A UK Insurer's Guide to 'Insurance for a Week' and Preventing Claims Leakage

The demand for short-term cover like insurance for a week has created a significant challenge for UK insurers. While offering flexibility to consumers for situations like house moves or temporary lets, these policies create a high-risk, low-information environment perfect for opportunistic fraud and costly claims disputes.

The core problem is simple: insuring unknown assets for a short period means the first time an insurer learns what they are covering is at the point of a claim. By then, it is too late to prevent fraud or verify the asset's pre-loss condition, leading directly to claims leakage.

The Quantified Problem: Hidden Risks in Temporary Cover

While offering flexibility for consumers, the explosion in short-term insurance has created a major headache for UK insurers. Policies that last for just a week introduce a level of risk traditional underwriting models were not built for. The come-and-go nature of this cover creates the perfect environment for opportunistic fraud and expensive, drawn-out disputes.

The Insurance Fraud Bureau (IFB) estimates that undetected general insurance fraud costs the industry £1.1 billion a year . A significant portion of this comes from low-value, high-volume opportunistic claims—exactly the type that flourishes in the temporary cover market. FCA data reinforces this, showing that home claims fraud involving undocumented items costs the industry £1.2bn annually , with a worrying 18% originating from short-term policies.

A New Avenue For Claims Leakage

The fleeting lifecycle of weekly insurance gives an insurer insufficient time to build a true picture of the risk. This creates vulnerabilities that directly impact profitability.

Here are the key weak spots insurers are wrestling with:

- 'After-the-Event' Fraud: It’s all too easy for a policyholder to insure items that are already damaged or don't exist, then file a claim a few days into the seven-day cover.

- Inflated Valuations: Without an upfront, verified inventory, it's incredibly difficult to challenge an exaggerated claim for lost or stolen goods, often leading to overpayments.

- Operational Strain: The high volume and low premium value of these policies mean that detailed, manual checks at the claims stage are not commercially viable.

The problem isn't unique to the UK; similar insurance challenges for short-term rentals are prevalent globally. The fundamental issue is always the same: a lack of verifiable information before the policy goes live.

Insurer Risk Profile: Weekly Versus Annual Policies

This table breaks down the heightened risks of weekly policies from an insurer's commercial perspective.

| Risk Factor | Traditional Annual Policy | Weekly Policy |

|---|---|---|

| Relationship Lifecycle | Long-term (12+ months), allowing for data collection and relationship building. | Very short-term (7 days), offering no time to establish a baseline of trust or behaviour. |

| Fraud Opportunity | Lower. Pre-existing damage is harder to hide over a longer period. | High. Perfect for 'after-the-event' fraud where already-damaged items are insured. |

| Asset Verification | More likely to involve upfront checks, especially for high-value items. | Almost non-existent. Assets are unknown until a claim is made, inviting disputes. |

| Underwriting Data | Rich data history from previous years allows for more accurate risk pricing. | Minimal to no data. Pricing is based on broad assumptions, not specific asset knowledge. |

| Claims Scrutiny | Higher-value claims justify detailed investigation and loss adjuster involvement. | High volume and low premiums make detailed, individual claim investigation uneconomical. |

| Profit Margin | Stable. Premiums are structured to cover risk and operational costs over a full year. | Thin. A single fraudulent claim can easily wipe out the profit from hundreds of policies. |

The table makes it starkly clear: weekly policies operate in a high-risk, low-information environment, which is a recipe for financial leakage.

The fundamental problem with insuring unknown assets for a short period is that you are paying to formalise a dispute. The claim is the first time you learn what you were actually covering, by which point it's too late.

This reactive approach is a direct path to claims leakage. The risks are even more concentrated for shorter periods, a topic explored in our guide on insurance for 1 day in the UK.

Why Current Approaches Fail for Short-Term Policies

The traditional insurance model—insure first, detect fraud at the claim stage—completely falls apart when squeezed into a seven-day timeframe. For an annual policy, investigating a claim after the event is inefficient but manageable. For insurance for a week , it’s a recipe for disputes, fraud, and spiralling operational costs.

This reactive approach places claims handlers in an impossible position. They are asked to confirm the ownership, existence, and condition of items they knew nothing about a week earlier, relying solely on the policyholder's self-declaration after a loss.

The Problem with Post-Loss Verification

Consider the 'lounge exercise': ask a policyholder to list their living room contents, and they will say it is easy. Ask them to do it from memory after a burglary, complete with makes, models, and proof of purchase, and you will spend six weeks in a dispute over undocumented possessions.

This is magnified in the chaotic situations that require weekly cover—a house move, the changing stock of a pop-up shop, or equipment in temporary storage. Relying on memory in these scenarios is a massive commercial risk.

Waiting until a claim to verify what was owned is a broken system. It creates a situation where honest policyholders struggle to prove their loss, while fraudsters find it easy to invent it.

This friction leads directly to costly delays. ABI statistics show that 35% of home insurance payouts were delayed or reduced because policyholders could not accurately list and value their contents post-loss.

An Open Invitation for Opportunistic Fraud

The reactive, post-claim model is a welcome mat for opportunistic fraudsters. It creates the perfect window for 'after-the-event' fraud, where someone insures items that were already broken, never existed, or they never owned.

Without a concrete record of an item’s existence and condition at policy inception, the insurer has no solid ground to challenge a suspicious claim. This is especially true when the time between policy inception and claim can be as short as 48 hours.

This weakness is a key reason why claims leakage spikes in travel insurance. The lack of upfront proof means the insurer is always playing catch-up, forced to either pay out on questionable claims or launch costly investigations that wipe out any profit.

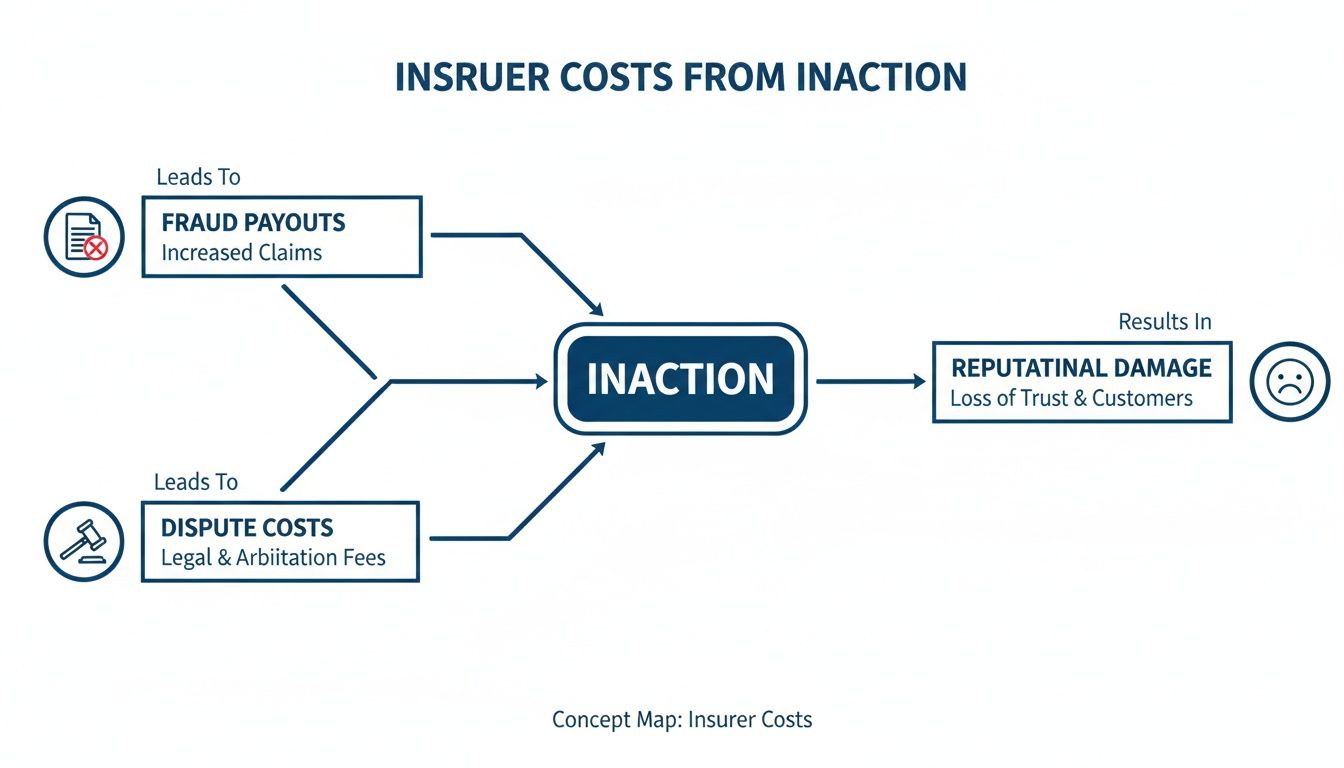

The Cost of Inaction: Quantifying the Financial Leakage

Sticking with outdated, reactive claims processes for weekly policies isn’t a neutral decision—it is a choice to accept financial leakage. In a high-volume, low-margin product line like insurance for a week , even minor inefficiencies and small fraudulent claims accumulate rapidly, causing real commercial damage.

The most obvious impact comes from fraudulent payouts. As the IFB states, undetected fraud bleeds the industry of £1.1 billion a year , much of which stems from opportunistic claims that thrive in the low-friction world of temporary cover.

The Spiralling Costs of Disputes and Delays

Beyond outright fraud, the operational costs of verifying claims after an event are immense. As soon as a claim on a weekly policy hits a snag—usually due to a lack of evidence—the meter starts running on administrative costs.

Every email, phone call, and internal review adds to the claim's expense. For a policy with a premium of perhaps £20 , it doesn’t take long to wipe out any profit. This is before considering the deployment of a loss adjuster for what should be a simple, low-value claim.

The real cost of inaction isn't just the fraudulent payout; it's the operational drag from hundreds of disputed claims. You are paying claims handlers to argue over undocumented assets, which is a fundamentally loss-making activity.

This operational strain inevitably damages the customer experience. Drawn-out disputes lead to customer churn and negative reviews, making it harder to attract good business. The financial leak is twofold: the immediate claims cost and the long-term commercial harm.

Key Areas of Financial Leakage

Ignoring the unique risks of weekly insurance policies creates tangible costs that drain profitability daily.

- Direct Fraud Payouts: Paying for items that were already broken, never existed, or were not owned by the policyholder at policy inception.

- Operational Overheads: The mounting cost of staff time spent arguing over ambiguous claims, which is disproportionate for low-premium policies.

- Loss Adjuster Expenses: Deploying third-party adjusters for small claims, an expense that can easily exceed the claim's value.

- Customer Churn: The long-term revenue lost from policyholders who leave after a poor claims experience, directly hitting market share.

Ultimately, the cost of inaction is a steady erosion of profitability, driven by a process unfit for the reality of temporary insurance.

How Pre-Inception Verification Solves This

Waiting until a claim to discover what you were covering is a guaranteed way to lose money through fraud and disputes. The only sustainable solution is to shift verification from a reactive, post-loss headache to a simple, proactive step before cover begins.

This is where pre-inception verification changes the game for insurance for a week .

Instead of relying on self-declarations, this approach requires the policyholder to create a definitive, digital record of their assets at the point of sale. Using a simple mobile app, they build a geo-tagged and time-stamped inventory, providing undeniable proof of an item's existence, condition, and location before the policy goes live.

Disarming Fraud Before It Happens

This single step makes common types of opportunistic fraud obsolete. A policyholder can no longer insure a TV with a pre-existing smashed screen and claim for a new one days later. A business cannot inflate its stock list with imaginary items. The verified digital record acts as an agreed-upon baseline—a single source of truth for both insurer and policyholder.

This is vital when a single fraudulent claim on a weekly policy, where average premiums are just £14-£22, can wipe out the profit from hundreds of policies.

As the infographic above shows, failing to verify assets upfront directly fuels higher fraud payouts, inflates operational costs from drawn-out disputes, and causes serious reputational harm.

Arming Claims Handlers with Evidence

Pre-inception verification transforms the claims process from a forensic investigation into a simple administrative check. When a claim is submitted, the handler is not starting from zero; they are comparing the claim against a pre-existing, immutable record.

The conversation shifts from, "Can you prove you owned this?" to, "Let's check the verified record you created at inception." This eliminates ambiguity, reduces the claim lifecycle from weeks to days, and dramatically cuts the operational drag on your claims department.

This evidence-led approach provides the clarity needed for swift, accurate settlements. It protects honest policyholders by making it easy to prove their losses while creating a powerful deterrent against fraud. By embedding verification at the start, you not only plug financial leaks but also build a more efficient and trustworthy claims experience.

Learn more in our detailed guide on how pre-authentication can reduce claims costs by up to 30 percent.

The Commercial Outcome: Measurable Cost Reduction and Efficiency

Implementing pre-inception verification for short-term policies delivers direct, quantifiable commercial gains. By moving evidence-gathering to the start of the policy, insurers can attack the two biggest profit drains in the insurance for a week market: opportunistic fraud and high claims processing costs.

The impact is immediate and significant. The primary win is a drastic reduction in fraud, as the process deters the most common forms of claims leakage before they are even attempted.

Slashing Fraud and Leakage at the Source

When a policyholder creates a time-stamped, geo-tagged inventory before cover starts, the opportunity for fraud vanishes. This delivers two key financial benefits:

- Elimination of 'Ghost' Item Claims: Claims for items that never existed are stopped. The verified inventory is the single source of truth; if an item is not on the pre-agreed list, it cannot be claimed for.

- Prevention of Pre-Existing Damage Fraud: A policyholder cannot insure an already-damaged item and claim for it days later. Visual proof of an item's condition at inception provides an unbreakable defence against this common and costly tactic.

The commercial win isn't catching fraud after the fact; it's creating an environment where it's not worth attempting. This shifts resources from costly investigations to settling legitimate claims quickly.

Accelerating Claims and Cutting Operational Costs

Beyond fraud prevention, the efficiency gains are enormous. The traditional claims process for an undocumented short-term policy is a minefield of disputes and delays. With a verified inventory on file, the process transforms from an investigation into an administrative check.

This shift directly impacts operational metrics. Claims lifecycles are slashed from weeks to days, customer satisfaction improves, and the claims team is freed from unproductive, margin-eroding arguments.

For brokers, this is a powerful client retention tool. A smooth, evidence-led claims process reduces post-claim complaints and reinforces their value, protecting their renewal book.

Impact Of Pre-Inception Verification On Claims Metrics

The table below quantifies how a digital inventory solution like Proova improves key claims department KPIs.

| Metric | Traditional Process | With Proova Verification | Commercial Outcome |

|---|---|---|---|

| Average Claim Lifecycle | 4-6 weeks | 3-5 days | 90% reduction in claim processing time, freeing up handler capacity. |

| Dispute Rate | 15-20% | <2% | Drastic reduction in administrative overhead and associated legal costs. |

| Loss Adjuster Deployment | Required for claims >£1,500 | Rarely required | Significant savings on third-party verification and survey fees. |

| Claims Leakage (Fraud) | 5-8% of claims value | <1% of claims value | Direct improvement to underwriting profit and loss ratio. |

The numbers speak for themselves. Shifting verification to inception doesn't just prevent fraud—it creates a faster, leaner, and more profitable claims operation.

Putting Pre-Inception Verification Into Practice

For claims directors and brokers, implementing a new process for a high-volume product like insurance for a week raises practical questions. This is not about adding friction; it is about eliminating the guesswork that costs insurers in fraud and operational drag.

How Does This Affect The Customer Journey?

The process is quick and positions the insurer as a modern, fair partner. Using a mobile app, policyholders take minutes to create a time-stamped digital inventory. For honest customers, this is reassuring, providing peace of mind that a legitimate claim will be fast and straightforward. It transforms the application from a blind transaction into a collaborative, evidence-based agreement.

What Is The Cost Of Implementation?

A verification platform like Proova is not a large capital investment. It is a low-cost, high-return operational tool that pays for itself almost immediately by reducing fraud and processing costs.

The question for a claims director is not the cost of the technology, but the ongoing cost of inaction. When one fraudulent claim can wipe out the profit from hundreds of policies, the expense of manual investigations far outweighs the cost of a preventative tool.

Is This Only for High-Value Items?

While essential for high-value assets, its power in the weekly insurance market is in tackling everyday items. Opportunistic fraud thrives on low-value goods—the £300 television, the £200 games console—that are not valuable enough to trigger a full investigation but collectively create a massive financial drain. Requiring verification for all items deters this high-volume, low-value fraud.

How Does This Benefit Insurance Brokers?

For brokers, this is about client retention and differentiation. A difficult claims process is a primary reason clients leave. By facilitating a streamlined, evidence-led claims experience, brokers demonstrate value beyond price. When a client's claim is settled in days, not weeks, it cements the broker's reputation. This means fewer complaints, stronger client relationships, and a healthier renewal book.

Stop paying claims on items that were never owned or were already damaged. Proova provides the undeniable proof at policy inception needed to eliminate fraud and slash claims processing costs. Discover how to protect your profitability today.