A Guide to Framework Risk Management in UK Insurance

A framework risk management approach is the blueprint an organisation uses to build its financial and operational stability. Think of it as a structured, repeatable system for identifying, assessing, and controlling threats before they can cause real damage.

Understanding the Need for a Risk Framework

Imagine trying to build a house without proper blueprints. You might end up with walls and a roof, but the structure would almost certainly be unstable, unsafe, and unfit for purpose. A risk management framework is that essential blueprint for an insurance organisation.

It moves a business away from chaotic, reactive problem-solving—like only buying sandbags when the floodwaters are already rising—towards a proactive and structured defence. In the UK insurance sector, where managing unforeseen events is the core business, this isn't a luxury; it's a necessity for survival and compliance.

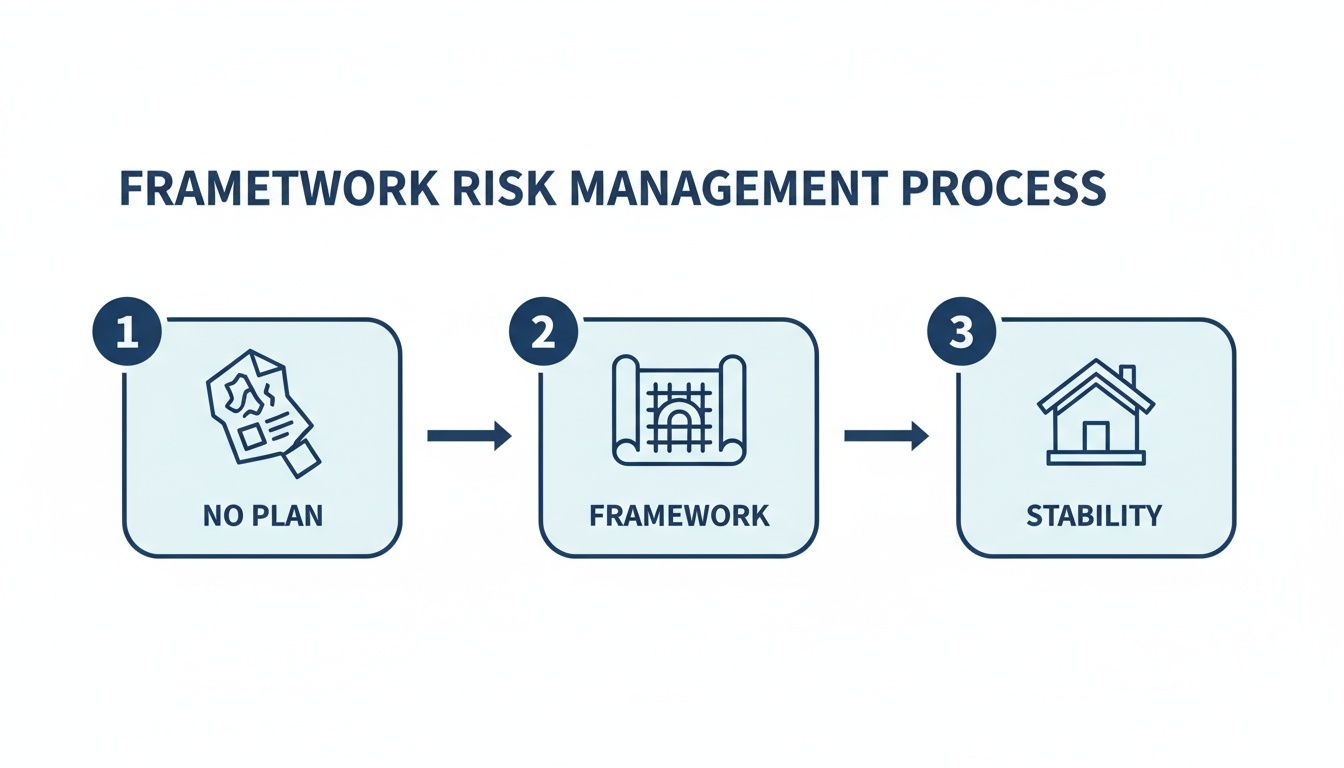

The Problem of Operating Without a Plan

Operating without a formal framework is like asking a homeowner to list every single item in their lounge from memory, complete with serial numbers. As our 'lounge exercise' analogy shows, it’s an impossible task. An insurer trying to manage risk without a system faces a similar challenge, which inevitably leads to significant blind spots.

This lack of structure brings tangible and costly consequences:

- Increased Fraud: Without a system to verify assets at policy inception, insurers are wide open to 'after-the-event' fraud, where a claim is made for an item that was never owned or was already damaged.

- Delayed Claims: Inconsistent processes and missing information create bottlenecks, slowing down claim settlements and damaging customer satisfaction. This kind of inefficiency can quickly attract scrutiny from the Financial Conduct Authority (FCA).

- Regulatory Penalties: UK regulators expect insurers to have robust systems for managing risk. A failure to demonstrate this can lead to hefty fines and serious reputational damage.

- Inaccurate Underwriting: When risk is based on assumptions rather than concrete data, policies are often mispriced. This leads to an unbalanced and unprofitable portfolio.

This infographic shows the journey from having no plan at all to achieving stability through a structured framework.

It clearly shows how adopting a formal framework transforms a chaotic, unplanned approach into a solid foundation for organisational stability and resilience.

A Structured System for Control

A framework provides the architecture for managing all types of business threats in a coordinated way. For example, a robust occupational health and safety management system is a practical example of a structured framework designed to manage specific workplace risks. In the same way, an insurance framework integrates processes across underwriting, claims, and fraud prevention.

A risk management framework is not just a document to be filed away. It is a living system that enables an organisation to consistently identify threats, make informed decisions, and protect its long-term health.

By defining roles, responsibilities, and clear procedures, it ensures everyone in the organisation understands how they contribute to risk mitigation. This creates a culture where risk is managed proactively, turning uncertainty into a calculated and controlled part of the business model.

The Core Components of an Effective Risk Framework

A proper risk framework isn’t just a policy document you file away and forget. It’s a living, breathing system built from four essential parts, all working together to protect your organisation. Let's ditch the corporate jargon and think of these as clear, actionable steps for building a proactive defence against uncertainty.

Each component naturally builds on the last, creating a continuous loop of identification, assessment, mitigation, and review. It's this structured approach that transforms reactive fire-fighting into strategic foresight.

Risk Identification

First up is Risk Identification . This is all about proactively spotting threats before they can blow up into major problems. It means looking beyond the obvious and finding potential weak spots across the entire business.

For a UK insurer, this could involve:

- Digging into claims data to spot patterns that point towards organised fraud rings.

- Pinpointing the operational bottlenecks that always seem to slow down claim settlements.

- Recognising where gaps in underwriting data are leading to mispriced policies.

Effective identification requires a real understanding of both your internal processes and what’s happening in the wider world. It’s about asking "what could go wrong?" in every corner of the organisation.

Risk Assessment and Analysis

Once you’ve spotted a potential risk, the next step is Risk Assessment and Analysis . This is where you figure out the likelihood of it actually happening and just how bad the fallout would be if it did.

This process helps you separate minor headaches from business-critical threats, so you can focus your resources where they count. An insurer might decide, for example, that while the chance of a massive data breach is low, the financial impact would be catastrophic, making it a high-priority risk. On the other hand, small administrative errors might happen more often but have a tiny impact.

A proper assessment transforms a long list of potential problems into a clear, prioritised action plan. It ensures you focus your efforts on the threats that truly matter to your business stability.

Risk Mitigation and Control

With a solid grasp of your key risks, it’s time for Risk Mitigation and Control . This is the practical bit—implementing strategies and controls designed to reduce the chances or impact of those identified threats.

These controls can be preventative (stopping a problem before it starts) or detective (flagging an issue as it happens). A perfect example of a preventative control is tackling 'after-the-event' fraud head-on.

By requiring policyholders to provide a verified digital inventory from Proova when a policy begins, an insurer completely neutralises this risk. The timestamped, geo-located record provides undeniable proof of what was owned before cover started, making it impossible to claim for an item that was already damaged or never even existed. For more on this, check out our complete guide to your business risk management framework.

Monitoring and Review

Finally, a risk framework is never truly "finished." Monitoring and Review is the ongoing process of keeping an eye on your identified risks, checking how well your controls are working, and adapting your strategy to new challenges as they appear.

The risk landscape is always shifting, from new fraud techniques to changing regulatory demands from bodies like the FCA. A regular review process makes sure your framework stays relevant and effective. This continuous loop of feedback and improvement is what turns a risk framework into a powerful tool for building genuine, long-term resilience.

Comparing Major Frameworks: ISO 31000 vs COSO

Choosing a risk management framework can feel a bit like picking a blueprint for a house. For most organisations, especially in the insurance world, the choice often comes down to two major players: ISO 31000 and the COSO ERM Framework .

While they both aim to build a strong structure for managing risk, they approach the job from very different angles. Getting to grips with these differences is the first step in deciding which one is the right fit for your insurance organisation.

Here’s a simple way to think about it. ISO 31000 is like a set of flexible, high-level architectural principles. It gives you the fundamental concepts of good design—like integrating risk management into every department, from claims to underwriting—but trusts you to draw up the specific plans that suit your unique operational needs.

COSO, on the other hand, is much more like a detailed, prescriptive building code. It provides a rigid structure with specific components you must have in place, with a heavy focus on internal controls, financial reporting, and strict governance. It’s no surprise it's a popular choice for organisations facing intense regulatory scrutiny.

ISO 31000: A Flexible Set of Principles

It’s important to realise that ISO 31000 is a set of guidelines, not a standard you can get a certificate for. Its real purpose is to embed a risk-aware mindset deep into an organisation’s culture and day-to-day decision-making. It’s built on the core idea that risk management isn't a separate, siloed activity but an integral part of everything a business does.

Its key characteristics are:

- Adaptability: It’s designed to be applied to any organisation, no matter its size, sector, or the specific risks it faces.

- Integration: It strongly champions the idea of weaving risk management into governance and all other business activities.

- Holistic View: It encourages a wide-angle view of risk, covering everything from top-level strategic objectives to daily operations.

For a UK insurer, ISO 31000 provides the guiding principles to create a more joined-up approach, helping to manage everything from large-scale underwriting risk down to the specific operational risks within the claims department.

COSO ERM: A Prescriptive Structure

The COSO Enterprise Risk Management (ERM) Framework is a different beast altogether—far more structured and formal. It originally grew out of efforts to help organisations prevent financial statement fraud, and that DNA is still very apparent in its focus on internal controls and governance. This makes it a natural favourite for businesses in heavily regulated sectors like finance and insurance.

Its foundation is built on five interconnected components:

- Governance and Culture: Setting the tone from the top and establishing clear responsibilities.

- Strategy and Objective-Setting: Defining the organisation's risk appetite and aligning it with its core strategy.

- Performance: The nuts and bolts of identifying, assessing, and responding to risks.

- Review and Revision: Continuously assessing how the framework is performing and making improvements.

- Information, Communication, and Reporting: Ensuring risk information flows freely and clearly across the organisation.

For UK insurers, COSO's prescriptive nature can align very neatly with the stringent requirements set out by regulators like the Financial Conduct Authority (FCA), especially around internal controls and transparent reporting.

ISO 31000 vs COSO: A Practical Comparison for Insurers

Choosing between these two leading frameworks isn't about which one is "better" but which one is the "best fit" for your insurer's specific needs, culture, and regulatory landscape. The table below breaks down the key differences to help guide your decision.

| Aspect | ISO 31000 | COSO ERM Framework |

|---|---|---|

| Primary Focus | Integrating risk management into all organisational processes and decision-making. | Internal controls, financial reporting, and achieving business objectives. |

| Approach | A set of flexible principles and guidelines. Not certifiable. | A formal, prescriptive framework with specific components and principles. |

| Scope | Broad and universal. Applies to any type of risk across the entire organisation. | More focused on enterprise-level risks, particularly those related to finance and operations. |

| Best For | Organisations wanting to build a deep, integrated risk culture and a custom-fit system. | Regulated industries needing to demonstrate compliance and strong internal controls. |

| Audience | Risk managers, leadership teams, and operational managers. | Boards, audit committees, and senior management. Primarily governance-focused. |

In short, if your main goal is to embed a proactive, risk-aware culture throughout your entire operation, ISO 31000 offers an excellent, adaptable guide. If, however, your priority is demonstrating robust compliance and strengthening financial controls to satisfy regulators, COSO’s ready-made structure is hard to beat.

It’s also worth remembering that these aren't the only options out there. For a deeper dive, especially into security, you can explore other cyber risk management frameworks like NIST and ISO 27001 to broaden your understanding.

Ultimately, the right choice comes down to your organisation's strategic goals, your regulatory environment, and how much structural guidance you need to get the job done.

Understanding the UK's National Risk Management Approach

A strong risk management framework doesn’t operate in a vacuum. For UK insurers, it has to connect with the much larger national strategy designed to protect the country from major threats. This link makes the whole concept of risk management feel both more tangible and far more urgent.

Any effective internal framework must account for the external environment. In the UK, that means understanding the government’s own blueprint for resilience, which offers invaluable intelligence for any insurer looking to stay ahead.

The UK Government's Resilience Framework

At the heart of this is The UK Government Resilience Framework . Think of it as the nation's strategic plan for preparing for, responding to, and recovering from just about any major crisis you can imagine. It promotes a whole-of-society approach, making it clear that resilience isn't just a job for Whitehall—it's a shared responsibility between public services, private industry, and individuals.

For insurers, this framework is much more than just another policy document. It’s a clear signal of government priorities, highlighting where the private sector is expected to step up and play a crucial role in building national preparedness. It directly shapes how insurers should think about large-scale, systemic risks.

Tapping into the National Risk Register

The most practical tool to come out of this strategy is the National Risk Register (NRR) . This is a public document that gives a transparent and detailed assessment of the biggest threats facing the country over the next two years, from widespread flooding and pandemics to crippling cyber-attacks.

The NRR isn’t based on guesswork. The UK's National Risk Register 2023, for instance, drew on over 25,000 data points . It ranks threats by likelihood and potential impact—for example, a massive cyber-attack is deemed highly likely to cause catastrophic disruption for weeks. For insurers, this register is a goldmine of strategic intelligence that can be used to sharpen and validate their own internal risk models. You can dig into the latest findings in the official government report on the UK Government Resilience Framework.

By using the NRR, insurers can align their underwriting strategies and claims planning with government-identified priorities. This ensures their own framework is focused on the most credible and impactful threats facing their policyholders.

This high-level intelligence has very real, ground-level implications. When the government flags a specific threat like flooding as a top-tier national risk, it creates a powerful business case for proactive mitigation right down to the individual policy. It drives home just how critical it is for homeowners and businesses in vulnerable areas to have meticulously documented inventories of their assets.

This national context bridges the gap between high-level strategy and the everyday challenges of insurance. A threat identified in a government report directly translates into the need for a homeowner in a flood-prone area to have a clear, verifiable record of their belongings before disaster strikes.

This is precisely where national strategy meets practical solutions. Tools like Proova empower both insurers and their customers to act on this vital intelligence. By enabling policyholders to create a verified digital catalogue of their possessions, it provides the essential evidence needed to navigate a claim smoothly when a national-level risk becomes a personal crisis. It turns a theoretical framework into a practical defence.

How to Implement a Risk Framework in Your Organisation

Bringing a risk management framework from theory to reality isn’t about a disruptive overhaul. It's a structured process that delivers a powerful return when you have clear steps, strategic buy-in, and the right tools.

Moving from a blueprint to a working system is a manageable journey that builds lasting resilience.

It all starts with securing commitment from the top and getting the right people in the room. A framework imposed by a single department will always struggle; success depends on a collaborative, business-wide effort.

Secure Senior Management Buy-In

First things first: you need the full support of your senior leadership team. A risk framework isn't just a compliance exercise. It's a strategic asset that protects profits, improves customer satisfaction, and strengthens the business against future shocks.

To get that backing, you need to frame it in terms of strategic value. Talk about the commercial benefits—reduced claims leakage from fraud, faster settlement times, and more accurate underwriting. Go beyond just risk mitigation.

It's also crucial to connect it to regulatory duties. The Bank of England's Prudential Regulation Authority (PRA) has put a huge emphasis on accountability. In May 2023 , it released SS1/23 , which outlines principles for model risk management that demand strategic ownership from leaders via their Senior Management Functions (SMFs). This regulatory pressure makes it clear: a robust framework is no longer optional.

You can learn more about PRA expectations for model risk management on bankofengland.co.uk.

Assemble a Cross-Functional Team

Once leadership is on board, your next move is to build a cross-functional team. Risk management isn't one department's job. To get a complete picture, you need input from every corner of the business that deals with risk.

Your team should include people from:

- Claims: They know the settlement bottlenecks and common points of dispute inside out.

- Underwriting: They can ensure the framework supports more accurate risk pricing.

- Fraud: Their input helps identify vulnerabilities and build in preventative controls.

- Compliance: They’ll make sure the framework aligns with FCA and PRA requirements.

This approach ensures the final framework is practical and addresses the real-world challenges your teams face every day.

Customise and Integrate Technology

Your chosen framework, whether it's ISO 31000 or COSO, needs to be tailored to the specific risks of the UK insurance market. This is where you turn a generic template into a system built for your business. The most important part of this stage is integrating the right technology to power it with reliable data.

A framework without accurate data is like a car without fuel. This is where Proova’s technology becomes a foundational piece of the puzzle. By providing verified, pre-inception asset data, Proova strengthens every single stage of the risk lifecycle.

For underwriting, Proova supplies the ground-truth data needed for accurate risk assessment. For claims, it provides irrefutable evidence that reduces fraud and speeds up settlement, completely changing the customer experience.

This integration is a core pillar of any successful rollout. By embedding verified data right at the start of the policy lifecycle, you turn your framework from a passive guide into an active defence. It's a vital part of the wider digital transformation in the insurance industry a UK guide describes.

Drive Adoption Through Training and Communication

Finally, a framework is only effective if people actually use it. Roll out a clear training and communication plan so everyone understands their role and what's expected of them. The goal here is to embed a culture of proactive risk awareness, not just to tick a training box.

Show your teams how the new processes make their jobs easier. Explain how underwriters can price with more confidence or how claims handlers can resolve cases faster. When your people understand the "why" behind the framework, adoption will follow naturally.

Why Verified Data Is the Foundation of Effective Risk Management

A risk management framework is only as good as the data that powers it. That’s a simple truth. Every single component, from the initial assessment right through to mitigation, hinges on having accurate, timely information. Without a single source of truth, even the most sophisticated framework is just a house of cards, built on guesswork and assumptions.

This is where verified asset data becomes the bedrock of any solid risk management strategy. It’s the crucial link that connects every high-level concept back to the ground-truth reality of what an insurer is actually covering.

Strengthening Every Component of the Framework

Let's revisit the framework's core components and see how pre-inception, geo-tagged digital inventories completely change the game. It’s about turning theoretical processes into practical, data-driven actions.

For underwriting and risk assessment , verified data provides a crystal-clear picture of the risk from day one. Instead of relying on vague descriptions or outdated valuations from policyholders, underwriters can see exactly what assets are on-site. This dramatically reduces the need for costly physical surveys and helps prevent mispriced policies right from the start.

When it comes to claims handling and risk mitigation , an undisputed digital record is a genuine game-changer. It offers irrefutable proof of an item's existence and condition before a policy even begins, which accelerates processing times, minimises disputes, and massively improves customer satisfaction when they need it most.

A Proactive Defence Against Fraud and Uncertainty

Perhaps the most significant impact is on fraud prevention . 'After-the-event' fraud—where a policy is taken out to cover an item that's already damaged or doesn't even exist—is virtually eliminated. A timestamped digital record created before the policy inception date is the ultimate preventative control. You can discover more about fighting fraud before it happens with the power of verified evidence.

This approach mirrors a broader national strategy. True resilience, as the UK government has emphasised, starts with knowing exactly what you are protecting. The government’s own Resilience Framework was built on a massive data overhaul, incorporating 25,000 pieces of data to create the most transparent National Risk Register ever. This national focus on data-driven preparedness underscores just how critical ground-level asset intelligence has become.

The ultimate takeaway is clear: verified, pre-inception data isn't just an add-on; it's the foundational element that makes any risk framework more effective, efficient, and robust. It transforms risk management from a theoretical exercise into a practical, evidence-based defence.

Your Questions, Answered

Here are some straight-talking answers to the questions we hear most often about bringing risk management frameworks to life in the UK insurance industry.

What’s the Real Goal of a Risk Management Framework?

At its heart, the main goal is to shift your entire organisation's mindset from reactive "fire-fighting" to proactive and strategic thinking. Instead of scrambling to deal with crises as they happen, a good framework gives you a structured way to spot, assess, and control threats long before they can cause serious damage.

For UK insurers, this translates directly into protecting your financial stability, staying on the right side of regulators like the FCA , and making everything from claims to underwriting run more smoothly.

How Long Does It Actually Take to Implement a Framework?

This is a common question, but it’s a bit like asking how long it takes to get fit. The initial setup—getting leadership on board, putting a team together, and tailoring a model like ISO 31000 or COSO to your business—might take a few months.

But implementation isn't a project with a finish line; it’s a permanent change in how you do business. The real work is embedding risk awareness into your company culture, which is a continuous cycle of monitoring, reviewing, and adapting to whatever comes next.

Are Risk Frameworks Just for the Big Players?

Absolutely not. The core principles of managing risk are completely scalable and just as relevant to a small MGA as they are to a massive multinational insurer.

A smaller firm will naturally have a simpler framework with fewer formal controls, but the fundamental process of identifying and managing threats is exactly the same. The key is to build a system that’s proportionate to the size and complexity of your operation.

How Does a Framework Actually Help My Customers?

A solid framework has a direct and positive impact on your policyholders. For example, when you integrate verified data on a customer's assets right from the start of a policy, you can slash the time it takes to process a claim and cut down on frustrating disputes.

This leads to much faster settlements and happier customers. It also means you can price policies more accurately, ensuring people pay a fair premium based on real, data-driven assessments instead of guesswork and broad assumptions.

What's the Single Biggest Mistake to Avoid?

Without a doubt, the most common pitfall is treating your framework as a box-ticking exercise just to keep the compliance department happy. A framework that only exists in a dusty binder on a shelf is completely useless.

To have any real value, it needs to be a living, breathing part of your organisation. It must be actively used to inform daily decisions, be properly integrated with your technology, and be championed from the top down to create a genuine culture of risk awareness.

A robust risk management framework is only as good as the data it's built on. Proova provides that ground-truth intelligence, strengthening every stage from underwriting right through to claims. See how our pre-inception digital inventories can help you reduce fraud, cut costs, and delight your customers.