputation. In a competitive market, brokers and insurers cannot afford a reputation for creating friction at the moment of truth. The cost of acquiring a new customer is always far higher than the cost of retaining one through a smooth, efficient claims journey.

How Verification at Inception Solves This

The traditional, reactive model for insuring laptops accepts fraud and disputes as a cost of doing business. The solution is to mandate proof before the policy incepts, thereby eliminating the root causes of these costs. This involves requiring the policyholder to create a simple, undeniable digital record of their laptop—a geocoded, time-stamped file with clear photos of the device, its serial number, and its physical condition.

Embedding this verification step into the onboarding process fundamentally changes the claims dynamic. A claim transforms from a contentious investigation into a straightforward administrative check.

Eradicating Common Fraud Vectors

This pre-emptive approach directly neutralises the most common and costly types of laptop insurance fraud.

-

'After-the-Event' Fraud Prevention: The common scenario where an individual damages their laptop and then purchases insurance becomes impossible. The time-stamped record proves the item’s condition at inception, allowing any claim for pre-existing damage to be rejected with confidence.

-

Valuation and Model Disputes: Disagreements over whether a lost device was a basic model or a high-specification machine are eliminated. The verified record, complete with a serial number, establishes an agreed-upon reality from day one, preventing inflated claims.

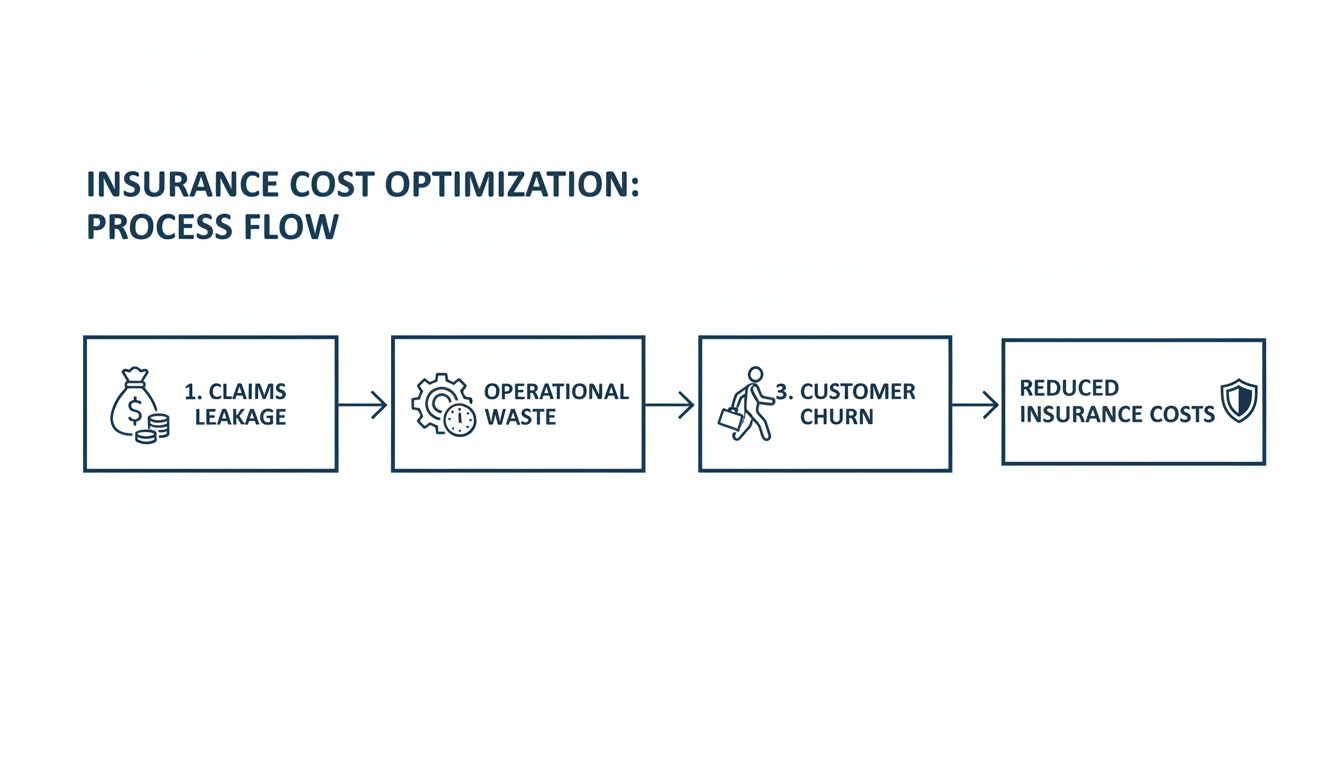

The infographic below illustrates how this proactive verification method enables insurers to reduce unnecessary costs.

As you can see, verifying assets at inception is a direct line to reducing claims leakage, cutting operational waste, and stopping the customer churn that comes from frustrating claims experiences.

From Ambiguity to Certainty

With a pre-verified inventory, the claims process becomes remarkably simple. When a policyholder reports a theft or damage, the claims handler does not need to launch an investigation to prove the laptop's existence or value; they simply consult the inception report.

The core value is this: You stop paying to solve problems that shouldn't exist in the first place. Instead of spending weeks chasing receipts and arguing over condition, the evidence is already on file, waiting to be confirmed.

This shift does not just reduce fraud; it has a profound impact on operational efficiency. It eliminates the need for most loss adjuster visits for laptop claims, frees up experienced handlers to focus on more complex cases, and drastically shortens the claim lifecycle. To get a better sense of the wider financial benefits, you can learn more about how pre-authentication can reduce claims costs by up to 30 percent.

Ultimately, pre-inception verification provides the evidential certainty needed to process claims quickly, fairly, and with minimal friction. It protects insurers from fraud while delivering the fast, transparent service that modern policyholders expect.

The Commercial Outcome: Driving Efficiency and Reducing Costs

Implementing pre-inception verification for laptop insurance is not just a fraud prevention tactic; it is a strategic redesign of the claims process to deliver tangible commercial results. The primary benefit is a significant acceleration of the claims lifecycle, which directly cuts operational costs, optimises resource allocation, and provides a competitive advantage for insurers and brokers.

A claim that once involved a six-week dispute over receipts and valuations can now be settled in days. When proof is on file from inception, the process shifts from investigation to simple confirmation.

Measurable Reductions in Claims Handling Costs

The time saved on each claim directly impacts the bottom line. With a pre-verified digital record, claims handlers are no longer consumed by low-value administrative tasks. This efficiency gain allows experienced teams to focus on complex, high-value cases where their expertise adds real value.

In 2024-2025, 68% of UK adults owned laptops , feeding a market where accidental damage claims command a 78.57% market share . With claims for theft and loss also rising, operational efficiency is critical. You can find more details on the UK electronic gadgets insurance market growth on mordorintelligence.com. By automating the evidence-gathering stage, insurers can achieve significant operational savings.

We see clients reduce their average claim handling time from 14 days down to just 3 . This is not a marginal improvement; it is a transformation of the claims function that frees up thousands of man-hours per year.

A Differentiator for Brokers

For brokers, offering a tool that guarantees a smoother claims process is a powerful differentiator in a crowded market. It shifts the conversation from price to superior service and client protection. A fast, frictionless claims experience builds client loyalty and dramatically reduces post-claim complaints.

This approach benefits all parties. Insurers reduce operational costs and leakage, while brokers build stronger client relationships with a proven, value-added service. The table below highlights the stark contrast between the traditional method and a modern, Proova-enabled approach.

Before vs After Implementing Pre-Inception Verification

Here's a comparative look at the claims lifecycle for a typical laptop claim, highlighting the efficiency gains and cost reductions achieved with Proova.

| Claims Process Stage | Traditional Approach (Without Proova) | Proova-Enabled Approach (With Verification) |

|---|---|---|

| FNOL Evidence | Handler chases customer for receipts, serial numbers. | Handler accesses time-stamped, geocoded report instantly. |

| Verification Time | Days or weeks spent validating ownership and condition. | Minutes spent confirming details against inception record. |

| Loss Adjuster Need | Frequent call-outs for high-value or ambiguous claims. | Call-outs cut by up to 80% as evidence is pre-verified. |

| Settlement Speed | Average 14-21 days, often longer. | Average 1-3 days. |

| Customer Experience | Adversarial and stressful, leading to disputes. | Transparent and fast, reinforcing client trust. |

The contrast is clear. Moving verification to the start of the policy doesn't just prevent problems; it builds a faster, more efficient, and more trustworthy claims process from the ground up.

Answering Your Questions on Laptop Verification

Adopting a pre-inception verification process raises practical questions for claims directors, underwriters, and fraud teams. Here are answers to common queries, focusing on the operational and commercial outcomes of documenting laptops before a policy goes live.

Will Policyholders Actually Do This?

Yes, provided it is positioned correctly as a direct benefit to them: a guarantee of a faster, smoother claims process. A few minutes of effort upfront provides peace of mind and avoids the future stress of proving ownership after a loss.

This simple step transforms an abstract policy into a tangible, protected inventory of their assets. Our data shows high engagement when the value is clearly communicated at the point of sale. It ceases to be a requirement and becomes a guarantee of a swift, fair settlement.

How Does This Reduce Costs Beyond Fraud?

While fraud prevention is a key benefit, the most significant savings are operational. The primary advantage is the reduction in touchpoints required to process a claim.

With a complete, verified inventory available at First Notification of Loss (FNOL), efficiency increases immediately. You can:

- Slash handler follow-ups for receipts or serial numbers.

- Eliminate most desk-based validation checks that consume team resources.

- Reduce the budget for loss adjusters needed to confirm the existence of high-value electronics.

This operational efficiency directly lowers the claims handling expense ratio and allows experienced staff to focus on complex cases where their expertise is most valuable.

How Does Verification Integrate with Existing Systems?

Our platform is designed to integrate seamlessly into existing workflows via robust APIs that connect directly to your claims management or policy administration systems.

When a claim is filed, the verified, time-stamped report for the specific laptop is automatically pulled into your system. This provides the claims handler with all necessary evidence from the outset, eliminating manual data entry and ensuring data integrity from policy inception to claim settlement.

This isn't about adding another system for your team to juggle. It's about feeding better, cleaner data into the systems you already rely on, making them work harder for you from day one.

Is The Collected Evidence Strong Enough for Disputes?

Absolutely. Every item logged through the platform is supported by user-submitted photos that are time-stamped and geocoded upon upload. This creates an immutable digital record of the laptop's existence, condition, and location at a specific point in time— before a loss occurred.

This level of proof is significantly more robust than a policyholder's memory or an old receipt. It is designed to provide the clear, indisputable evidence required to meet validation standards, empowering your teams to reject fraudulent claims with confidence.

At Proova , we provide the tools to get rid of ambiguity and transform your claims process. By verifying assets right at the start, you can slash claims costs, shut down fraud, and deliver the fast, fair service your policyholders expect. Discover how our platform can deliver measurable commercial outcomes for your business.