Comprehensive Car Insurance: What Does It Cover in the UK?

Comprehensive car insurance is the highest level of cover you can get in the UK. At its heart, it's designed to protect your own car against a whole host of real-world problems, from theft and fire to everyday accidental damage. This is a huge step up from basic policies that only cover damage you might cause to others.

Understanding Your Comprehensive Cover

It's easy to hear the word "comprehensive" and think it means absolutely everything is covered, but the reality is a bit more nuanced. The best way to think about it is as a robust safety net for your vehicle against the unpredictable. Its main job is to pay for repairs to—or the replacement of— your car.

This is the policy that handles the kind of mishaps that third-party insurance simply won't touch, many of which don't even involve another driver.

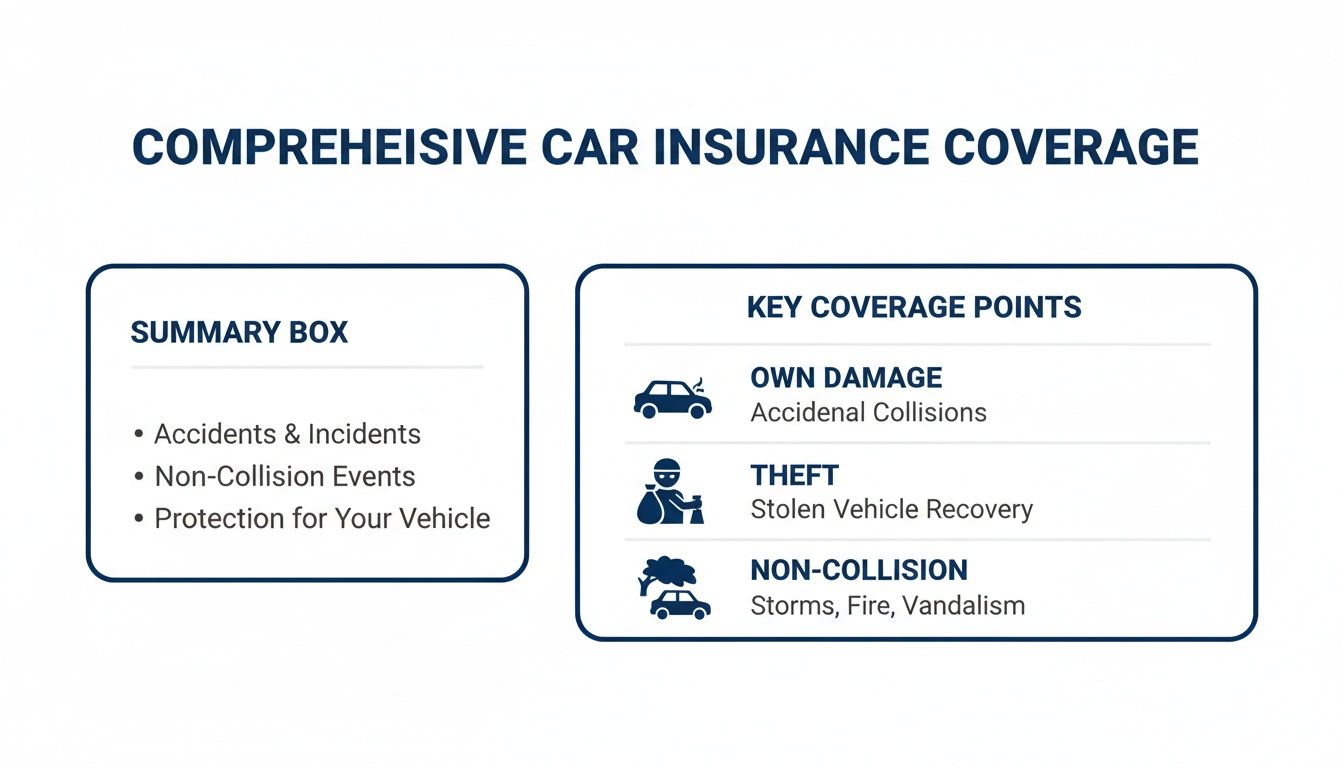

Here are some of the most common situations it covers:

- Accidental Damage to Your Car: This is the core benefit. Whether you've scraped a post in a tight car park or been involved in a more serious collision where you're at fault, this cover is what pays for your repairs.

- Theft and Vandalism: If your car is stolen and isn't recovered, or someone deliberately damages it—think of it being keyed in a supermarket car park—comprehensive cover steps in.

- Fire Damage: It protects you against damage from accidental fires, arson, or even explosions.

- Storms and Falling Objects: Picture this: you're driving down a country lane when a sudden storm brings a tree branch crashing down onto your windscreen. That's precisely the kind of non-collision damage comprehensive insurance is for. According to the Association of British Insurers (ABI), UK motor insurers paid out a staggering £2.5 billion on claims in Q3 2023 alone. A massive £1.9 billion of that went towards repairs for exactly these kinds of damages.

Comprehensive Car Insurance At a Glance

To make it simple, here’s a quick look at what a standard comprehensive policy usually includes.

| Coverage Type | What It Means For You |

|---|---|

| Damage to Your Own Vehicle | Your car is covered for repairs, even if an accident was your fault. |

| Theft and Vandalism | You're protected if your car is stolen or maliciously damaged. |

| Fire Damage | Covers damage from accidental fires, electrical faults, or arson. |

| Third-Party Liability | Still covers injury or damage you cause to others, their car, or their property. |

| Windscreen Cover | Often included for chips and cracks, sometimes with a separate, lower excess. |

| Personal Belongings | Provides limited cover for items stolen from or damaged in your car. |

While this table gives you a good overview, remember to always check your specific policy documents, as cover can vary between insurers.

Why Details Matter After an Incident

Knowing what's covered is one thing. But when you actually need to make a claim, the real test begins: proving what you've lost. This brings us to a simple problem we like to call the "lounge exercise."

Try asking a friend to list every single item in their lounge. They'll probably say it's easy. Now, ask them to do it again, but this time from memory, without looking. It suddenly becomes almost impossible. Could you do the same for your car—listing the exact model of the alloy wheels, the specific infotainment system, and any modifications—after it's been stolen or badly damaged?

For most people, the answer is no. This is where claims can slow down or get complicated. An insurer needs to know the exact condition and specification of your vehicle to settle your claim fairly. Without proof, it turns into a stressful guessing game.

Having a detailed, pre-emptive record of your vehicle turns a potential argument into a straightforward verification process. For a deeper look into the precise definitions and what they mean, especially in a commercial setting, this guide on the detailed meaning of comprehensive car insurance for UK motor trades is a great resource. It really highlights how critical clear definitions and solid evidence are.

This is why meticulous documentation isn't just about being organised. It's about making sure you get the full value you're entitled to from the policy you pay for, without all the unnecessary delays and stress.

How Comprehensive Compares to Other UK Car Insurance

To really get a feel for what makes comprehensive cover so valuable, it helps to see how it stacks up against the other options out there. In the UK, car insurance isn’t a one-size-fits-all deal; it’s split into three clear tiers of protection. Getting your head around the differences is vital because picking the wrong one could leave you facing a massive repair bill you never saw coming.

The three main types are Third-Party Only (TPO) , Third-Party, Fire and Theft (TPFT) , and of course, Comprehensive . Think of them as building blocks, with each level adding more layers of protection for you and your vehicle.

Third-Party Only: The Legal Minimum

Consider Third-Party Only cover the absolute bare minimum the law requires to drive on UK roads. It’s the most basic policy going, and its purpose is simple: to cover the costs of any damage or injury you cause to other people (the ‘third party’), their cars, or their property.

What it absolutely doesn't cover is your own car. If you have a TPO policy and you back into a bollard or you’re at fault in a collision, the bill for your own repairs is coming straight out of your pocket. It offers zero protection for your own vehicle.

Third-Party, Fire and Theft: The Next Step Up

Just as the name suggests, Third-Party, Fire and Theft (TPFT) includes everything from a TPO policy but bolts on two crucial protections for your own car:

- Fire: If your car is damaged by an accidental fire, lightning, or an act of arson.

- Theft: If your car is stolen or damaged when someone tries to steal it.

This is a big step up, but there’s still a major gap in the armour. A TPFT policy will not pay out for any other damage to your vehicle. If you're in an accident that's your fault, you're still on the hook for the entire repair cost, which could easily run into thousands of pounds.

Comprehensive Cover: The Complete Picture

Finally, we arrive at comprehensive cover . This policy bundles everything from the previous two levels—third-party liability, fire, and theft—and adds the most important piece of the puzzle: cover for damage to your own car . This protection kicks in even if an accident was your fault.

This diagram breaks down the core protections you get with a comprehensive policy.

The key takeaway is that comprehensive is the only type of policy that acts as a full safety net, protecting your vehicle against accidental damage from a whole range of incidents.

It means that if you misjudge a tight parking spot, get hit by an uninsured driver, or a storm sends a tree branch crashing onto your roof, your policy is there to help. For a more detailed look at how these policies compare, our guide on third-party insurance vs comprehensive cover offers a deep dive for insurers and brokers.

To make it even clearer, let's compare the three main policy types side-by-side.

UK Car Insurance Cover Compared

| Feature | Third-Party Only (TPO) | Third-Party, Fire & Theft (TPFT) | Comprehensive |

|---|---|---|---|

| Damage/Injury to Others | ✅ | ✅ | ✅ |

| Damage to Your Car (Theft) | ❌ | ✅ | ✅ |

| Damage to Your Car (Fire) | ❌ | ✅ | ✅ |

| Damage to Your Car (Accident) | ❌ | ❌ | ✅ |

| Windscreen Damage | ❌ | ❌ | Often included |

| Personal Belongings | ❌ | ❌ | Often included |

| Personal Accident Cover | ❌ | ❌ | Often included |

This table shows at a glance how each level builds on the last, with comprehensive offering by far the widest range of protection.

There's a persistent myth that comprehensive insurance is always the most expensive option. This is often not the case. Over time, insurers noticed that drivers choosing basic third-party cover sometimes fit a higher-risk profile, which can bizarrely push their premiums up.

Always get quotes for all three levels of cover. You might be surprised to find that the most complete protection doesn't always come with the highest price tag, giving you far greater peace of mind for a similar cost.

Common Exclusions in a Comprehensive Policy

While the word "comprehensive" sounds like it covers everything, no car insurance policy is a blank cheque. It’s better to think of it as a powerful safety net with clearly defined edges. Understanding what falls outside that net is just as important as knowing what’s inside, as it helps manage expectations and avoids the shock of a rejected claim.

A lot of these exclusions are just common sense. Your policy is there to protect you from sudden, unexpected events—not the predictable costs of simply running a car. That’s why insurers won’t pay out for problems that are part of a vehicle's general upkeep or a result of simple, preventable mistakes.

General Wear and Tear

One of the most common exclusions you'll find is for general wear and tear . Over time, parts of your car will naturally degrade and need replacing. This isn’t an insurable event; it's a standard maintenance cost.

This umbrella covers things like:

- Tyres wearing thin after thousands of miles.

- Brake pads and discs reaching the end of their life.

- The exhaust system corroding over the years.

Your insurer won't cover these because they are an expected part of owning a car. However, there's a crucial distinction. If a worn-out component causes an accident—say, a threadbare tyre blows out and you hit a barrier—the damage to your car's bodywork from the crash would likely be covered by your policy.

This is where having clear, dated documentation becomes so valuable. A time-stamped visual record of your vehicle's condition before an incident makes it much easier to distinguish between pre-existing wear and new, claimable damage. It removes the guesswork and helps your insurer process the claim without unnecessary delays.

Mechanical and Electrical Breakdowns

Another major area that's typically excluded is mechanical or electrical failure. If your engine seizes, your gearbox gives up, or the onboard computer develops a fault, your comprehensive policy isn't the solution. These sorts of internal problems are usually covered by a manufacturer’s warranty on a new car, or by a separate mechanical breakdown policy you can buy.

Think of it this way: your comprehensive policy covers damage from an external event, not internal failure. It will pay for the damage caused by hitting a tree, but not for the engine failure that might have caused you to lose control in the first place.

Common Driver Errors and Misuse

Insurers also draw a line at damage caused by certain types of driver error or misuse. These are situations where the damage wasn't caused by a traditional accident but by a completely preventable mistake.

A few classic examples include:

- Misfuelling: Putting petrol into a diesel engine (or vice versa) can cause thousands of pounds in damage, but it’s almost always excluded from a standard policy. Some insurers do offer "misfuelling cover" as an optional extra.

- Using the Wrong Type of Cover: If you start using your personal car for business purposes, like making deliveries for a fee, a standard personal policy won't cover you in an accident. You’d need a proper commercial or "business class" policy.

- Deliberate Damage or Negligence: Intentionally damaging your own car is insurance fraud and is never covered. Likewise, extreme negligence—like leaving your keys in the ignition with the engine running—might give the insurer grounds to reject a theft claim.

Understanding these exclusions isn't about finding fault with insurance companies; it's about being a savvy policyholder. It equips you with a clear picture of what comprehensive car insurance does cover , so you can make informed choices and avoid any unwelcome surprises when you need your cover the most.

Popular Add-Ons to Enhance Your Cover

Think of your standard comprehensive policy as a solid foundation. It covers the big, important risks, but your own needs might call for a few extra layers of protection. This is where add-ons, or optional extras, come into play.

These bolt-ons let you build a policy that fits your life perfectly, rather than settling for a one-size-fits-all solution. Insurers offer a whole range of them, and choosing the right ones can make a massive difference if you ever need to make a claim. The goal is to pick add-ons that give you genuine value, not just tick every box and inflate your premium.

Let's walk through some of the most common and useful options you'll find in the UK.

Breakdown Assistance

This is probably the most well-known add-on of them all. If your car grinds to a halt on the side of the road with a mechanical failure, this cover ensures a recovery service will come to your rescue.

Policies vary from basic roadside assistance to more complete packages that include help if you break down at home (home start) and onward travel arrangements.

Courtesy Car Cover

If your car is in the garage for repairs after an incident, how will you get around? A standard policy might not automatically provide a replacement vehicle, which can be a real headache.

Enhanced courtesy car cover makes sure you’re given a temporary vehicle to use, keeping you on the road and minimising disruption. It’s an absolute lifesaver for daily commuters or parents on the school run.

Legal Expenses Protection

Imagine you're in an accident that wasn't your fault. While your insurer handles your car's repairs, you could be left with other out-of-pocket costs, often called "uninsured losses." These might include your policy excess, loss of earnings, or even personal injury claims.

Legal expenses cover provides the funds to hire a solicitor to pursue these costs from the at-fault party's insurer. Without it, you could be left to fight that battle—and fund it—all on your own.

Other Valuable Add-Ons

Beyond the big three, several other options can really strengthen your policy and give you extra peace of mind.

- No-Claims Bonus (NCB) Protection: Your NCB is a valuable discount you've earned over years of claim-free driving. This add-on lets you make one or two claims within a set period without it affecting your hard-earned discount.

- Key Cover: Modern car keys can be incredibly expensive to replace. This covers the cost of replacing lost or stolen keys and reprogramming your car’s security system, potentially saving you hundreds of pounds.

- Personal Belongings Cover: While a standard policy offers some protection for items in your car, you can often increase this limit. This is great for covering more valuable possessions like laptops or sports equipment. Just remember, the same rule applies here as with your home contents—if you can't prove what was in the car, claiming for it gets tricky.

- Dashcam Cover: Installing a dashcam can provide crucial, impartial evidence in an accident. You can learn more about how they can impact your policy in our guide exploring if dashcams lower insurance premiums in the UK.

- Anti-Theft Devices: Beyond just insurance add-ons, physical enhancements can also play a role. For instance, investing in approved car anti-theft devices can sometimes lead to lower premiums because they reduce the risk of theft in the first place.

Why Clear Documentation Is Key to Your Claim

Knowing what your comprehensive car insurance covers is only half the story. The other, often trickier, part is actually proving your loss when you need to make a claim. This is where a perfectly good policy can unravel into a frustrating, drawn-out settlement process.

Think back to our 'lounge exercise'. It’s one thing to list everything in your living room while you’re sitting there, but could you recall every single item from memory after a fire? Now, apply that same test to your car after it’s been stolen or badly damaged.

Could you, in the heat of the moment, remember the exact make and model of your alloy wheels? What about the serial number of that expensive infotainment system you had fitted? For most of us, those details vanish under stress. This lack of proof is exactly what causes delays, arguments over value, and ultimately, a smaller payout than you deserve.

The Problem of Proving Ownership and Condition

When you file a claim, your insurer’s job is to get you back to the financial position you were in right before the incident happened. To do that accurately, they need to know precisely what they're covering. Without solid evidence, they have to rely on your memory—which, especially after a traumatic event, is never foolproof.

This information gap is at the heart of so many claim disputes. An insurer might question the car's condition before the crash or debate the value of specific modifications you’ve made.

Just think about these common scenarios where documentation makes all the difference:

- Modified Vehicles: Did you upgrade the sound system, add custom wheels, or install a roof rack? Without dated photos and receipts, these valuable extras could easily be missed in your settlement.

- Theft Claims: Proving what was inside the car when it was stolen is incredibly tough. A simple digital inventory of personal items you normally keep in the vehicle provides concrete evidence.

- Condition Disputes: After an accident, an insurer might suggest some of the damage was just pre-existing wear and tear. A clear, time-stamped visual record of your car’s condition shuts that conversation down before it even starts.

Having this proof ready to go completely changes the claims process. It shifts the dynamic from a stressful negotiation based on memory to a straightforward verification of facts. The result? A faster, fairer settlement with a lot less anxiety. This is especially true when it comes to separating genuine claims from fraudulent ones, a topic we explore in our guide on how real-time evidence changes everything from theft to payout.

From Guesswork to Certainty

The solution is simple: create a complete, verified digital record of your vehicle before you ever need it. This gives you the undeniable evidence insurers need to settle your claim quickly and fairly. It completely removes the stress of trying to remember what you’ve lost when you’re at your most vulnerable.

For many drivers, the real pain comes from claims being rejected or paid out at a lower value due to poor proof of ownership or condition. This is where an app like Proova becomes invaluable. By photographing your car's assets and logging key details at the start of your policy, you build an ironclad database. This approach helps slash fraudulent claims—like 'after-the-event' damage reports—by proving ownership and value from day one.

Ultimately, a comprehensive policy is only as good as your ability to prove your claim against it. By documenting everything upfront, you ensure you get the full benefit of the cover you pay for, turning a potential disaster into a manageable inconvenience.

Your Comprehensive Car Insurance Questions Answered

Even when you've got your head around the basics of comprehensive cover, a few practical questions always pop up. Car insurance can feel needlessly complicated, but most queries boil down to real-world situations. Let's clear up some of the most common ones you'll hear in the UK.

Does Comprehensive Cover Mean I Can Drive Any Other Car?

This is a huge one, and getting it wrong can be incredibly costly. Years ago, many comprehensive policies included a ‘Driving Other Cars’ (DOC) benefit, but this is becoming much rarer today. You should never, ever assume it’s included.

Even when it is part of your policy, the cover is almost always just third-party only . What does that mean in practice? If you borrow a friend's car and have a crash that's your fault, your insurance would pay for the damage to the other car involved. But it would provide zero cover for the car you were driving . Your friend would be left with a damaged car and a hefty repair bill.

Driving without the right insurance is a serious offence, leading to big fines and points on your licence. Before you get behind the wheel of someone else’s car, always read the fine print of your policy documents.

Will Making a Claim Always Affect My No-Claims Bonus?

Usually, yes. Making a claim will almost certainly knock your no-claims bonus (NCB). The only real exception is when the accident was clearly not your fault, and your insurer manages to get all their money back from the other driver's insurance company. If they recover 100% of the costs, your NCB should be safe.

But there is a way to shield this valuable discount. Most insurers offer No-Claims Bonus Protection as an optional extra.

For a relatively small top-up on your premium, this add-on lets you make one or sometimes two 'at-fault' claims over a few years without losing your NCB. It’s a popular safety net, protecting years of careful driving from being wiped out by a single mistake.

It's worth remembering, though, that even with a protected NCB, your base premium might still go up at renewal. Your claims history is a big part of how insurers calculate your price, and a recent claim flags you as a higher risk.

Is Comprehensive Insurance Always the Most Expensive Option?

It feels like it should be, right? More cover, more cost. But surprisingly, the answer is often no. Insurers build their prices on massive amounts of risk data, and over the years, a strange pattern has emerged: drivers who choose the most basic third-party cover are sometimes, as a group, more likely to be involved in an incident.

This can lead to the bizarre situation where a third-party policy is actually more expensive than a comprehensive one for the exact same driver and car. The only way to know for sure is to get quotes for all three levels of cover—Third-Party Only, Third-Party Fire & Theft, and Comprehensive.

You might just find that getting the best protection on the market also happens to be the best deal.

How Can I Prepare Now for a Potential Car Insurance Claim?

There's one thing you can do right now that will make a world of difference later: create a detailed, undeniable record of your car and its condition before anything happens. This simple bit of prep can be the difference between a quick, fair payout and a drawn-out, stressful argument with your insurer.

Think back to the 'lounge exercise' – it’s almost impossible to list everything you own from memory, especially when you're stressed. The same goes for your car and its features.

This is exactly the problem an app like Proova was built to solve. Here’s how you can get prepared:

- Photograph Everything: Walk around your car and take clear, well-lit photos of the exterior from every angle. Then do the same for the interior – the dashboard, the seats, and any special tech like the infotainment system.

- Document Modifications: Have you spent money on upgrades? Special alloy wheels, a performance exhaust, or a better sound system all add value, but you need to prove they were there. Photograph them and keep the receipts.

- Record Serial Numbers: For high-value items like the stereo or navigation unit, jotting down the serial number is brilliant evidence if it gets stolen.

By creating a verified, time-stamped digital inventory of your vehicle, you give your insurer indisputable proof of its condition and value. It cuts through the ambiguity, massively speeds up the claims process, and ensures you get a settlement that truly reflects what you've lost.

Don't wait until you’re trying to prove what you owned after the fact. With Proova , you can easily create a secure, verified digital record of your car and its features, giving you the undeniable evidence you need for a fast and fair insurance claim. Download the free Proova app today and get prepared.