UK Window Cleaning Insurance Guide

Window cleaning insurance is not just another business expense you have to stomach; it is the single most important tool for your professional survival and growth. For a relatively small monthly premium, you are buying a critical safety net against the kind of accidents that could otherwise sink your business overnight.

Why Insurance Is Your Most Important Tool

Think about all your gear—squeegees, ladders and water-fed poles. They are all essential for doing the job but none of them can protect you when something goes pear-shaped. A simple slip could send a ladder crashing through a customer's conservatory roof or, even worse, injure a passerby. Without insurance, the compensation claim from that one incident could easily bankrupt your entire business.

This is where the right window cleaning insurance steps in to become your most valuable asset. It acts as a financial shield, picking up the tab for legal fees and compensation costs that spring from accidents. This is not just about dodging disaster; it is about building a resilient, trustworthy business from the ground up.

The Growing Need for Professional Cover

The UK window cleaning industry has been quietly booming, expanding by an average of 6.4% per year between 2019 and 2024. Most of this growth comes from small businesses and sole traders just like you. But here is a shocking statistic: studies show that nearly half of all UK small and medium-sized enterprises have no insurance at all and many more are likely underinsured.

In a trade as hands-on and potentially hazardous as window cleaning, that gap in cover is a massive risk for both the operators and their clients. For many customers, especially in the commercial sector, seeing proof of insurance is now a deal-breaker. They need to know you operate professionally and can handle any potential damages. If you do not have adequate cover, you are automatically out of the running for those bigger, more lucrative contracts, which really puts a cap on your growth potential. Investing in insurance does not just protect you; it opens doors.

Protecting Your Reputation and Future

Beyond the financial security, insurance is your best defence for your professional reputation. An uninsured accident can trigger a tidal wave of negative word-of-mouth that could permanently poison your client base. On the flip side, being fully insured sends a powerful message. It shows you are responsible and gives your clients genuine peace of mind.

Having robust insurance cover is not just about ticking a box; it is a clear signal to your customers that you are a serious professional dedicated to quality, safety, and accountability.

Let’s be honest, there are inherent risks in this trade, especially when you are working off the ground. It is vital to follow expert safety guidance for working at heights to minimise incidents. Ultimately, that small monthly cost for a solid policy is one of the smartest investments you can make in your business's stability and long-term success. New platforms are even emerging to help you understand why proving what you own is a key part of modernising that protection.

Understanding Your Insurance Policy Cover

An insurance policy can often feel like it is written in another language, full of jargon and confusing clauses. But getting to grips with the key bits is simpler than you might think. Do not look at your policy as a list of restrictions; see it as your business toolkit, where each type of cover is a specific tool designed to solve a particular problem.

At its heart, your window cleaning insurance is a collection of safeguards. Each one targets a different risk you face every day, whether it is a customer tripping over your hose or your expensive water-fed pole system getting nicked from the van. Knowing what each part does means you can handle whatever the workday throws at you with confidence.

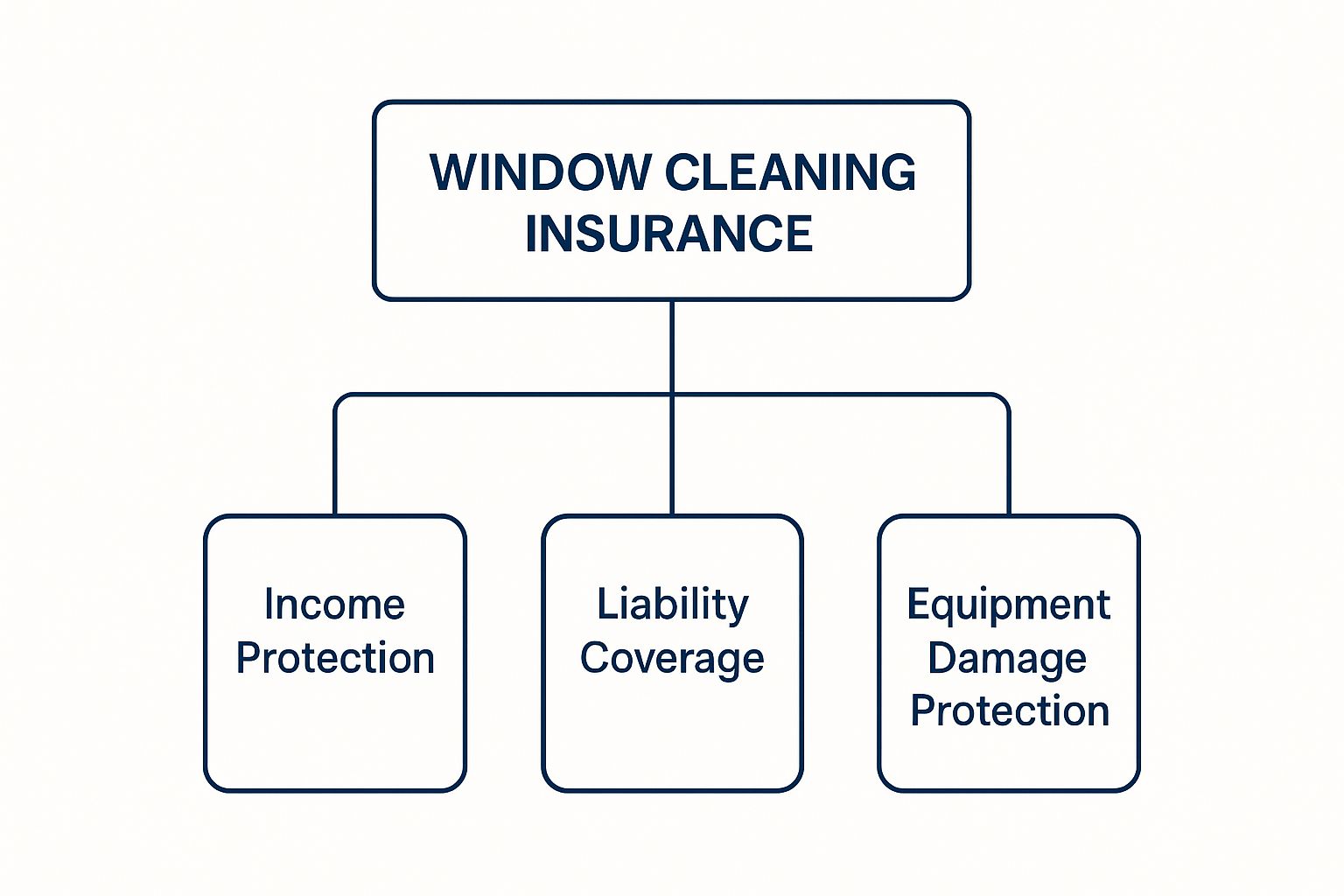

This image breaks down the core benefits of having a solid, comprehensive policy.

As you can see, a good plan gives you a three-pronged defence: it protects your liabilities, your income and your essential gear.

The Essential Types of Cover

Let's break down the insurance every professional window cleaner needs to think about. Each type of cover acts as a different layer of protection, safeguarding your business from the ground up.

Core Insurance Cover for UK Window Cleaners

| Type of Cover | What It Protects Against | Is It a Legal Requirement? |

|---|---|---|

| Public Liability | Claims of injury to the public or damage to their property caused by your work. | Not legally required but essential for trading. Many clients will not hire you without it. |

| Employers’ Liability | Claims from employees who get injured or fall ill as a result of working for you. | Yes , if you employ anyone, including part-time or temporary staff. |

| Tools & Equipment | Theft of or damage to your essential gear, like ladders, poles, and cleaning systems. | Optional but highly recommended to avoid costly out-of-pocket replacements. |

| Personal Accident | Loss of income if you are seriously injured and cannot work. | Optional but a vital safety net for sole traders and the self-employed. |

| Professional Indemnity | Claims of financial loss from a client due to negligent advice you have given. | Optional but worth considering if you offer specialist advisory services. |

The table above gives you a quick overview but let's dive into what these really mean for your day-to-day operations.

Public and Employers' Liability: Your Core Defence

The most fundamental part of your toolkit is Public Liability insurance . This is your main shield. If you accidentally crack a window pane, scratch a conservatory roof or a passer-by trips over your equipment, this cover steps in to handle the legal fees and any compensation costs. It is the one thing you really cannot trade without.

If you have anyone working for you—even casual weekend help— Employers’ Liability insurance is not just a good idea; it is a legal must-have in the UK. It protects your business if an employee gets hurt or falls ill because of their work. The government takes this one seriously and the fines for not having it can be crippling.

Think of your insurance policy as your business's suit of armour. Public Liability is the shield that deflects claims from others and Employers’ Liability protects the team inside. Each piece is vital for complete protection.

But liability is only half the story. You also need to protect your ability to actually do the job.

Protecting Your Livelihood and Assets

Your tools and equipment are the lifeblood of your business. That is where Tools and Equipment cover comes in. If your gear is stolen or damaged, this policy helps you replace it quickly without having to dip into your own pocket. It keeps your cash flow healthy and gets you back on the tools and earning again. Simple as that.

For sole traders, Personal Accident cover is another game-changer. It provides a financial buffer, paying out if you are seriously injured and cannot work. This income protection ensures you can still pay the bills while you recover—an absolutely vital safety net when you are the business.

Finally, if you ever give specialist cleaning advice, maybe on how to treat historic or delicate glass, Professional Indemnity insurance becomes important. This covers you if a client claims your advice was flawed and cost them money. Since every policy is a binding legal agreement, it is always smart to understand how to review an insurance contract so you know exactly what you are covered for.

The Hidden Costs of Claims and Insurance Fraud

Making an insurance claim might seem like a simple fix when something goes wrong but the reality is far more complex. It is never just about the payout. The moment you file a claim, you kick off a chain of events that can have a lasting financial and operational impact on your window cleaning business.

The most immediate sting is the hit to your future premiums. Insurers work on risk and a claim on your record paints you as a higher risk. This often leads to a sharp increase in what you pay for your renewal, directly eating into your profit margins for years to come.

Then there is the hidden cost that really grinds you down: lost time. Dealing with a claim means wading through a mountain of paperwork, endless phone calls and meetings. Every hour you spend talking to adjusters or filling out forms is an hour you are not out on a job, earning money. For sole traders and small businesses, where time is literally money, this disruption can be crippling.

The Ripple Effect of Insurance Fraud

While genuine claims are just part of doing business, the industry is battling a much bigger, more corrosive problem: insurance fraud. And it is not a victimless crime. Every dishonest claim affects every single person and business holding a policy. The cost of this dishonesty ultimately filters down to all of us, pushing up the price of cover for honest tradespeople.

In the window cleaning world, fraud can pop up in different ways. It could be a homeowner exaggerating the extent of accidental damage or even an orchestrated 'slip-and-trip' scam from a member of the public. These might seem like small, isolated incidents but their collective impact is enormous.

Here is how fraudulent claims send ripples across the industry:

- Higher Premiums for Everyone: Insurers have to recover the money paid out on fraudulent claims. They do this by spreading the cost across all their policyholders. In short, your premiums go up to cover someone else's dishonesty.

- Tougher Claim Scrutiny: To fight back against fraud, insurers are forced to bring in more rigorous investigation processes. This means even genuine claims take longer to process and demand more provable evidence, creating delays and frustration for honest traders like you.

- Damage to the Industry’s Reputation: When fraud is common, it can tarnish the reputation of tradespeople as a whole. This can make potential clients more suspicious and potentially lead to more disputes down the line, affecting the entire industry's credibility.

The cost of this dishonesty is staggering. You can get a clearer picture of how insurance fraud really costs the industry in our detailed guide, which dives into this multi-billion-pound problem.

Why Your Integrity Is a Collective Asset

This is why fighting fraud is not just up to the insurers; it is a shared responsibility that benefits the entire window cleaning community. When you run your business with integrity, you are not just protecting yourself—you are helping keep the entire system fair and affordable for every other professional out there.

By keeping meticulous records, documenting your work thoroughly with photos and notes and being prepared to challenge suspicious claims with provable facts, you contribute to a much healthier insurance market. This collective effort is what keeps premiums manageable and ensures the system works for those who genuinely need it.

Ultimately, your commitment to honesty is one of the most powerful tools in your arsenal. It protects your reputation, strengthens your case when you do need to make a genuine claim and helps secure the long-term affordability of essential insurance for everyone in the trade.

How to Build an Undeniable Insurance Claim

When an accident happens on a job, your first reaction is usually shock or stress. But in those crucial first moments, what you do next can be the difference between a smooth, provable claim and a long, drawn-out dispute.

Solid, undeniable evidence is your absolute best defence. It works both ways: it protects you against dodgy or fraudulent accusations and it helps your insurer process a genuine claim without hitting unnecessary roadblocks.

Building an undeniable insurance claim is not about being defensive; it is about being professional and prepared. Think of it like creating an airtight case file that leaves no room for argument or doubt. This body of evidence becomes your strongest asset, helping you prove a genuine claim while swiftly shutting down a dishonest one.

Immediate Actions at the Scene

The second an incident occurs—whether it is a cracked pane of glass, a dented car or an injury—your priority is to capture the scene exactly as it is, right away. If you wait, details get fuzzy, stories change and the scene itself can be altered.

Here is what you need to do on the spot:

- Take Time-Stamped Photos: Whip out your smartphone and take clear, detailed pictures of the damage from every conceivable angle. Get wide shots to show the context of the scene and then zoom in for close-ups of the specific damage. Modern phones automatically embed the time and date, which is gold dust for proving a claim.

- Gather Witness Details: If anyone saw what happened, politely ask for their name and phone number. An independent witness account is incredibly powerful and adds a huge amount of credibility to your side of the story.

- Do Not Admit Liability: This one is critical. Stick to the facts of what happened but never, ever say things like "it was my fault" or "I am so sorry." Admitting liability on the spot can seriously complicate your insurance claim and might even invalidate your cover entirely.

The Power of Factual Reporting

Once the immediate situation is under control, your next job is to write a factual incident report as soon as you possibly can. Do it while the details are still completely fresh in your mind.

This report should not be an emotional diary entry. It needs to be a clear, objective summary of the events.

Your report must include:

- The date, time and precise location of the incident.

- A step-by-step, chronological account of what happened.

- Details of any property damage or injuries you observed.

- The names and contact information of everyone involved, including any witnesses you spoke to.

This written record, combined with your photos and witness statements, forms the solid core of your claim. This is where being organised and proactive really pays off. Having up-to-date risk assessments and method statements (RAMS) also shows you are a professional who takes safety seriously, which can only strengthen your position.

By creating a verifiable timeline of events, you are not just submitting a claim; you are presenting irrefutable proof. This meticulous approach helps insurers validate legitimate claims faster and gives them the ammunition they need to reject fraudulent ones.

This level of detail is non-negotiable. To get a better sense of how specific data points can make or break a case, it is worth learning more about how geo-location data strengthens insurance claims. This kind of provable information protects both you and the insurer from opportunistic fraud.

Navigating Rising Costs and Industry Pressures

Running a window cleaning business in the UK right now feels like trying to walk a tightrope. Profit margins are being squeezed from every direction, with the cost of everything from van fuel to specialised cleaning solutions seemingly always on the up.

For sole traders and small businesses, these mounting operational costs are a serious challenge. When you are watching every penny, the temptation to cut back wherever you can is huge. It is easy to see why some might think about skipping an insurance renewal or choosing a cheaper, less comprehensive policy to reduce overheads.

But this is a classic false economy. While it might save a few quid in the short term, cutting corners on your insurance opens your business up to catastrophic financial risk. The potential cost of just one uninsured accident dwarfs any savings you will ever make on premiums.

The Impact of Rising Labour Costs

One of the biggest squeezes is coming from wages. Rising labour costs are reshaping the UK window cleaning sector, especially with the National Living Wage continuing to climb. For any business where labour is a major expense, these increases hit the bottom line hard.

This is part of a much bigger picture across the UK, where liability claims account for a staggering £7.6 million of the £22 million paid out daily in business insurance claims. As financial pressures mount, having solid insurance becomes more critical than ever. You can find more insights on UK window cleaning industry trends on ibisworld.com.

Meeting Higher Client Expectations

At the exact same time costs are rising, your clients—especially commercial ones—are demanding more. Large businesses, property management firms and local authorities now see proof of adequate insurance as a non-negotiable part of their vetting process. They simply will not take the risk on a contractor who cannot prove they are fully covered.

This puts window cleaners in a tough spot. The very contracts that offer better money and more stability are locked behind the requirement for comprehensive insurance. Skimping on your cover does not just increase your risk; it actively blocks your path to better-paying, more professional work.

Investing in robust insurance is not just a defensive move to protect what you have. It is a proactive strategy that proves your professionalism and unlocks access to the high-value commercial contracts essential for business growth.

Ultimately, proper insurance is an investment in your business’s future. It is the safety net that protects you from financial ruin after an unexpected accident but it is also a powerful signal to premium clients that you are a serious, reliable and trustworthy professional. In a competitive market, that distinction is priceless.

Your Window Cleaning Insurance Questions Answered

Even when you think you have got your policy sorted, real-world questions always pop up on the job. Let’s tackle some of the most common queries we hear from professional window cleaners to help you make confident decisions about protecting your business.

This is not just about the small print; it is about the practical stuff you face every day, from policy limits to tricky client demands.

How Much Public Liability Insurance Do I Really Need?

This is the big one, is it not? While there is no single legal minimum for sole traders, £1 million is widely seen as the absolute baseline. But honestly, for anything more than small residential jobs, that often will not cut it.

Many commercial clients, local authorities and larger contracts will demand a minimum cover level of £5 million , and sometimes even £10 million , right there in the tender documents. The best advice? Always check the contract requirements carefully and think about the genuine "worst-case scenario" for your typical jobs. That will tell you the right level for you.

Is Insurance for My Tools Worth the Extra Cost?

To figure this out, just ask yourself one simple question: if someone nicked all your essential kit overnight—ladders, poles, your pure water system—what would it cost to replace it all?

If that number makes you wince, or would seriously stop you from working and earning, then tools and equipment cover is not a cost; it is a crucial investment. It protects your cash flow and gets you back on the tools quickly after a theft or accidental damage, keeping downtime to a minimum.

What Happens If I Work at Heights Without the Right Cover?

This is a point you absolutely cannot afford to misunderstand. Most standard policies have specific height limits written in, often around 10 or 15 metres. If you work above your policy's stated limit without telling your insurer first, you could void your cover entirely.

If an accident happens while you are working at a height you are not insured for, your provider could flat-out refuse the claim. That would leave you personally on the hook for everything—legal fees, compensation, the lot. It could be financially devastating.

Being completely transparent with your insurer about the full scope of your work is non-negotiable.

Why Do Some Clients Refuse to Hire Uninsured Cleaners?

For clients, especially commercial ones, your insurance is a clear sign of professionalism and a vital risk management tool for them. By hiring an insured cleaner, they are protecting their own business from being held liable for any accidents that might happen on their property.

Industry data shows that while public liability insurance is essential for window cleaners, a surprising number of small businesses across the UK are uninsured or underinsured. The fallout can be severe, which is why so many clients now make proof of adequate cover a non-negotiable condition of hiring. You can read more on UK business insurance statistics on policybee.co.uk to get a better sense of the landscape.

At Proova , we believe insurance should be clearer and more secure for everyone. Our platform helps you document your assets and build a verifiable record, strengthening your position when you need to make a claim and protecting you against fraud. Discover how Proova can support your business at https://www.proova.com.